Yes, it’s inflation and, like some creature from the black lagoon, it is emerging from booming wages, via the AFR:

Reserve Bank assistant governor Chris Kent says bond markets are underestimating the risk of wages growth stoking higher inflation, as long-term Australian bond rates fall towards historically low levels.

…”What we have had here is a gradual pick-up in inflation while unemployment rates have moved to quite low levels in NSW and Victoria,” he said.

“The question is will that be picking up soon enough to give us some comfort, and that depends on the outlook.”

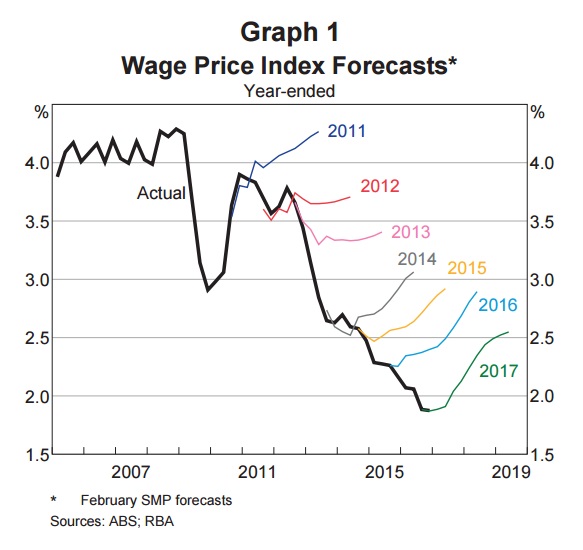

Deary me. Inflation like this, Dr Kent?

No, Dr Kent, neither wage nor broader inflation will be picking up any time soon. Both will be crashing in short order, just as markets are pricing for the next decade:

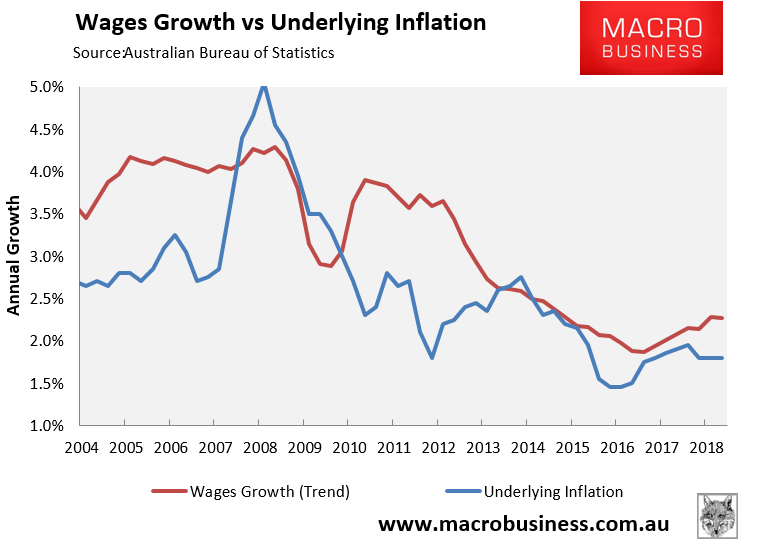

There is no inflation. In fact, there is deflation, a lot of it, emanating from house prices and about to swamp everything else including wages:

This driving in the rear vision mirror is typical of the RBA.

Take the post-GFC mining boom. Rather than acknowledge that it was a passing fad, the Bank foresaw a 30 year boom and hiked interest rates plus egged-on the dollar in a structural adjustment to “mining-led” growth. Everything tradable got hollowed out.

When that boom died in the blink of eye two years later, the Bank did a volte face to “rebalance” the economy to “non-mining” growth drivers via slashed interest rates. This lurch from one polarity to another whiplashed the entire economy from east to west and back again.

Now, of course, it is desperately trying to undo its own wild property bubble without blowing up the entire economy. Again it is failing and will be forced to slash rates, this time plunging Australia into the lowflation dynamics already prevalent across the Western world.

At each step the lunacy of the RBA was to be looking backwards when it should have been looking forwards, fighting the last war, as it were. The first time it fought a repeat of 1980s mining inflation that was never coming. The second time it fought a structural mining bust with cyclical policy tools. Now it is trying not to ease rates for fear of wage inflation and re-igniting a property bubble that is bursting right before its eyes.

There were always alternative policy paths but the Bank never took any. The monetary world was in foment with new ideas and options that sought to manage many of the same problems Australia was experiencing with direct lessons for any forward looking central bank.

During the mining boom it should not have hiked rates so far and embedded inflation expectations in the currency. It should have joined the global currency war, printing AUD to give to speculators.

At the beginning of the housing bubble it should have cut investor mortgages off at the knees and backed macroprudential hard and early. It should also have campaigned for lower immigration instead of celebrating it. This would have slashed interest rates to zero and crashed the currency, helping deflate the economy externally instead of internally via wages. The price of that mistake has been political chaos as households have taken the full brunt of the income recession.

Today the bank is pretending like some village idiot that the economy will be just fine as a $7 trillion asset market comes undone when it ought to be planning for the fallout with rates at zero plus open discussions of unconventional policy options. These could include QE to buy bank bonds or to lower BBSW rates. Or, it could buy longer yielding assets, though that will not help much given mortgage rates are set at the short end. It could still be printing money for foreign speculators to drive down the currency. Or, it could go further, and directly finance fiscal spending.

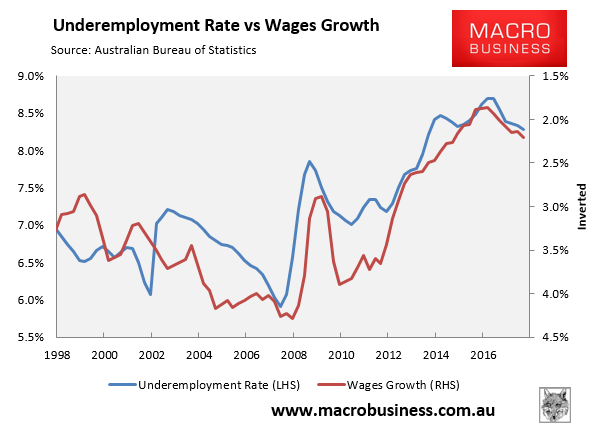

How do we fix this busted wheel? First, the place needs a damn good clean out. It is full of dead wood governors that have not looked out the window in a decade. Second, given it is completely lost in today’s lowflation environment, we should change the bank’s reaction function from keeping unemployment low to keeping underemployment low:

The RBA has done Australia immeasurable harm since 2010. Time it paid for it. Independence is no excuse for ineptitude.