From Bloomberg:

Australia’s best-performing superannuation fund is going against the grain by avoiding cash and bonds, betting the 30-year investment horizon of its youthful members means it can ride out looming economic shocks.

Hostplus, which represents swathes of the country’s baristas and restaurant waiters, had about 53 per cent of its $40 billion invested in the sharemarket, and the remainder in unlisted assets including airports and water-cleaning plants, chief investment officer Sam Sicilia said.

Hostplus beat local peers with a 10 percent return over three years ended Jan. 31, according to Lonsec Group. It’s also top ranked over five years, up 8.9 percent and outpacing the country’s largest pension fund AustralianSuper Pty, the data show. Hostplus has held no cash since at least 2011 and bonds in its portfolios were effectively zero over the past three years, according to Hostplus. The firm prefers stakes in office buildings, pipelines and emerging technology.

Part of that success was due to the fund’s ability to stomach less liquid unlisted assets, Mr Sicilia said.

Risk and Reward

There are a few ways to read this.

I think the implication of the article is meant to be that the fund that has done the best over the past 5 years did so because it shunned low-risk assets like cash and bonds and loaded up on high-risk assets, and therefore the same strategy will work going forward. Which is why ASIC require everyone to add a disclaimer “Past performance is not an indication of future performance”. You do need to give Hostplus credit for taking a more risk over a period where stock markets performed well relative to other assets. If it were a conscious tactical decision to allocate to more risk assets (I don’t know) then the decision was a good one.

However, the way the article is written seems to imply that Hostplus is simply taking more risk because its members are younger. Which is concerning. The implication would then be:

- Hostplus will go up more when markets rise and down more when they fall as Hostplus has structurally higher risk. Suggests the recent outperformance was circumstance rather than good judgement

- You don’t want to be in this fund if you are older because they are tailoring the asset allocation for younger members

Are unlisted assets less risky than listed ones?

Another implication of the article is that unlisted assets are similar to cash and bonds. They aren’t.

This proprietary process involves implementing our normal hedged liquid alternative process, but only marking to market occasionally, and then reporting some combination of the weighted average of the prior few years’ prices, with a healthy weight also given to our own unaudited estimates of what the Fund is likely worth (based on how we think it should’ve performed).

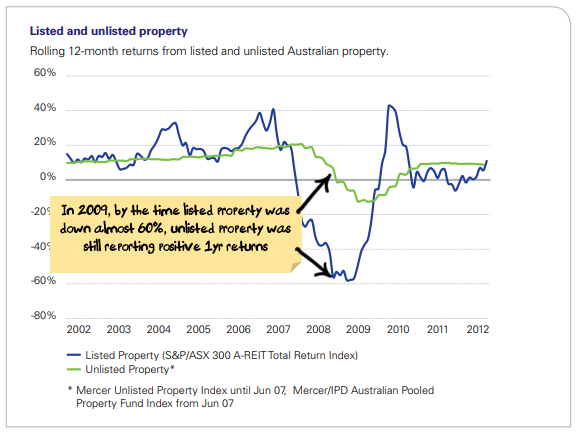

This is the issue when comparing funds that invest in listed assets vs ones that invest in unlisted assets – you have no way of knowing the actual value of the unlisted assets. A great example is unlisted property funds during the financial crisis. Unlisted property funds invest in effectively the same assets as listed property funds, the underlying properties are worth the same, the performance differs because of how it is reported:

Do you really think that while listed property prices fell almost 60% over a year, unlisted property prices had increased slightly over the same year? They both own the same buildings, it is just that unlisted assets don’t get valued regularly and so the values being reported were the values from prior years and didn’t reflect the actual market value.

By this stage, unlisted property funds weren’t trading anyway and so you couldn’t sell your unlisted asset at the inflated made-up prices – who would want to buy unlisted property assets at last year’s prices when you could get listed property assets at almost 60% off?

So, this is the trillion dollar question. Is an unlisted property trust less risky than listed property? There are a lot of people who say yes as the reported prices are less volatile – but my emphasis on the word “reported”.

For me, if it is the choice between owning an asset:

- in a listed vehicle where I can see what is happening, how much it is worth and buy/sell at any time, or

- in an unlisted vehicle where I don’t know what is happening, the asset can only be sold at infrequent intervals and the valuation is a mix of prices from prior years and management estimates

then I will take option 1 every time. Just because I can’t see the price move doesn’t mean that it hasn’t.

The other problem is that I can be diluted by other investors coming and going. To illustrate with an extreme example, let’s say:

- You and I are the only investors in a fund with $100 each invested

- The fund owns 50% an unlisted asset and 50% cash. So, the total value of the fund is $200 made up of $100 in the asset and $100 in cash.

- The asset falls 60% ($60) in price, so our fund is now only worth $140 ($70 each for you and I) but the fund doesn’t revalue the asset and so reports the fund still being worth $200.

- I decide to redeem my holding in the fund.

- The unlisted asset can’t be easily sold, and so the fund pays me $100 cash being half of the $200 that the fund is still being officially valued at.

- This leaves you with $40 of unlisted asset – double the loss that you should have taken.

Is now the right time to have no cash and bonds?

Assets move in cycles. Ordinarily, towards the end of a ten-year bull market in risk assets you would want to be increasing your holdings of cash and bonds, leaning into the cycle so that when the bull market in risk assets ends you can cushion the downside and you have a war chest to look for bargains. That is my strategy at the moment, but Hostplus has taken the opposite strategy – they are suggesting that now is the time to own more risk assets and to abandon cash and bonds.

Hostplus may be right. Recessions may be avoided, central banks might hit the printing presses, growth and inflation might return and risk assets might continue to go up.

I’m hoping the Bloomberg journalist has mis-represented the Hostplus investment process – a cynical view of the Bloomberg article would be that Hostplus simply loads up on risky assets with a plan to outperform in rising markets and then use unlisted assets to “smooth” the reporting of losses when markets fall. I’m hopeful that Hostplus has a more nuanced view about the value of risk assets vs cash and bonds – they are a big fund with lots of investment managers and you would expect that to be the case.

The net effect is if you are looking to replicate the Hostplus asset allocation and abandon cash and bonds, do it because you genuinely think that risky assets will continue their streak, not because you think that unlisted assets have some magical ability to provide stability while their listed brethren fall.

——————————-

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.