Following yesterday’s crash in mortgage credit growth, which plumbed the lowest level on record, a reader sent an email asking me to explain what this means for house prices.

The short answer is “not much” when viewed in isolation. The longer answer is “a lot” if the slowing mortgage growth translates into falling housing finance commitments. Let me explain.

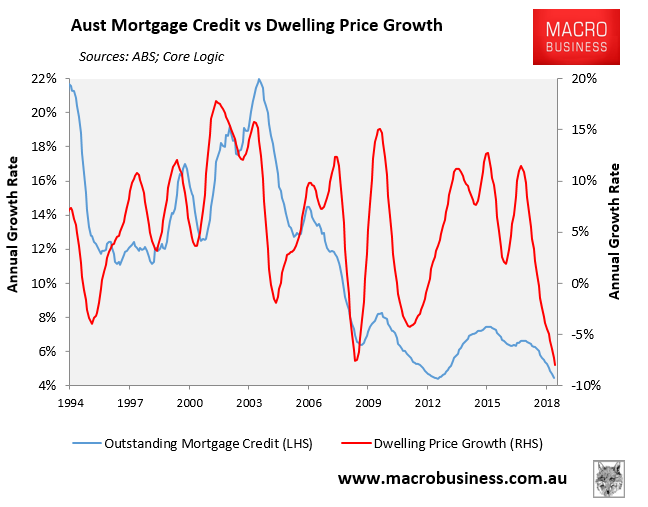

As shown in the next chart, there is a weak correlation between the growth in outstanding mortgage credit and house prices:

The reason why this correlation is weak is because mortgage credit growth measures two primary things: 1) the addition to the mortgage stock from new mortgages taken out by borrowers (increases the stock of debt outstanding); and 2) the repayment of mortgage debt by existing borrowers (reduces mortgage debt).

Only the first point – new mortgages created – actually impacts house prices. The second – mortgage repayments by existing borrowers – does not reflect new housing demand and does not impact prices.

Indeed, when interest rates are low – as they are currently – we are likely to see mortgage repayments rise, which lowers mortgage credit growth, but doesn’t actually impact house prices. Similarly, many investors have been forced to switch from interest-only mortgages to principal and interest, meaning they are now lowering the stock of mortgage debt outstanding (other things equal) without adding to housing demand.

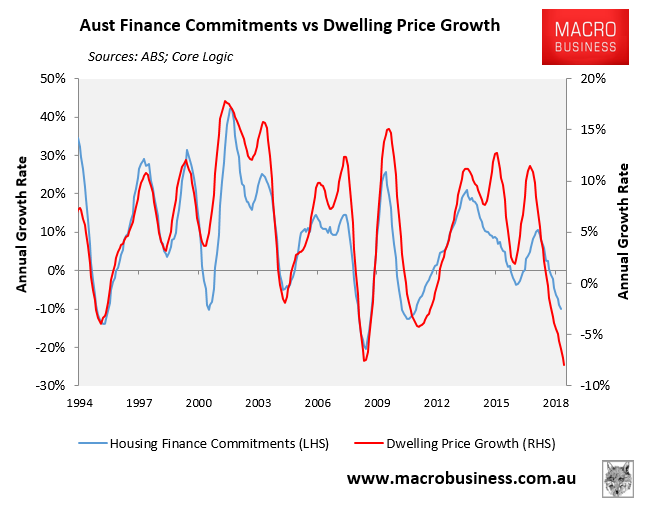

While MB does monitor mortgage credit growth whenever it is released, we prefer the ABS’ housing finance series, which measures new mortgages only and leaves out the noise generated by repayments. This series does have a very strong historical correlation with house price growth and is one of our favourite housing indicators:

So yes, the crash in mortgage credit growth does matter for house prices provided it translates to actual housing finance commitments. We’ll find out mid-month when the ABS’ housing finance series is released.