Via Deloitte:

The economy is getting worse, but the Budget’s getting better. That’s unusual: people think politicians drive the Budget, but it’s almost always the economy in the driver’s seat.

So it is undeniably bad news that the economy has been taking a few hits since the Budget update was issued ahead of Christmas. It’s hard to pick up a newspaper without getting depressed: global growth is slowing, including in our key partnerChina, trade woes are deep and could deepen further, and here at home houseprices are seeing their fastest falls in forty years. Those price falls are now damaging the Australian economy’s growth.

Yet the Budget has dodged these bullets: that’s just luck, but luck’s a fortune. The worst economic news is in things that the Federal Budget taxes lightly (such as wealth) or we don’t tax much (such as spending). Meanwhile there’s good news in profits and jobs. Both are outperforming official forecasts amid a jump in iron ore prices and rip-roaring job growth.

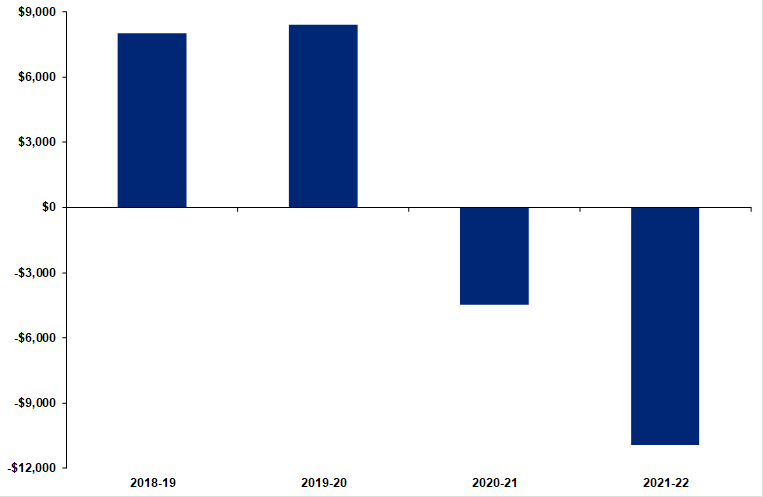

The upshot is the dollar size of the economy is set to be even bigger than the Treasury estimates that were released in late 2018. Yep, bigger – not smaller. We project nominal GDP to be 0.4 percentage points ($8 billion) above official projections this financial year, and the same again (another 0.4 percentage points and $8 billion) in 2019-20.

Annual differences in nominal GDP – DAE less official forecasts

So although downside economic risks grew fast of late (thanks to China looking sicker and to an acceleration in house price falls), the hard data that’s of most importance to the Budget – profits and jobs (for revenues), unemployment, prices and wages (for spending) – are looking more ‘Budget friendly’ than the latest official forecasts for both this financial year and next.

Budget revenues make wine from the economy’s tears

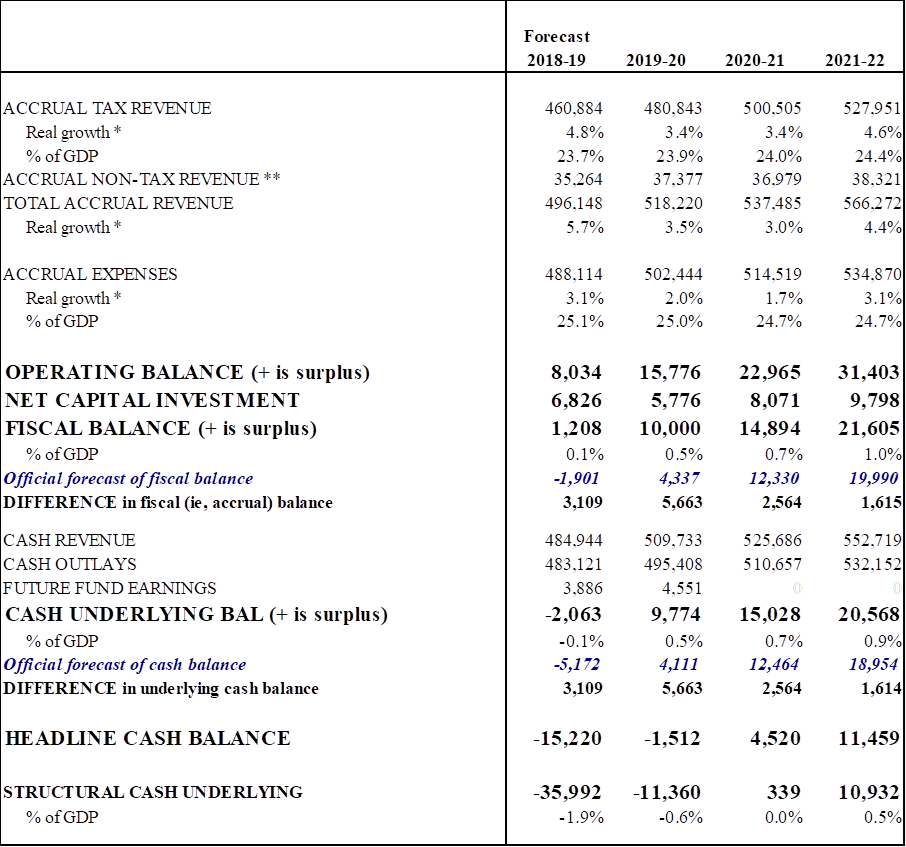

The big surprises are almost always centred in profit taxes, and that’s true this time. China’s stimulus in the face of slowdown has propped up coal and iron ore prices, while iron ore also got an extra boost from the dam wall tragedy in Brazil. And although bank profits will fall, that won’t happen straight away. So, dominated by company tax, total profit taxes (companies, super taxes, FBT and PRRT) are forecast to outperform the matching official forecasts by a handy $2.3 billion this financial year, and by a hefty $5.2 billion next.

Yet it isn’t all beer and skittles. Even in this group of winners, PRRT revenues remain a sad story, and FBT’s split personality (too tough on average Joes, too generous for car leasing, charities, and some others) leaves it as a perennial underperformer. But we’re quibbling. And with good news on jobs outweighing bad news on wages, taxes on individuals look like outperforming official views by $1.2 billion in 2018-19, fading to $0.5 billion in 2019-20.

The news is otherwise pretty poor, with crashing house prices increasingly weighing on the willingness of families to spend. That’s why indirect taxes may fall shy of Treasury forecasts by $0.5 billion in 2018-19, with that shortfall then blowing out to $1.6 billion in 2019-20.

Add those elements (plus non-tax revenues) together, and Deloitte Access Economics sees total revenue beating the official forecasts issued in December by $2.9 billion in 2018-19 and $3.7 billion in 2019-20.

Yes, most of the economic news has been bad since the Budget update was released. But the effect of that on revenues this year and next is pretty small. In particular, the house price crash is a problem for the economy, but it’s a nothing burger for the Budget – remember that we don’t tax wealth, and that indirect wealth taxes such as capital gains receive overly generous treatment. And although the house price crash will take bites out of the GST take, that downside hits grants to the States. That’sa budgetary bullet dodged.

And so too is weak wage growth. Although that will be a rising challenge for the Budget, those challenges become much more acute in later years than either this year or next.

Meanwhile profits and jobs are both still pumping iron. Or, in the case of profits, pumping iron ore. That combination means the good news in the economy is concentrated in areas vital to the tax take, whereas the bad news is in areas of secondary concern, thereby allowing the Budget to snatch rising revenues from the jaws of a weakening economy.

At the same time as the economy is raising revenues, it is slimming spending

The Government is spending on new policies. There’s been money for disaster recovery in Queensland, plus money for health and for domestic violence prevention. The Government is also reopening the Christmas Island Detention Centre. In total, thepolicies announced since the pre-Christmas Budget update have already cost $0.4 billion this financial year, with a further estimated $0.6 billion coming as a hit to the 2019-20 bottom line.

But a stronger economy (or an economy that’s strong where it counts) puts wind beneath the Budget’s wings amid better-than-budgeted (meaning lower) outcomes for unemployment, inflation and wages. Taken together, these save around $0.4 billion from spending this financial year, with those savings then sprinting up towards $1.3 billion in 2019-20.

Cautious consumers are part of the story too. Falling housing prices mean lower GST grants to the States. Adding those in too (saving $250 million this year and $1.3 billion next), we see total spending at a moderate $0.25 billion lower this year than expected by Treasury in the Budget update issued in December. Fast forward a year to 2019-20 and that gap morphs into a large $2.0 billion saving versus latest Treasury estimates. These ‘economic savings’ are big: so far they swamp the cost of recently announced policy, though the next few months may well see new spending policies keep coming thick and fast.

A better Budget bottom line

With the economy simultaneously raising revenues and slimming spending, Deloitte Access Economics sees our decade of deficits only a whisker away ending in 2018-19, with the $2.1 billion cash underlying deficit we project for this year pretty much a rounding error.

Come 2019-20 and this year’s rounding error of a deficit grows into a fully-fledged cash underlying surplus of $9.8 billion. Our estimates are $3.1 billion and $5.7 billion, respectively, better than the official estimates of cash balances from MYEFO.

Our matching fiscal balances are surpluses of $1.2 billion and $10.0 billion, respectively.

Could there be a surprise surplus this financial year?

Don’t forget that we’re already forecasting a surplus this year: 2018-19 will see the first accrual surplus recorded since before the GFC in 2007-08. And although we don’t forecast a cash underlying surplus, the Government could get there if it really wanted. Yes, it would be a stretch, but there’d be a few options open to get across the line – such as help from a larger Reserve Bank dividend – if the politics were sufficiently compelling.

But the politics of a surprise surplus probably aren’t that compelling. Chances are the hard heads will see the better politics as more likely to lie in spending in marginal electorates.

And, either way, on current trajectory we’ll have a surplus next year anyway, the first cash surplus since 2007-08. That’s great.

Remember the risks

But there are two risks. As usual, they can be summarised as ‘Canberra’ and ‘China’. The Canberra risks are all election-related. Our figuring allows for any and all policy changes announced up until 8 March, but the imminent election – and the potential for a ‘cash splash’ ahead of June 30 to eat into the revenue side of the Budget – is a key caveat.

We’re a little less scared of China-driven risks to the Budget, but only because China’s initial reaction to any acceleration in its slowdown would probably be to stomp on the stimulus accelerator. The resultant upside for coal and iron ore prices could provide the economy and the Budget with a degree of breathing space before the proverbial hit the budgetary fan.

Yet that’s temporary protection at best. Don’t forget that the good news of the moment rests on further company tax write-ups. That’s welcome, but company taxes are the most volatile (and hence uncertain) of the Government’s revenue sources. Let’s be clear: revenues aren’t roaring because the Government has been raising tax rates. They’re up because the only bits of the economy still moving at speed happen to be key drivers of revenues. Yet that also means that revenues are vulnerable to any further signs of weakness.

This is an old story. It’s a continuation of the trend since the early 2000s, when a rapidly industrialising China first began to have a massive impact on the nation’s finances. Since then, governments of both parties have used the surges in revenues to offer tax cuts and new spending, both of which then turned out to be longer lasting that the temporary higher revenues that were supposed to pay for them. This ultimately created the conditions for the persistent deficits we’ve seen over the last decade when the economy turned.

Permanent promises paid for with temporary revenues. Sounds familiar? The current run of good news on commodity prices (and company profits) could just as easily turn nasty, leaving a China-shaped hole in the nation’s finances.

Remember that coal and iron ore prices aren’t better-than-budgeted because China is better-than-expected. Rather, they’re looking good precisely because China is weakening, leading that nation to pump stimulus into construction. Over and above that, a tragedy in Brazil sent iron ore prices up even further. That combination plays to the sweet spot of company profits and company tax as of today, but don’t let it lull you into a false sense of security as to where tax revenues will head over time. Besides, bank profits are already weakening. That combination could yet prove to be kryptonite for company tax over the next few years.

The good news for the economy sours by 2020-21 and 2021-22

The further out you look, the more the short term positives of the moment run into some bad news bears for revenues. The iron ore price spike fades, the good news on jobs gets more than smothered by the bad news on wages, the dive in house prices makes consumers increasingly cautious, and overall economic growth seems set to disappoint.

Although we forecast the dollar value of the Australian economy – nominal GDP – to be better than Treasury last forecast both this year and next, the singing sauce is then removed from the table. Deloitte Access Economics forecasts nominal GDP at $4 billion below the official estimates in 2020-21, and then $11 billion (0.5 percentage points) behind by 2021-22.

In particular, wage woes start to hurt: the gap between Treasury’s forecast of wages and ours (or, for that matter, those of the Reserve Bank) grows steadily over time. With the job surge of the moment gradually powering down, that increasingly pulls the rug out from underneath taxes on individuals. From being a source of strength this year and next, they fall a little behindcurrent official forecasts in 2020-21(down $0.2 billion), and then the red ink starts to gush in 2021-22 (with a shortfall of $2.8 billion versus current official forecasts).

There’s a similar slide in spending-related taxes. Consumers have surfed unsustainable gains in their spending for too long. With house prices finally reconnecting with gravity, consumers will need to savea bit more than they have been. That adds to shortfalls on indirect taxes, which widen to $2.4 billion in 2020-21 and $2.5 billion in 2021-22.

And the good news on profit taxes becomes less good. We see profits being a bigger share of the national income pie than Treasury, but we also forecast a smaller total pie than they do. Add those together, and profit taxes, seen outperforming by a huge $5.2 billion in 2019-20, see that whittled back to outperformance of $2.2 billion in 2020-21 and $3.6 billion in 2021-22. That’s great, but those upsides are ‘nice to have’ rather than ‘knock it out of the park’.And that combination leaves overall revenue below the official trajectory, falling short by $0.7 billion in 2020-21, and then a bigger shortfall of $2.1 billion by 2021-22.

Luckily the economy keeps doing the Budget favours by driving savings on spending: despite developing weakness, unemployment looks set to be lower than budgeted. And the mix of lower-than-officially-forecast outcomes in wages, prices and interest rates will save a bunch of money on the spending front: $2.1 billion in 2020-21 and $2.5 billion in 2021-22.

There are similar savings on grants to the States ($1.9 billion in 2020-21, $2.0 billion in 2021-22), though those merely cancel out weaker GST inflows. And although policy costs grow (via top-ups to the Climate Solutions Fund and a Royal Commission into abuse of the disabled, leaving extra policy costing $0.7 billion in 2020-21 and $0.8 billion in 2021-22), that still leaves total spending set to save $3.3 billion in 2020-21 and $3.7 billion in 2021-22.

Add those elements together, and we forecast cash underlying surpluses of $15.0 billion in 2020-21 and $20.6 billion in 2021-22 (with matching fiscal surpluses of $14.9 billion and $21.6 billion, respectively). The happy news is that is still better than Treasury projectedin the Budget update back in December by $2.6 billion in 2020-21 and $1.6 billion in 2021-22.

More money, less sense?So the politicians look like having more money in their pockets. But there’s little sense on display around elections, and the politicians on both sides aren’t likely to let any windfall burn a hole in their pockets. If the economy hands the Budget more money, that will be ploughed straight back into promises. That’s short-sighted.

But the good news is that a decade of deficits is drawing to a close. The toxic politics of Budget repair were a torment for all involved. Everybody wanted everybody else to wear the pain of Budget repair, except for the Senate, which never saw a spending cut it liked.

But it’s happening because luck is still running the Budget’s way. Yet that may not last: the Budget is looking better even though China and house prices are looking worse. That’s a reprieve, not a mission accomplished.

The thief in the night: bracket creep

Inflation gradually pushes people into higher tax brackets. Despite 2018’s tax cuts, PAYG collections this year would have been $1.3 billion less if the 2014-15 thresholds had simply been indexed to the CPI. And the later stages of the already legislated tax cuts – which are substantial – don’t arrive until a few years from now. That’s why the punters would be paying less tax today than had we merely indexed 2014-15 thresholds to inflation.

With an election imminent, those gaps may be about to be more than closed. If not, however, then fiscal drag will get worse before it gets better: we forecast bracket creep to lift to $3.7 billion in 2019-20, $6.6 billion in 2020-21, and then to reach $9.9 billion in 2021-22.

So even though weak wage growth means that bracket creep isonly creeping along, it’s enough to see taxman grab a growing slice of paypackets(then again, the already legislated tax cuts – 1 July 2022 and 1 July 2024 – imply that the cavalry is already coming).

The twenty cents in the dollar of wages and salaries set to be paid in tax in 2021-22 has only been beaten once before in history – in 1999-00, just before the GST first came in. That suggests we haven’t heard the last of tax cuts ahead of the coming election.

PS, let’s fix that epic fail

Finally, we’d remind you that the Budget – this nation’s social compact with itself – is about far more than deficits or surpluses. We need taxes that don’t hurt prosperity and spending that ensures fairness. On the latter front, this nation has one epic fairness fail – the continuing crush we’re putting on the living standards of the unemployed. History won’t judge our record kindly.

Summary table: Overall Budget projections ($ million)

In short, don’t create a structural deficit by cutting taxes with cyclical revenue. Use one off payments instead if stimulus is required.

Of course, Recessionberg will ignore all sense and do it anyway to booby trap the budget for Labor.