DXY was strong last night as EUR sank:

Normally this would have resulted in a weak AUD but the deflationist RBA drove it up across the board instead:

Gold fell:

Oil was firm:

Metals too:

Miners rallied:

EM stocks too:

Junk was stable:

Treasuries eased:

Bunds too:

Aussie bonds got bashed by the deflationist RBA:

Stocks lifted:

Westpac has the wrap:

Event Wrap

US housing starts tumbled in Feb, posting a bigger than expected decline of 8.7%, (est: -1.6%). Permits, a gauge of pipeline construction also fell. The housing industry has cooled in the last year but the recent sharp fall in interest rates and ongoing firming in wages should buoy the market going forward. The Conference Board’s consumer confidence index fell to 124.1 in March from 131.4, the fourth decline in the last five months; weakness was concentrated in households’ assessment of present conditions – the expectations sub index also fell but by a much lesser amount. Readings of the labour market also notably weakened. Capping off a round of weaker data; the Richmond Fed’s manufacturing index fell to 10 from 16, in line with expectations.

FOMC member Evans said the impact of China’s slowdown on Fed policy depends on its scale, Harker said he didn’t support a December hike, and Daly said inflation has not met its 2% goal and falling inflation expectations require vigilance.

Event Outlook

NZ: The RBNZ OCR Review at 2pm today, releasing a one-page statement, should be largely a repeat of the message given at February’s MPS, that the OCR is expected to remain on hold over the next two years and risks are evenly balanced.

Australia: RBA Assistant Governor (Financial Markets) Kent speaks on a panel at the FX Week Australia, Sydney 10:10 am.

China: Feb industrial profits data is released.

Euro Area: ECB President Draghi speaks at the ECB and Its Watchers XX conference which also includes Praet and de Guindos. Italian business and consumer confidence data is released.

US: Jan trade balance is expected to be a $57.0bn deficit.

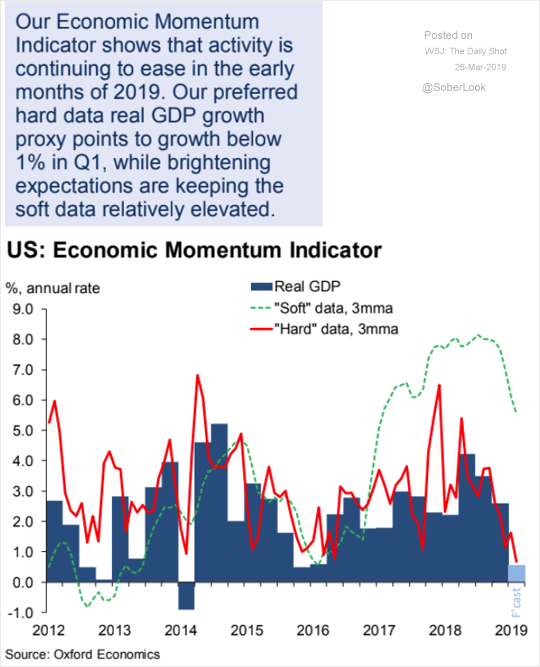

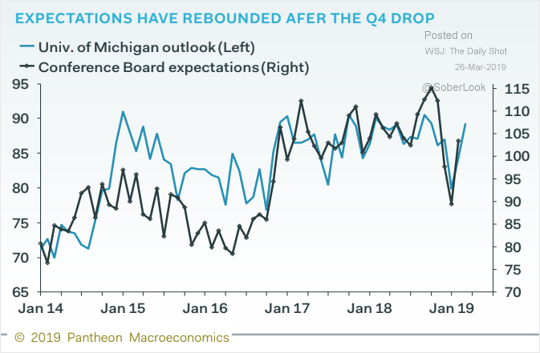

Some ordinary US data but still no cause for alarm. Housing starts are still ‘shut down’ effected and previous months were revised up. The consumer is still at solid levels. Here are some more charts on the US from the WSJ’s Daily Shot:

Readers will know I’ve long expected the US to slow into H2 as the fiscal cliff arrives for a few quarters. That has been made worse and brought forward by the shut downs. But, unless there is a further stock market shock, growth will climb back to trend above 2% into next year, which is nearly always a good year given Presidential race spending. The risk to the US are still external.

The AUD and Aussie bonds were simply popped by an overly optimistic and therefore deflationist RBA yesterday.