Policy makers clearly feel that easing is necessary, but question the means by which it should be delivered. RBA Assistant Governor Bullock said as much in her speech about lending standards yesterday. Bullock highlights that the period of mandated credit tightening by regulators is now over, perhaps implying that if banks are tightening, they are doing so on their own volition. Bullock goes even further, to implore banks to ease their lending standards. All of this follows on from developments in 4Q 2018, when APRA chose to relax lending caps – a tell-tale sign that policy makers wanted easing, but not necessarily through rate cuts.

Some RBA officials are defending the company line by pointing to backward-looking data. RBA Assistant Governor Kent continues to suggest that term premia in bonds are too low, and that the bond market has become too aggressive in pricing in cuts, because in his view, investors are underestimating the risk of accelerating wage inflation. He has tried to downplay the significance of market signalling. However, his argument only works if the labour market remains tight. If the unemployment rate were to start rising, a cyclical upturn in wage inflation might not materialize, or might be quite short-lived.

The RBA says that there is a tension in the domestic economic data to be resolved. In the March meeting statement, the RBA basically said that much of the rates outlook now hangs on the state of the labour market. In part, this is because labour income growth is a driver of consumption growth, even in the face of falling house prices. But in the March meeting minutes, the Bank clarified its position even further – the GDP and employment data are telling two very different stories about the economy. GDP data suggests that growth momentum has slowed below 1% annualized, well below RBA forecasts and estimates of potential. On the other hand, the employment data suggests that the economy is still booming, and that slack is limited, as evidenced by the low unemployment rate. How this tension is resolved seems key to how rates will evolve.

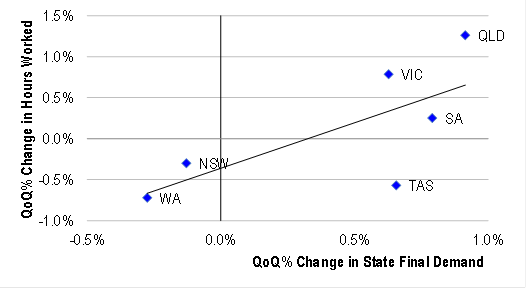

The link between GDP and employment has not broken, across states. While for now, there appears to be a de-coupling in the historical relationship between employment and GDP growth, the state data suggests that the linkage is still strong. Over the past quarter or so, the states that have experienced the strongest (weakest) job creation are also the same states that have experienced the strongest (weakest) GDP growth.

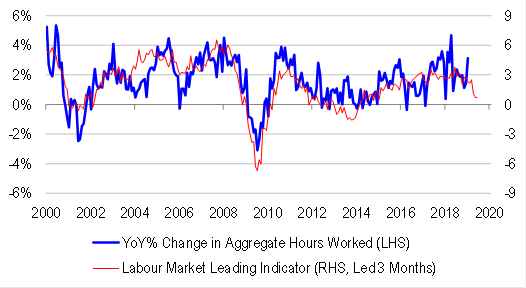

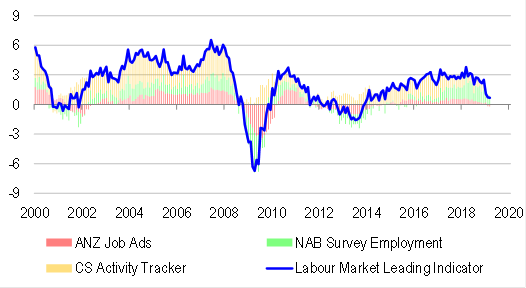

5. Employment is a lagging indicator. Our broadest possible leading indicator of labour market conditions is pointing much lower. We have created a new labour market conditions index, based on conventional labour demand indicators (eg NAB survey hiring intentions, ANZ job ads), as well as our less conventional, domestic activity tracker. The labour market index leads trend growth in hours worked by roughly a quarter, with a correlation of more than 70%. In recent times, the indicator has fallen away sharply, across all components. It is pointing to job creation well below trend, consistent with higher unemployment, but for offsetting movements in labour force participation.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.