Via Livewiremarkets:

In assessing whether to get long or short residential mortgage-backed securities (RMBS), we undertake a great deal of quantitative analysis, including revaluing the homes that protect these bonds at regular intervals and developing globally unique RMBS default and prepayment indices. (Regular readers will know that we exited most of our RMBS in February 2018.)

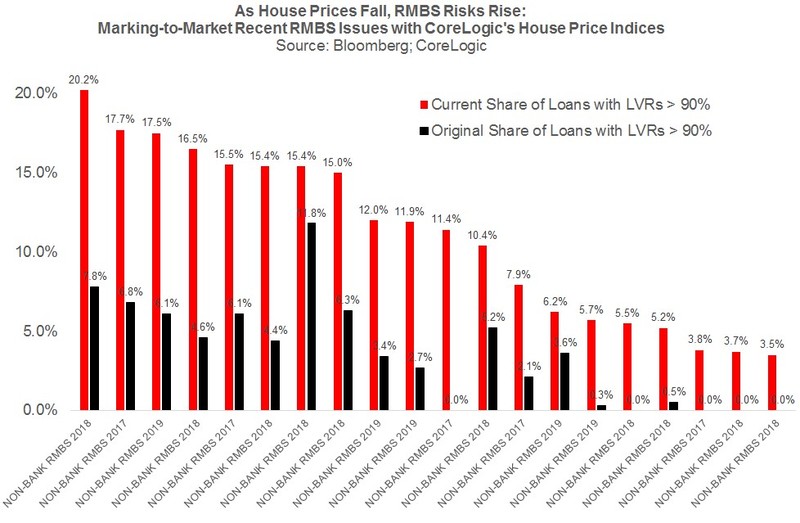

As house prices fall, the loan-to-value ratios underpinning an RMBS issue rise in lock-step, which reduces the equity protecting the bond. Using Bloomberg data on the current amortised value of the home loans in all Australian RMBS pools, the LVR distribution of the loans, and the geographic location of the properties, we have marked-to-market all the 2017, 2018 and 2019 issues after accounting for the amortisation or pay-down of loans through to the end of February 2019.

What we find is some huge increases in the share of an RMBS issue’s assets with LVRs over 90% compared to the leverage reported when the bond was originally sold to investors (often jumping from 5% of loans to 15% to 20% of loans).

We have also documented some recent RMBS deals where the share of loans that are underwater, or have LVRs over 100%, has increased strikingly, including one transaction where more than 1-in-10 loans appear to be underwater.

…At the same time as the equity protecting RMBS is shrinking, we have demonstrated that RMBS default rates are trending higher back to GFC peaks using our compositionally-adjusted hedonic index of RMBS arrears. This is consistent with the RBA’s data on mortgage arrears, which I have enclosed below our index chart.

There is also the problem of declining mortgage prepayment rates, which is blowing out the expected life of RMBS bonds (adversely impacting assumed credit spreads) as borrowers struggle to prepay loans at the same rate as they have done in the past.

Chris has previously noted his desire to get short Aussie RMBS in his AFR column though whether he succeeded is an open question. There are a couple of key points of note for the credit outlook here:

- these RMBS are mostly non-bank issuance stemming from the post-2016 macroprudential slowdown in bank lending;

- however, Aussie banks do buy these bonds so there could be feedback loops into the wider system;

- crucially, RMBS are off balance sheet and do not have any lender of last resort. As such they are much more exposed to the underlying asset values than bank held mortgages. If they sink then spreads will widen and issuance fall, creating a doom loop, though there would likely be a fiscal response of buying the bonds directly by the AOFM;

- finally, if you think this has echoes of the US “Big Short” then you’re spot on. The similarities are spooky. Indeed, if underlying collateral in these bonds is falling, and the LVR coverage shrinking so fast, then you have to ask where are the ratings agencies and their AAA rubber stamps? Admiring deals “structured by cows” again?

History doesn’t repeat but…you know the rest.