Is Australia’s little financial crisis over?

Advertisement

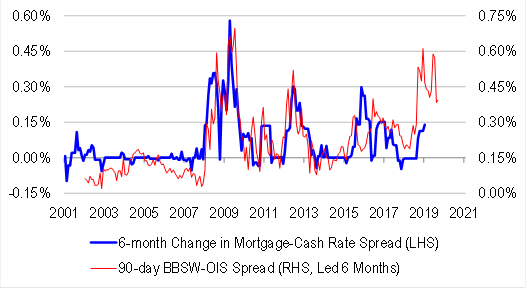

It’s been running for a few years: the widening spread between the cash rate and bank funding costs expressed through BBSW. This has led to impaired monetary transmission for the RBA as banks are forced to wither hike rates out of cycle, or not cut when it does.

Recent weeks have seen the spread compress to levels not seen in a while though banks are still out of the money, via Credit Suisse:

Westpac explains the spread compression by observing an abundance of cash at the moment:

Advertisement

The full text of this article is available to MacroBusiness subscribers

Cancel at any time through our billing provider, Stripe

About the author

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Advertisement