The Aussie dollar continues to hold up against all rapidly deteriorating data today:

Despite bonds soaring:

Long end yields are grinding relentlessly towards the 1970s and, probably the 1960s as well:

Advertisement

Yet the currency refuses to follow, basically for the first time since the float:

Advertisement

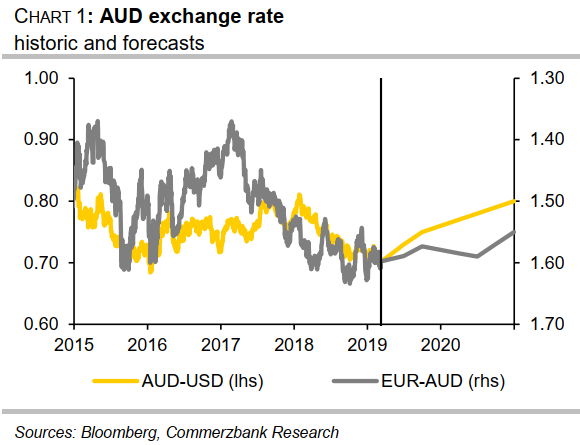

The reason is the high terms of trade. Markets have still not made the leap to the new Australian normal in which high commodity prices DON’T trickle down to the real economy thanks to years of terrible policy. This rubbish from Commerzbank is typical:

China remains the greatest risk.

The recovery of the Australian economy and thus of the AUD will depend largely on the extent to which concerns about the Chinese economy prove to be true … we are optimistic that there will not be a noticeable slump in Chinese economic growth.

We forecast a recovery of the Australian currency, especially against the US dollar, which is however primarily attributable to a weak greenback rather than a strong AUD.

Fed unlikely to raise its key interest rate any further.

ECB will also continue to pursue an expansionary monetary policy, we expect a sideways movement in EUR-AUD for the time being.

As soon as the prospect of an interest rate hike in Australia next year emerges, the AUD should also gain against the EUR.

Over that time frame, bulk commodities and the terms of trade can only fall given the Vale spike has already sent them to the sky.

Advertisement

If I’m right about the 100bps of cash rate easing ahead then some time next year the spread will be as wide as it was in 1980 and the negative yield pressure on the AUD will be immense.

XJO is down modestly:

Big Iron is mostly down:

Advertisement

Big Gas too:

Big Gold is better:

Big Banks are not:

Advertisement

But brokers have jumped as realty wilts:

Still so much mispricing to enjoy.

——————————————

David Llewellyn-Smith is chief strategist at the MB Fund and MB Super which is long international equities and local bonds that will benefit from a weakening Australian economy and dollar so he is definitely talking his book.

If the ideas above interest you then contact us below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.