There are reasons to be optimistic. More infrastructure is coming. But there are other, more powerful forces, that make it a worry. We know steel demand is being dented by the manufacturing recession and weak car demand. But the big one is realty. It always is, constituting 30-40% of steel consumption. This is a problem in the year ahead with sales already falling and starts tracking them lower:

Note that the weakest periods of bulk commodity prices have always coincided with real estate weakness.

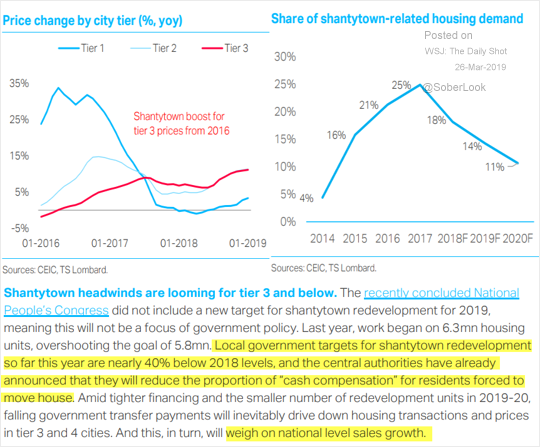

Then there is this from T.S. Lombard:

Advertisement