Reporting season has been better than feared. To date, the 1.2 ratio of beats-to-misses has been only modestly below average, while company guidance has been surprisingly resilient, with more outlook upgrades than downgrades.

Despite companies remaining generally optimistic on the outlook, 61% of companies have seen downgrades to FY19 consensus EPS estimates after reporting. Hence, analysts are being more cautious than companies on the outlook. However, ASX 100 earnings expectations have actually been revised up 0.7% through reporting season (Figure 18), with consensus now expecting 5.0% EPS growth in FY19 (albeit slowing from 6.7% in FY18, Figure 17). The increase has been entirely driven by a 7.6% upgrade for the Resources, with a 1.5% downgrade for the Financials and a 1.1% downgrade for the Industrials.

The main upside surprise this reporting season has come from larger than expected dividends, potentially driven by companies looking to return excess franking balances ahead of Labor’s proposed franking scale-back.

That does not look like it’s holding up to me. Other than a big thank you to Vale.

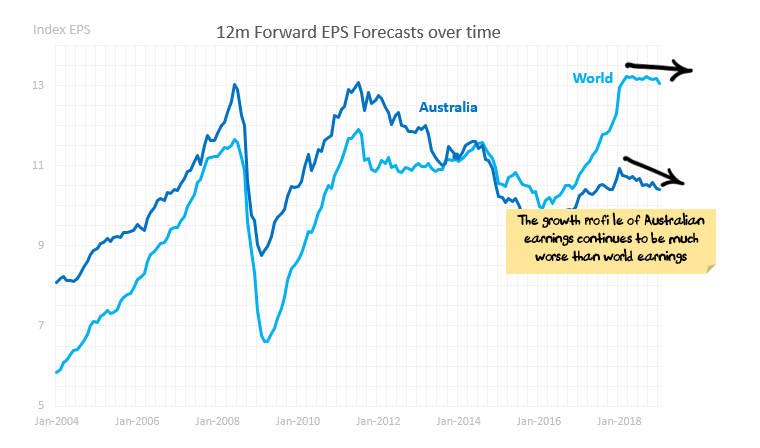

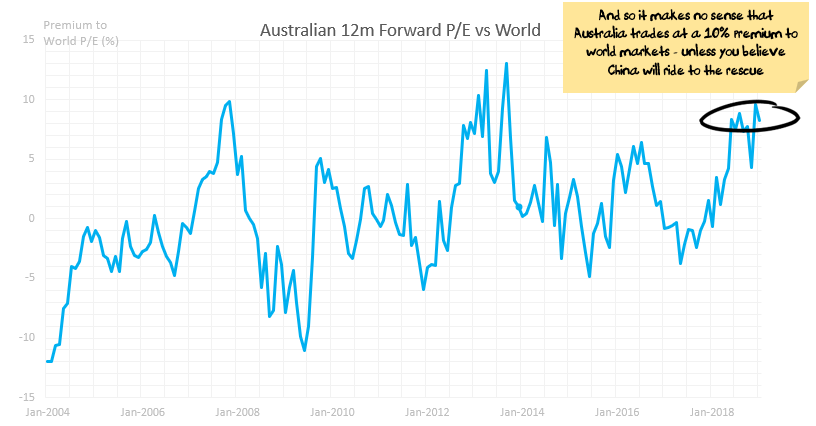

Very much along the lines of our expectations. The Australian share market starts the year facing a falling housing market, some of the weakest profit growth in the developed world, some of the highest interest rates in the developed world, growth slowing in (key customer) China and one of the most expensive share markets in the world.

Advertisement

The Australian market seems to us to be a one-way bet on China launching another major stimulus package, which will, in turn, boost demand for Australian iron ore and coal. This is possible, and maybe even likely if conditions get worse in China. However, there are a number of differences this time:

China has more debt than before. And additional debt is less and less effective at producing growth. Net effect: China needs to incur far more debt than they ever have to produce far less growth. There is a question mark over China’s willingness to do this. We expect China probably will, but that economic conditions will need to worsen markedly before their hand is forced.

Trade wars. China already runs a significant trade surplus with most countries. With tariffs, trade wars and a slow global economy there is downside risk to Chinese industrial production. i.e. there are other parts of the Chinese economy that will be competing with infrastructure for government stimulus, and these parts of the economy don’t use anywhere near as many Australian commodities.

China is already spending a massive amount on capital expenditure. There is scope for China to grow its infrastructure spending, but the key driver of much of China’s growth is home building which is already running at record levels. This limits the growth possible.

Advertisement

With those points in mind, and Australian stocks seemingly already pricing in a China bailout, we are opting to invest elsewhere. All of our portfolios are at, or close to minimum weights for Australian stocks.

—————————————

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super which is long international equities versus Australian. If the ideas above interest you then get in touch with us below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.