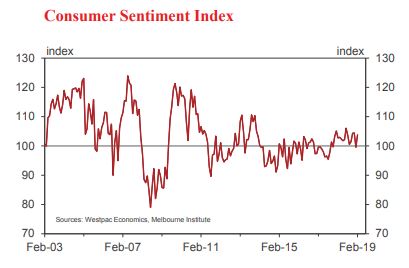

Sentiment has recovered after a shaky start to the year. The previous survey in January had shown a sharp pull back, the Index dipping into pessimistic territory for the first time since late 2017. The February lift takes the Index back into ‘cautiously optimistic’ territory. While that may indicate some of last month’s decline was holiday season noise, the survey detail suggests the Reserve Bank’s recent shift in tone has also played a part.

The survey was in the field over the week ended February 9. That week saw a significant shift from the RBA with the Governor giving a clear signal that the Bank now has a more evenly balanced view on the next move on rates, compared to the ‘next move likely to be higher’ assessment that it maintained throughout 2018.

We get a clear picture of how this has impacted consumer expectations from an additional question, run every six months, on respondents’ outlook for mortgage interest rates. Back in August, about half of Australians expected rates to rise over the next twelve months. That proportion fell to just below 43% in this month’s survey, the lowest reading since August 2016, the last time the RBA cut official interest rates. The February survey also showed a strong 7.4% lift in sentiment amongst consumers with a mortgage, another indication that diminished rate rise fears have been a support.

Stepping back from the month to month moves, confidence continues to bear up well in the face of significant headwinds. In particular, the continued house price correction, concentrated in Sydney and Melbourne, is impacting consumer expectations for house prices but so far appears to be having only limited spillover effects on wider confidence. Sentiment amongst consumers in NSW and Victoria is holding up well, averaging in line with the readings nationally. Even views around family finances in these two states are on a par with or slightly better than their interstate peers.

Other factors are likely to be having more mixed impacts. On the negative side: an apparent slowdown in Australia’s economic growth, ongoing concerns around global trade wars, and political uncertainty ahead of the Federal election are all factors. On the positive side are: continued firm conditions across Australia’s labour market, lower petrol prices, and a solid sharemarket rebound (the S&P/ASX200 is up 7% since the December survey).

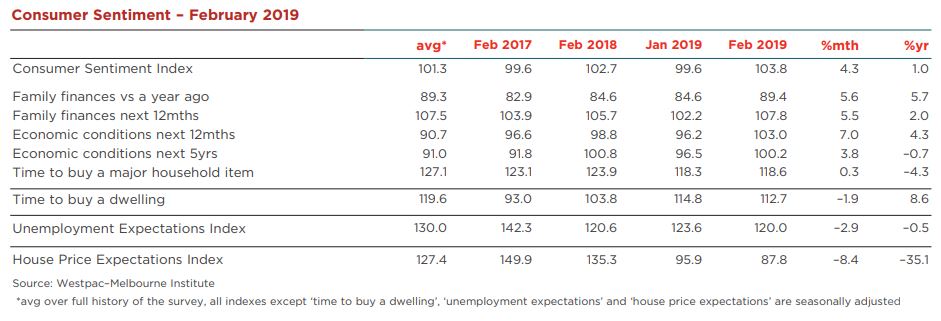

All index components recorded gains between January and February, in most cases reversing the bulk of the previous month’s decline.

On the economy, the ‘economic outlook, next 12mths’ subindex rebounded 7%, reversing most of last month’s 7.8% drop, which was the biggest fall in over three years. The ‘economic outlook, next 5yrs’ sub-index also rose 3.8%, reversing most of a sizeable 5.9% decline in January. Both sub-indexes remain slightly below their December levels but are comfortably above longer run averages. Despite the softer tone and shaky start to 2019, views on the economy remain a support for consumer sentiment.

Views on family finances remain the weak spot for consumer confidence but have improved on January’s poor start to the year. The ‘finances vs a year ago’ sub-index posted a 5.6% lift, reversing most of January’s 5.9% decline.

Consumer assessments of the outlook for family finances showed a more promising gain. The ‘finances, next 12 months’ index recorded a 5.5% rise and is the only component above its December level. At 107.8, the subindex is now a touch above its long run average and at the upper end of the range seen over the last four years. Expectations may be getting some support both from the shift in tone around interest rates and tax cuts announced in last year’s Budget and scheduled to come into effect from July this year.

Consumer attitudes towards major purchases have been steadier in recent months but remain subdued. The ‘time to buy a major household item’ sub-index rose just 0.3% in February, having dipped 1.3% in January. The sub-index remains below average, pointing to a continuation of the sluggish consumer spending growth seen through 2018.

Labour market conditions still look to be supporting confidence although expectations are no longer showing the steady improvement evident through 2016 and 2017. The Westpac-Melbourne Institute Unemployment Expectations Index – a proxy for consumers’ sense of job security – recorded a 2.9% decline in February (recall that lower reads mean more consumers expect unemployment to fall in the year ahead). At 120 the index is at a seven year low and considerably better than the long run average of 130 but is little changed on a year ago. Consumers in NSW and Vic remain more confident around jobs – likely a key source of support to wider confidence in these states – but unemployment expectations continue to show promising improvements across the mining states as well.”

Australia’s deepening housing downturn is continuing to impact consumer views around housing, price expectations in particular.

The ‘time to buy a dwelling’ index declined 1.9% in February, giving back some of January’s 4.1% gain. At 112.7 the index nationally is still up significantly on a year ago but below its long run average of 120. Improving affordability continues to see a lift in buyer sentiment in NSW and Victoria, the latter reaching a five year high in February. However, buyer sentiment is becoming more unsettled in other parts of the country with declines across all other states suggesting softening markets and tightening lending standards may be starting to affect assessments.

Consumer expectations around house prices recorded another sharp fall in February. The Westpac-Melbourne Institute Index of House Price Expectations dropped 8.4% to 87.8, marking a new record low since we began compiling this index in May 2009. Weakness remains more pronounced in NSW and Vic, with just over half of consumers in these states expecting prices to be lower in a year’s time. That said, the more positive views in other states are also starting to show signs of softening with notable pull backs in price expectations in Queensland and WA.

The Reserve Bank Board next meets on March 5. This month’s lift in consumer sentiment will be of some comfort to the Bank given its concerns around spillovers from the housing downturn. However, developments in the housing market continue to highlight downside risks to the outlook.

The recent changes to the Reserve Bank’s outlook have narrowed the gap with our own but Westpac remains more downbeat. Even so, our weaker forecasts have not been weak enough to warrant forecasting a rate cut. Accordingly, even if the RBA moves further towards Westpac’s current view, it seems likely that rates will remain on hold. The threshold for policy is whether spillovers knock the labour market off course. Our current forecasts do not incorporate that prospect but we acknowledge downside risks.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.