Back in 2016, Bernard Salt attacked the Millennial generation, claiming they’d rather spend their money on $20 smashed avocado breakfasts than making the sacrifice their parents and grandparents made to forgo consumption in order to accumulate a deposit.

The ABC has published an interesting chart series comparing age cohorts in 2016 to the same cohorts in 1981. The charts pertaining to the Millennial 31-40 cohort is particularly interesting and comprehensively debunks Salt’s profligate Millennial claim.

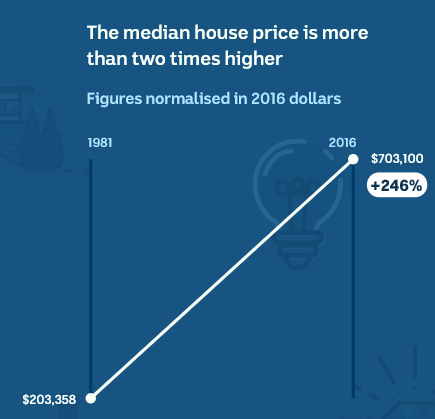

First, real median house prices were more than twice as high in 2016 as they were in 1981:

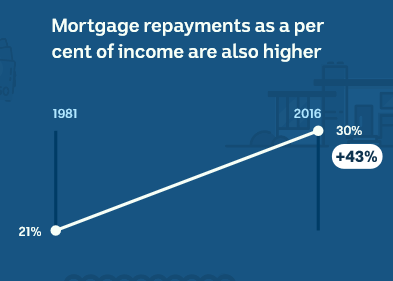

Second, mortgage repayments as a percentage of disposable income were also 43% higher:

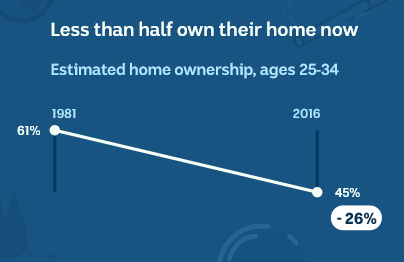

Third, home ownership rates have fallen 26%:

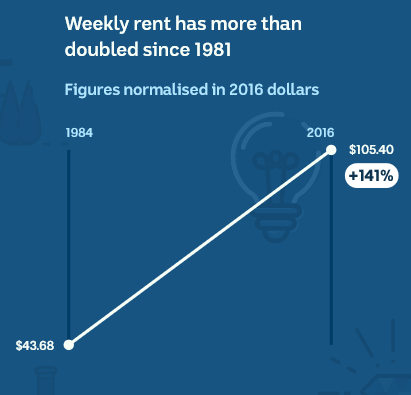

Fourth, real weekly rents have more than doubled, making saving a home deposit more difficult:

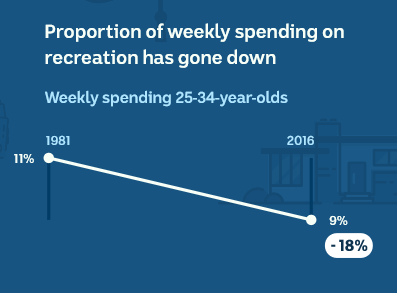

And finally, the percentage of income spent on recreation has actually fallen 18%:

In other words, Bernard Salt couldn’t be any more wrong about Millennials.