The economy is at risk of a “doozy recession” as the housing downturn accelerates at an “alarming pace” weakening consumer sentiment, warns former Morgan Stanley global strategist Gerard Minack.

Mr Minack, who is known for calling the global financial crisis, said a recession would drive cash rates to zero, 10-year bond yields to 1 per cent and the Australian dollar to $US60 cents.

The likelihood of a recession should become clear around the time of the May federal election, forcing economic management to the top of the political agenda.

Quite right. As we know, Mr Minack is a big bear on consumption:

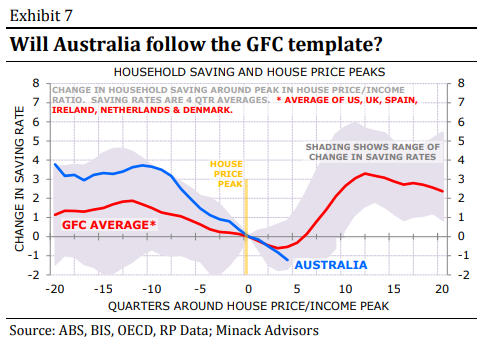

The evidence from other economies is that household saving rates typically keep falling for around a year after house prices peak relative to income. The adverse wealth effect – when household saving starts to rise – normally hits a year or two later.

Exhibit 7 shows the change in household saving rates around the house price/income peak for Australia and a selection of economies that saw significant house price declines in the GFC. On average, the household saving rate increased by 3½ percentage points over an 8 quarter period, starting one year after the peak in house prices.

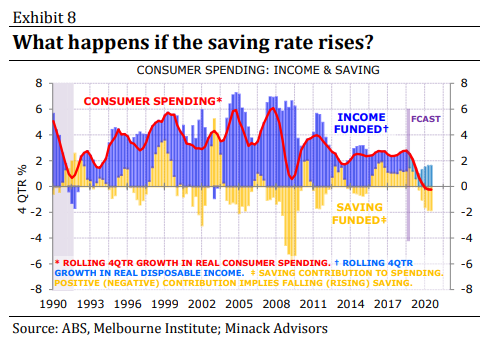

Australia is toast if it follows that pattern. Exhibit 8 shows what would happen to real consumer spending if the household saving rate rises by 3½ percentage points over the next two years. I have assumed that real household disposable income continues to rise by 1½%. Of course, that would be too optimistic: income growth would weaken if consumer spending – which accounts for over 55% of GDP – started to weaken as this scenario implies.

This illustrates the point that the wealth effect alone is capable of causing recession. The uncertainty is whether the wealth effect kicks in as powerfully as in this simple example. If the recent pattern of macro weakness – in house prices, building approvals and hiring intentions – continues, then I will make the bet that the wealth effect will cause a recession in Australia, most likely later this year.

Advertisement

I completely agree with his call on the bond bull and weakening Australian dollar which is why the MB Fund is positioned for both.

David Llewellyn-Smith is chief strategist at the MB Fund and MB Super which is long international equities and local bonds that will benefit from a weakening Australian economy and dollar so he is definitely talking his book.

Advertisement

If the ideas above interest you then contact us below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.