Outside Australia, stocks have dropped across the region as the US/NK summit ends on a whimper, cut short with no agreement. Risk markets have bid up the USD and pushed stocks down as the latest Chinese manufacturing PMI comes in lower than expected for a third month in a row.

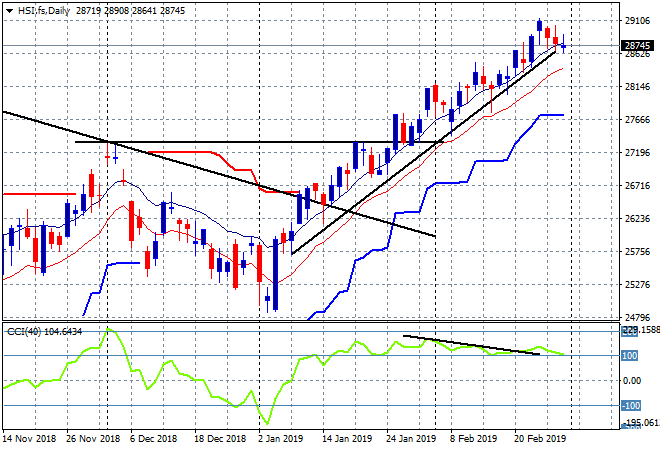

The Shanghai Composite is off nearly 1% going into the close, taking back most of the previous gains but still above 2900 points at 2936. The Hong Kong Hang Seng Index is down only 0.2% or so to be at 28700 points. The current rally remains intact , with prices remaining above the high moving average and the trendline on the daily chart, but the lack of a new daily high since the start of the week is starting to weigh:

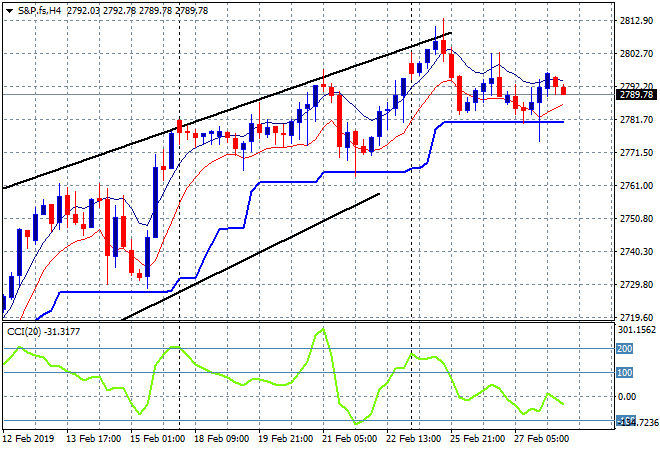

US and Eurostoxx futures are pulling back on the risk off mood with the S&P 500 remains unable to break through the psychologically important 2800 point level that has been staunch resistance all week:

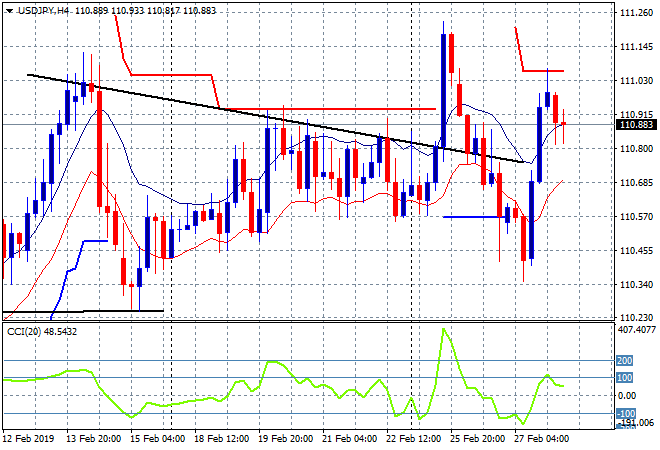

Japanese stock markets pulled back the most as the weaker move in Yen overnight did not translate into further slides today as the Nikkei 225 closed 0.8% lower to 21385 points, but still above previous key resistance. The USDJPY pair has retreated a little after last night’s sudden reversal, blipping just below the 111 handle and possibly setting up for further falls tonight due to the lack of a new session high:

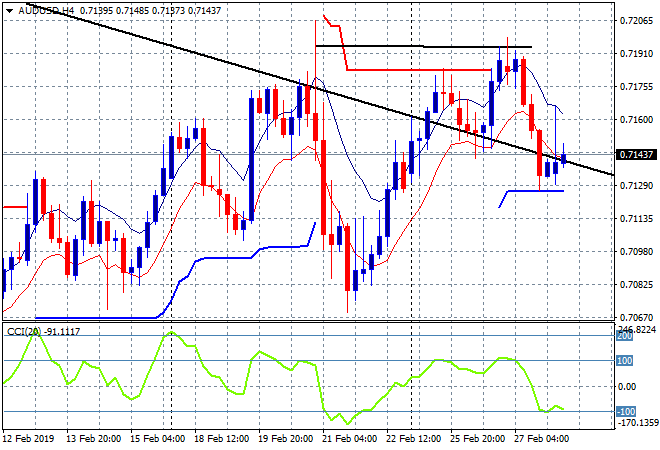

The ASX200 is the only market in the green, launching on the good mood around the Capex figures and the lower Aussie dollar as a result, closing 0.3% higher to 6168 points, still well above the key 6100 point resistance level. The Australian dollar went through a spike and then a reversal on the back of the capex numbers and then the Chinese PMI prints and is hovering just above ATR support at the 71.40 level going into the City open:

The economic calendar has two major releases of note tonight, first the January EZ wide CPI print, then the 4Q US GDP print.