Independent economist Gerard Minack has released a report explaining why he thinks “a recession in Australia is becoming more likely”.

In the report, Minack notes a number of downside risks, including:

The accelerating decline in dwelling values;

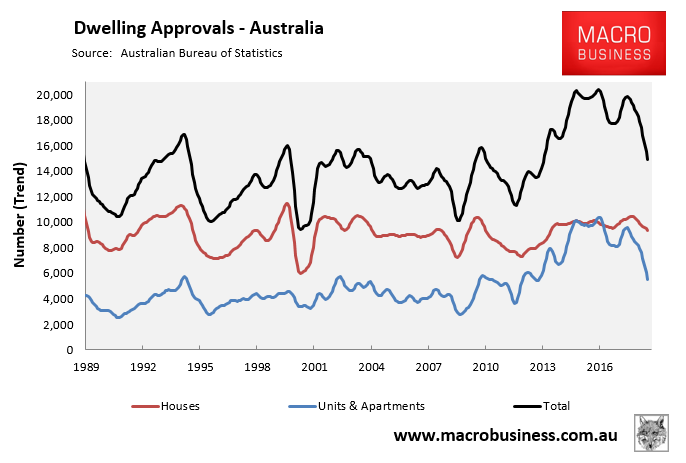

The accelerating decline in building approvals;

Leading indicators of employment are weakening; and

The negative wealth effect.

Advertisement

While these factors are nothing new to readers of MB, it’s Minack’s analysis of the household savings rate that is most alarming:

The evidence from other economies is that household saving rates typically keep falling for around a year after house prices peak relative to income. The adverse wealth effect – when household saving starts to rise – normally hits a year or two later.

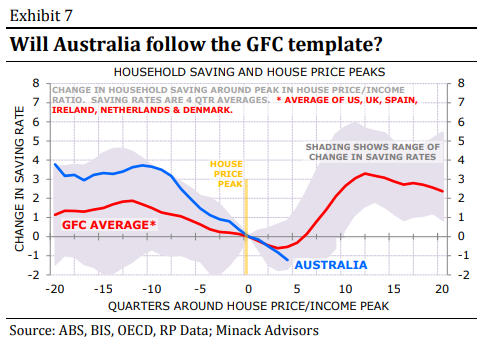

Exhibit 7 shows the change in household saving rates around the house price/income peak for Australia and a selection of economies that saw significant house price declines in the GFC. On average, the household saving rate increased by 3½ percentage points over an 8 quarter period, starting one year after the peak in house prices.

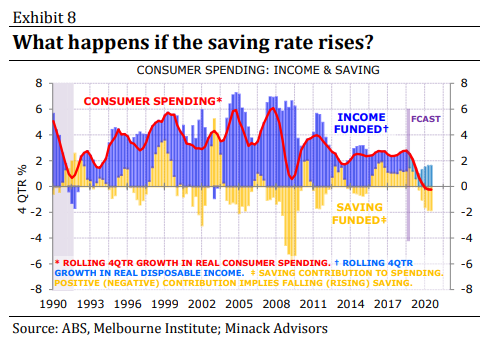

Australia is toast if it follows that pattern. Exhibit 8 shows what would happen to real consumer spending if the household saving rate rises by 3½ percentage points over the next two years. I have assumed that real household disposable income continues to rise by 1½%. Of course, that would be too optimistic: income growth would weaken if consumer spending – which accounts for over 55% of GDP – started to weaken as this scenario implies.

This illustrates the point that the wealth effect alone is capable of causing recession. The uncertainty is whether the wealth effect kicks in as powerfully as in this simple example. If the recent pattern of macro weakness – in house prices, building approvals and hiring intentions – continues, then I will make the bet that the wealth effect will cause a recession in Australia, most likely later this year.

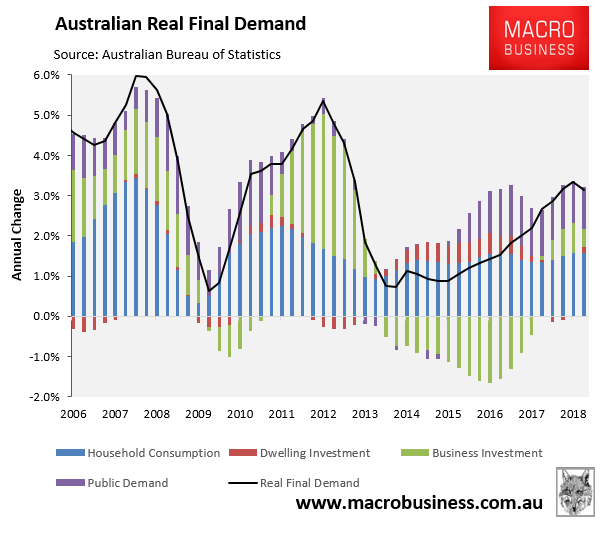

The below chart shows the four drivers of real final demand:

Advertisement

As at September 2018, these drivers were:

Household Consumption: 57% share;

Dwelling Investment: 6% share;

Public Demand: 24% share;

Business Investment: 13% share.

Dwelling investment is now falling, and will subtract from growth over the next few years:

Advertisement

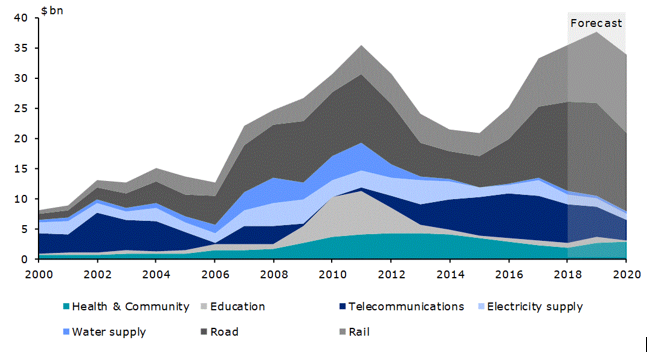

Whereas infrastructure investment to peak at $40 billion this year and then fall into 2020:

Advertisement

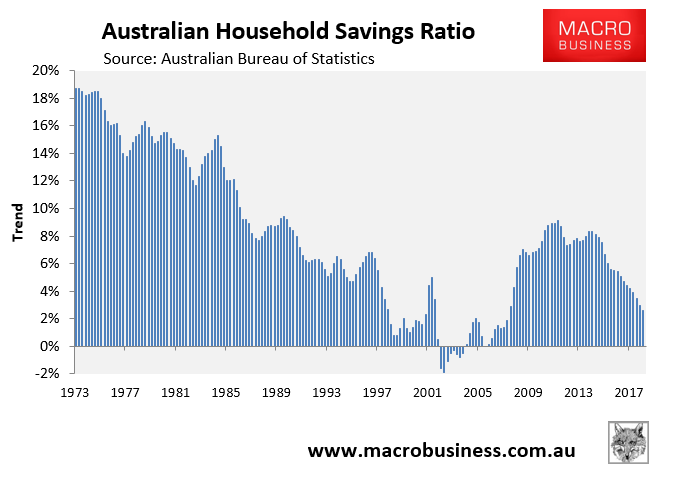

However, as pointed out by Minack, the big kicker is household consumption. Consumption has so far held-up by falling savings amid weak income growth, which is clearly not sustainable:

As the savings rate normalises, it will necessarily drain on household consumption, removing Australia’s key growth driver and raising the real prospect of recession.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.