The ABS is out with December quarter private capex and the news is pretty good:

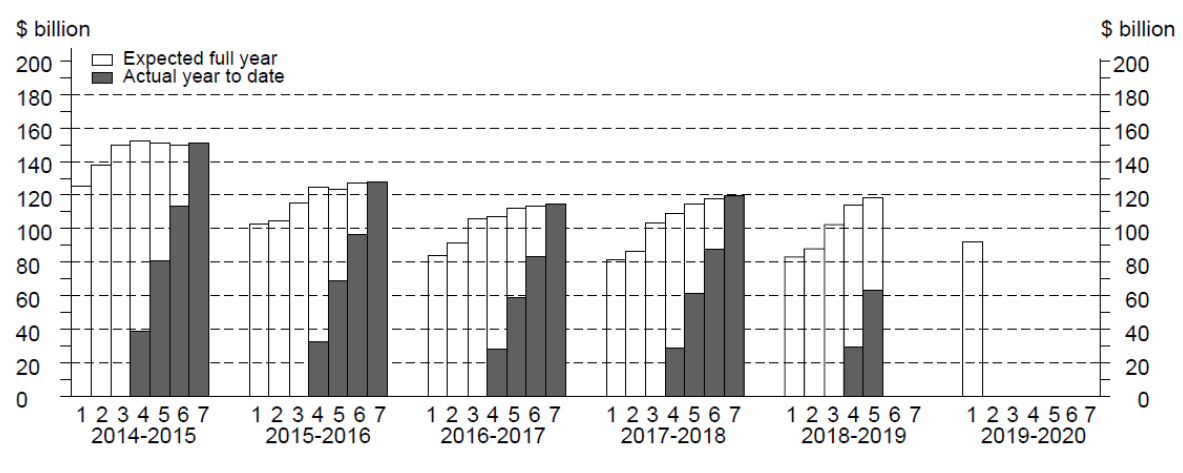

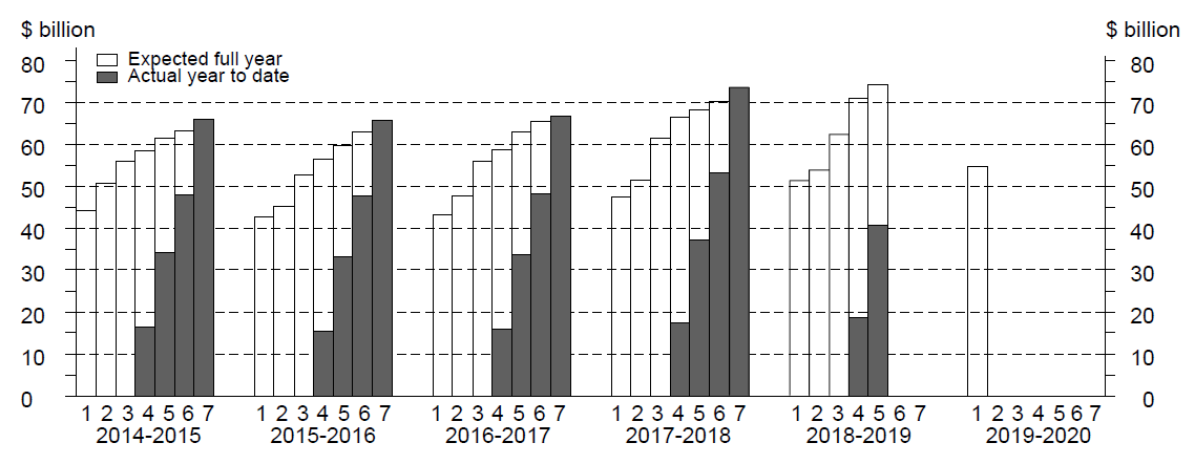

TOTAL CAPITAL EXPENDITURE

Estimate 5 for total capital expenditure for 2018-19 is $118,361m. This is 3.6% higher than Estimate 5 for 2017-18. The main contributor to the increase is Other Selected Industries (8.9%). Estimate 5 is 4.0% higher than Estimate 4 for 2018-19. The main contributor to the increase was Other Selected Industries (4.8%).

Estimate 1 for total capital expenditure for 2019-20 is $92,144m. This is 11.0% higher than Estimate 1 for 2018-19. The main contributor to the increase was Mining (21.4%).

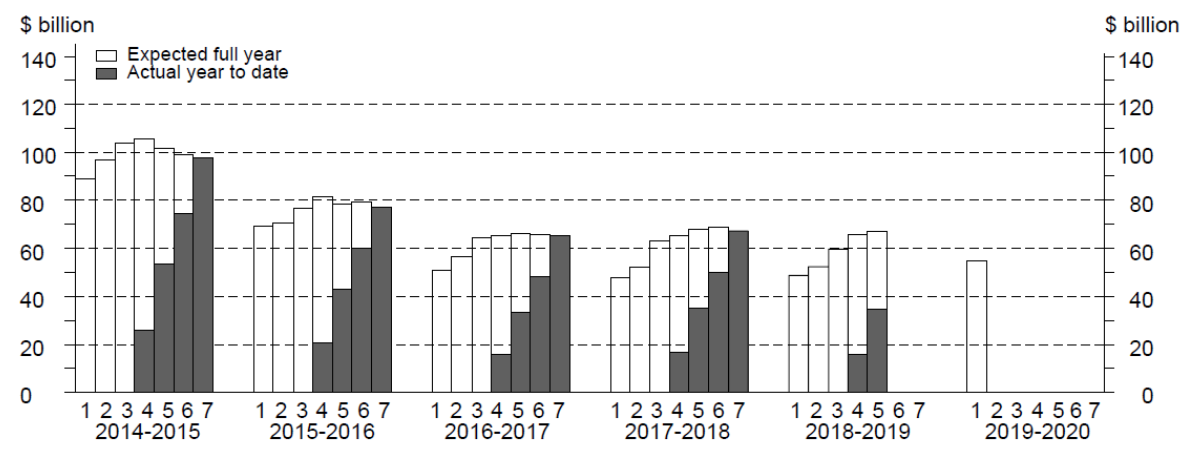

BUILDINGS AND STRUCTURES

Estimate 5 for buildings and structures for 2018-19 is $66,927m. This is 1.4% lower than Estimate 5 for 2017-18. The main contributor to the decrease is Mining (13.3%). Estimate 5 is 1.6% higher than Estimate 4 for 2018-19. The main contributor to the increase was Mining (4.5%).

Estimate 1 for buildings and structures for 2019-20 is $54,732m. This is 12.6% higher than Estimate 1 for 2018-19. The main contributor to the increase was Mining (22.4%).

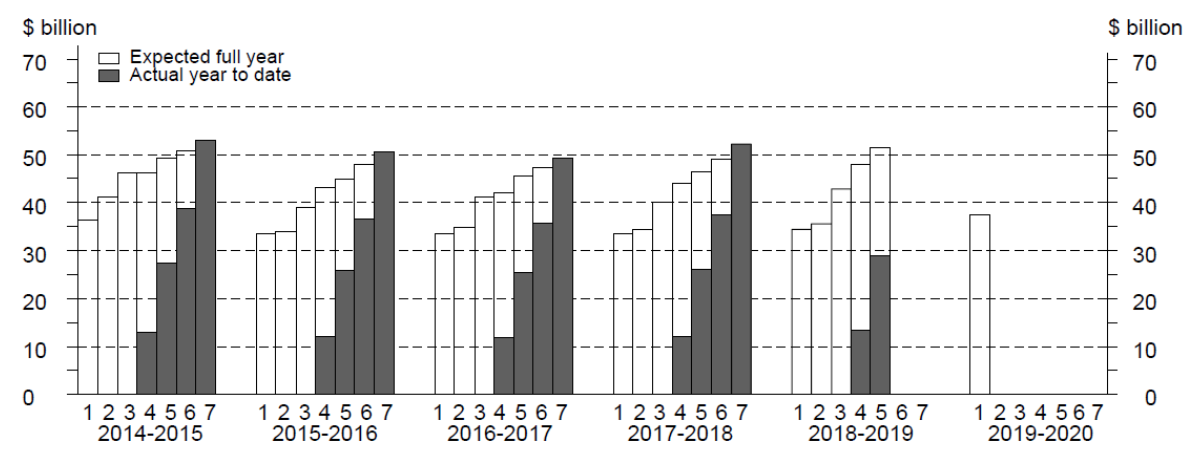

EQUIPMENT, PLANT AND MACHINERY

Estimate 5 for equipment, plant and machinery for 2018-19 is $51,434m. This is 10.8% higher than Estimate 5 for 2017-18. The main contributor to this increase is Other Selected Services (9.2%). Estimate 5 is 7.3% higher than Estimate 4 for 2018-19. The main contributor to the increase is Other Selected Industries (10.5%).

Estimate 1 for equipment, plant and machinery for 2019-20 is $37,412m. This is 8.8% higher than Estimate 1 for 2018-19. The main contributor to the increase was Mining (18.8%).

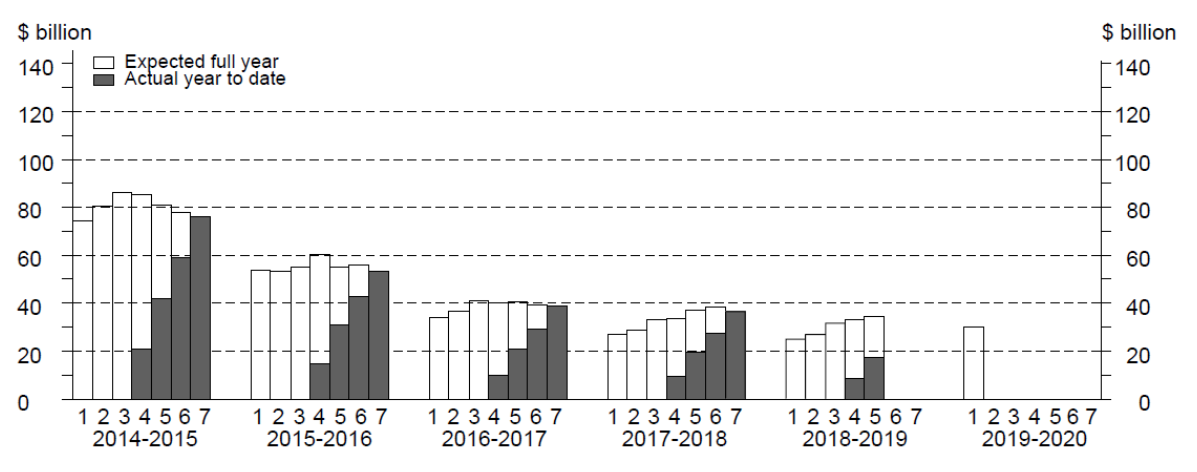

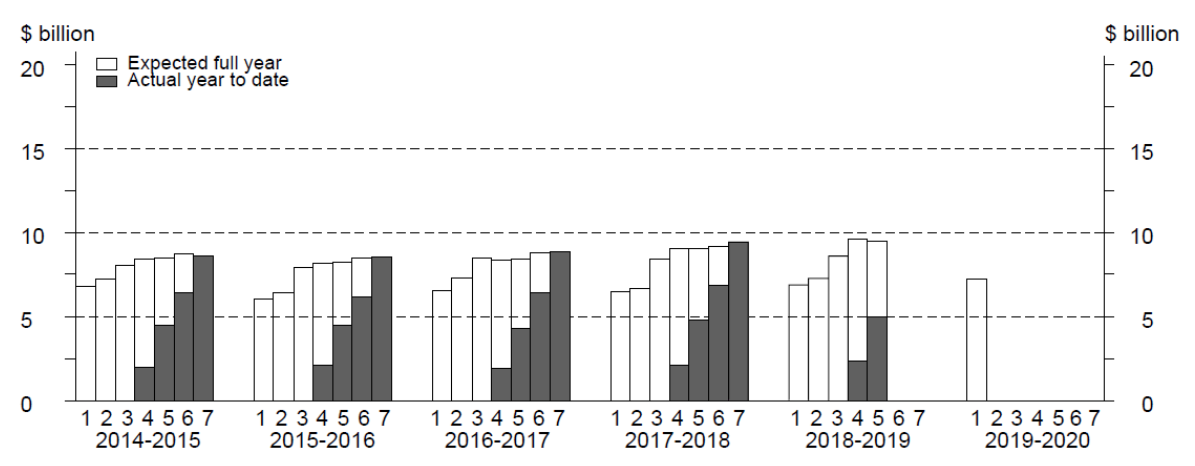

MINING

Estimate 5 for Mining for 2018-19 is $34,446m. This is 6.8% lower than Estimate 5 for 2017-18. Estimate 5 is 3.8% higher than Estimate 4 for 2018-19. Buildings and structures is 4.5% higher and equipment, plant and machinery is 1.6% higher than the corresponding fourth estimate for 2018-19.

Estimate 1 for Mining for 2019-20 is $30,161m. This is 21.4% higher than Estimate 1 for 2018-19. Buildings and structures is 22.4% higher and equipment, plant and machinery is 18.8% higher than the corresponding first estimate for 2018-19.

MANUFACTURING

Estimate 5 for Manufacturing for 2018-19 is $9,528m. This is 5.2% higher than Estimate 5 for 2017-18. Estimate 5 is 1.2% lower than Estimate 4 for 2018-19. Buildings and structures is 3.2% lower and Equipment, plant and machinery is 0.4% lower than the corresponding fourth estimate for 2018-19.

Estimate 1 for Manufacturing for 2019-20 is $7,246m. This is 5.2% higher than Estimate 1 for 2018-19. Equipment, plant and machinery is 8.2% higher and Buildings and structures is 1.4% lower than the corresponding first estimate for 2018-19.

OTHER SELECTED INDUSTRIES

Estimate 5 for Other Selected Industries for 2018-19 is $74,363m. This is 8.9% higher than Estimate 5 for 2017-18. Estimate 5 is 4.8% higher than Estimate 4 for 2018-19. Equipment, plant and machinery is 10.5% higher and buildings and structures is 0.1% higher than the corresponding fourth estimate for 2018-19.

Estimate 1 for Other Selected Industries for 2019-20 is $54,736m. This is 6.8% higher than Estimate 1 for 2018-19. Buildings and structures is 7.6% higher and equipment, plant and machinery is 5.7% higher than the corresponding first estimate for 2018-19.

I’ll be back shortly with the actual capex data, which feeds into the Q4 national accounts.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.