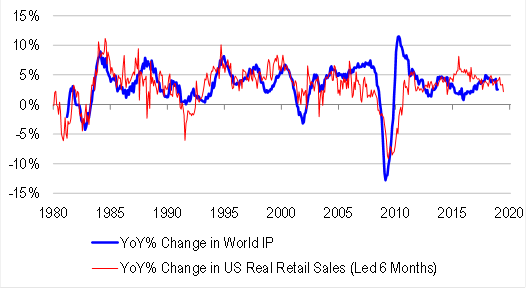

Via Damien Boey at Credit Suisse:

Overnight, we received very disappointing US retail sales data. Headline nominal sales fell by 1.2% over the month, their sharpest monthly decline since the financial crisis. Notwithstanding ongoing strong job creation, consumption weakened on the back of low confidence and market turbulence.