DXY rebounded a little overnight. EUR was weak and CNY surged:

The Aussie dollar is tracking CNY:

EMs even more:

Advertisement

Gold to the moon:

Oil fell:

Base metals beginning to show life:

Advertisement

Big Miners cock-a-hoop:

EM stocks have broken out:

Led by junk:

Advertisement

And a big bid for Treasuries:

As well as bunds at the long end:

Stocks love it:

Advertisement

Westpac has the detail:

Event Wrap

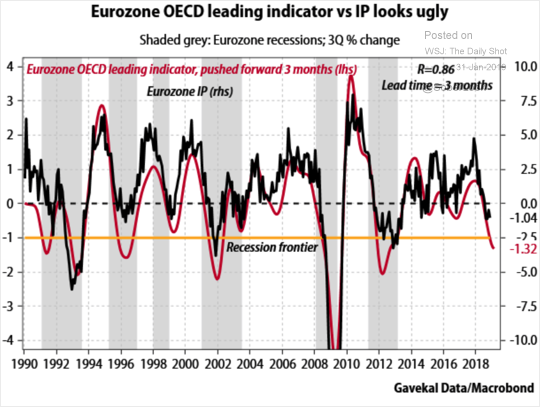

Although Eurozone Q4 GDP met, admittedly low, expectations of +0.2%q/q (1.2%y/y), market attention was grabbed by the confirmation of technical recession in Italy where Q4 GDP’s -0.2%q/q (est. was -0.1%q/q) followed Q3’s -0.1%. Concerns over Italy’s budget proposals submitted in Q4 2018 are about the Government’s projection for relatively sound growth in 2019. Politics in Italy is continuing to bubble. Recently Salvini and his right wing League have intimated the advantages of another election. Today Berlusconi suggested that a centre-right allegiance could sweep away the populist 5-Star even without an election.

Earlier German retail sales for December fell a sharp -4.3%m/m (est. -0.6%m/m). This was much more than can be explained by a distortion due to Black Friday boosting sales in November.

Bundesbank and ECB’sWeidmann acknowledged the low growth potential for Germany in 2019 but asserted that growth would return to its expansion course in 2020 and 2021.

Event Outlook

Australia: Jan CoreLogic home value index is expected by Westpac to decline 1.0%, continuing the downtrend. Jan AiG PMI is released after the index slipped to 49.5 in Dec – the first contraction in 26 months.

Japan: Dec jobless rate is expected to remain very low at 2.5%.

China: Jan Caixin PMI follows yesterday’s NBS reading which showed a still subdued manufacturing index but a jump in non-manufacturing.

Euro Area: Jan CPI is anticipated to show annual headline inflation decline to 1.4% from 1.6% due to energy prices while core inflation remains at 1.0%.

US: Jan non-farm payrolls are expected to rise 165k following the very strong read in Dec. The unemployment rate is seen to hold at 3.9% with average hourly earnings annual growth also unchanged at 3.2%.

And Charlie McElligot at Nomura has the reflexivity:

The steepening is the longer-term catalyst for U.S. Equities “Value” factor market-neutral as funds rebalance portfolios into the “end of cycle / start of next cycle” trade (long “Value,“ short “Growth” as steeper curve “bleeds” the prior funding-advantage of now-EXPENSIVE Growth companies in a flattening curve environment, and further down-the-road as we approach easing, we see “Value Longs” work, which are economically-sensitive / very Cyclical which respond to easier FCI)—also worth again noting that the steepening too is a powerful headwind for “Momentum” factor as well

The curve steepening is the core then to my favorite risk-book hedge, 1Y expiry 5s30s curve cap options contingent with SPX lower (we have this flow, and doing it contingent with SPX cuts the price in half)

The dovish capitulation is driving a massive move lower in U.S. Real Yields and U.S. Dollar, which means another impulse higher for Gold

For the same “lower USD / lower real U.S. Real Yields” catalysts, we are SUPER bulled-up on market-neutral (+) EEM / (-) SPY expression on the EM / DM convergence trade

A similar (but even “saucier”) thesis with additional “High Beta-” and “Value / Growth-” kickers is (+) FXI / (-) QQQ

Also juicing the rally, there is this, via Sinocism:

Advertisement

President Trump took to Twitter Thursday morning to tell us that the trade talks are progressing and that he will be meeting Xi Jinping soon:

Donald J. Trump@realDonaldTrumpChina’s top trade negotiators are in the U.S. meeting with our representatives. Meetings are going well with good intent and spirit on both sides. China does not want an increase in Tariffs and feels they will do much better if they make a deal. They are correct. I will be……

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

China’s top trade negotiators are in the U.S. meeting with our representatives. Meetings are going well with good intent and spirit on both sides. China does not want an increase in Tariffs and feels they will do much better if they make a deal. They are correct. I will be……