The big data release of the night was a US retail shocker:

Advertisement

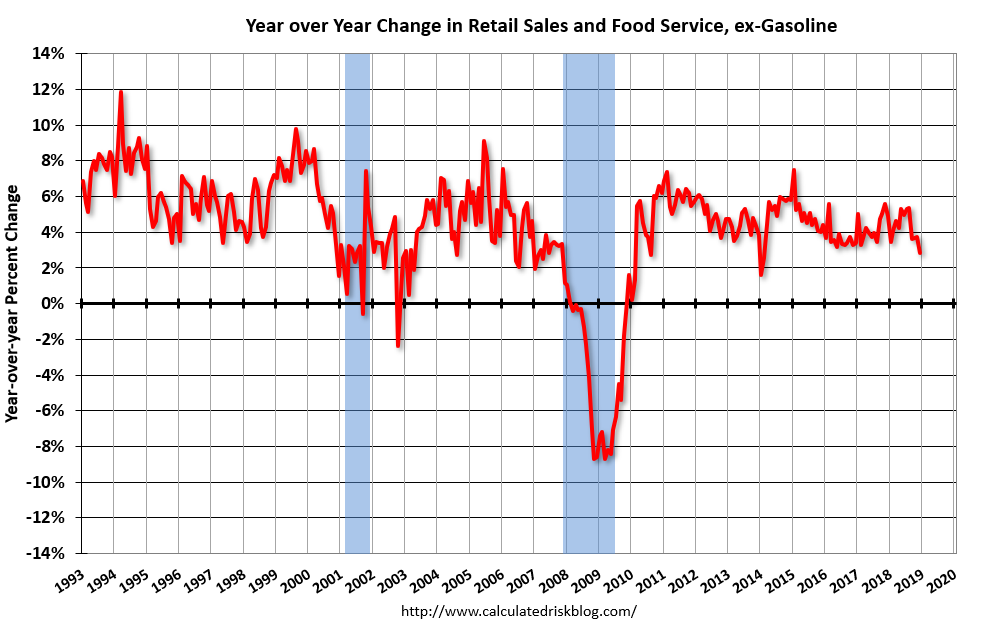

Advance estimates of U.S. retail and food services sales for December 2018, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $505.8 billion, a decrease of 1.2 percent from the previous month, but 2.3 percent above December 2017.

Looks like stock market jitters to me. With the shutdown to follow in January it might be weak as well. More such data will obvious pressure the USD.

Advertisement

But the main story remains Europe. Westpac weighs in with an assessment of its slowdown:

Concerns over world growth are a clear factor behind the recent realignment of central bank policy expectations. One of the early signs of easing momentum was in the Euro Area where an abrupt shift lower in external demand saw growth come off significantly. As such, an assessment of the Euro Area is paramount to gauging the current balance of risks for global output.

Today’s Euro Area Q4 GDP 2nd estimate of 0.2% growth indicates a subdued end to 2018. For the year in total, annual average growth printed at 1.8%, compared to the ECB’s projection made at the end of 2017 for 2.3% growth, which followed 2017’s strong 2.5% performance. While we won’t know the exact expenditure breakdown for 2018 until the 3rd estimate, our forecasts based on the first three quarters and preliminary information indicate domestic demand slowed to 1.6% from 1.9%, but more significantly, the contribution from net exports fell to 0.2ppts from 0.8ppts.

Equally of stark contrast between 2018 and 2017 is the dispersion of growth across Euro Area members. From weakest to strongest: Italy contracted through the second half of 2018, Germany stalled, France managed to eke out moderate gains, whereas Spain pushed ahead with strength. Some of the drivers behind this desynchronisation may be temporary (automotive sector disruption and Rhine levels in Germany) and others could last for longer (fiscal uncertainty in Italy and political unrest in France).

Yet, despite the drama over the year, the Euro Area unemployment rate declined to 7.9% from 8.6%. Employment grew by just over 1 per cent through the year whereas the labour only grew around a ¼ per cent. Here, there are two take-outs: a) the rate of employment growth needed to see a lower unemployment rate isn’t that high and b) lower growth than in the past is structural. Even if employment growth in 2019 were to fall to 0.3% due to slower GDP growth, it should still see unemployment down to 7.8% (7.3% is the historical low) and support wages with compensation per employee growth having already risen to 2.5%.

But perhaps we are getting ahead of ourselves? In a time of high geopolitical uncertainty, the confidence band around point estimate forecasts are naturally much wider. Indeed, the European Commission lowered their 2019 annual average growth forecast to 1.3% from 1.9% in November, and the ECB have acknowledged risks have moved to the downside of their 1.7% forecast.

While Westpac’s forecast for 2019 was only slightly lowered to 1.4% at the start of this year, compared to our 1.6% forecast as at March 2018, that is not to say we have not been surprised by recent data. Of particular concern is the 2.5% fall in industrial production in Q4 equating to a 3.9% decline through 2018. Historically, a sustained contraction in industrial production coincides with a downturn in overall growth and early evidence suggests continued softness in the start of 2019.

Yet in that regard, another factor that coincides with an impending downturn has so far not occurred – a slowdown in lending growth. Instead, lending to households and businesses has continued at a moderate pace, and interest rates remain low. Broader financial conditions are favourable, bar higher sovereign rates in Italy. Correspondingly, for the expansion in GDP to continue, the ECB needs to maintain supportive financial conditions.

In June 2020, the first operation of the ECB’s TLTRO-II (Targeted Long-Term Refinancing Operations) reaches maturity. The amount maturing is around half of the total value of the four operations. More pressingly, the implications of its expiry would be felt by June 2019, as its time to maturity falls below one year and will therefore impact regulatory stable funding ratios.

This is significant. The ECB’s ending of net asset purchases was not policy tightening; letting TLTRO’s lapse would be. Given their importance to the transmission of policy rates, we believe the path of least resistance is to extend the operations’ maturity dates. However, that would not signal the ECB is giving up on raising the deposit rate, and we continue to believe December 2019 is the most likely date for a first hike in a very gradual return to zero.

Barring a big new Chinese stimulus to lift Europe’s external demand, I see the ECB doing a new TLTRO and no rate hikes. That means a strong USD and a weak AUD.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.