DXY was firm Friday night. EUR too but CNY reversed sharply:

AUD fell back against DMs:

But was stronger than EMs:

Advertisement

CFTC positioning was out for the fist time in six weeks and showed another pullback in AUD shorts to -31k shifting into Xmas. The missing reports will be dropped out over the next four weeks. My bet is we’ll be headed back to a more neutral position. If so it’ll be good news for bears:

Gold flamed out:

Advertisement

Oil was strong as the US rig count fell:

Base metals have become reflation believers:

Big miners are well ahead:

Advertisement

EM stocks reversed:

And junk:

Along with hosed Treasuries:

Advertisement

But bunds rallied:

Stocks were stable:

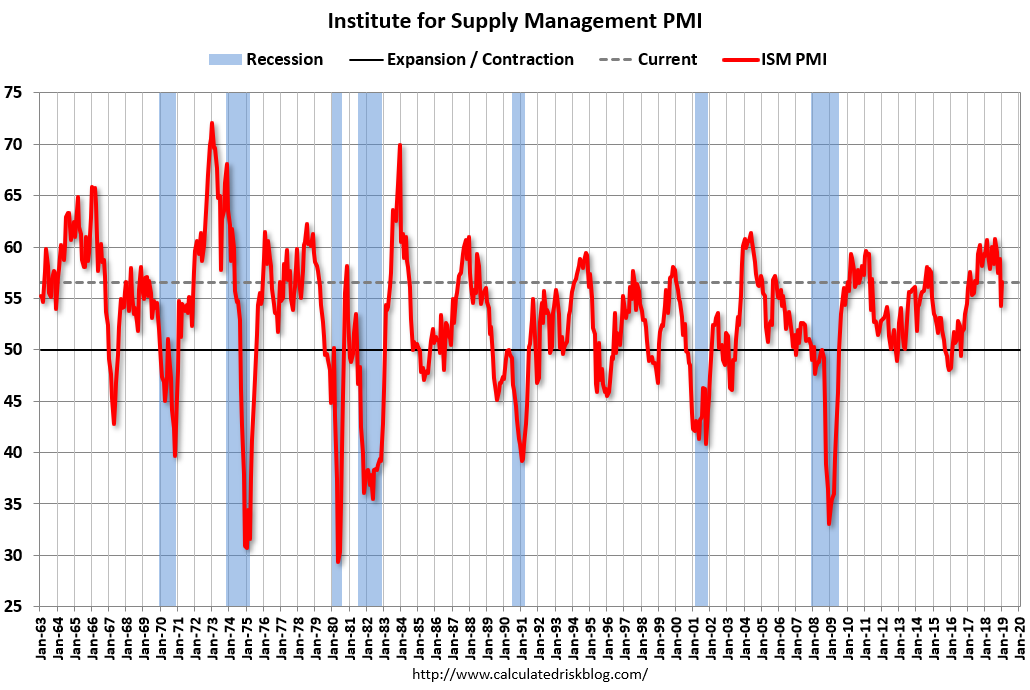

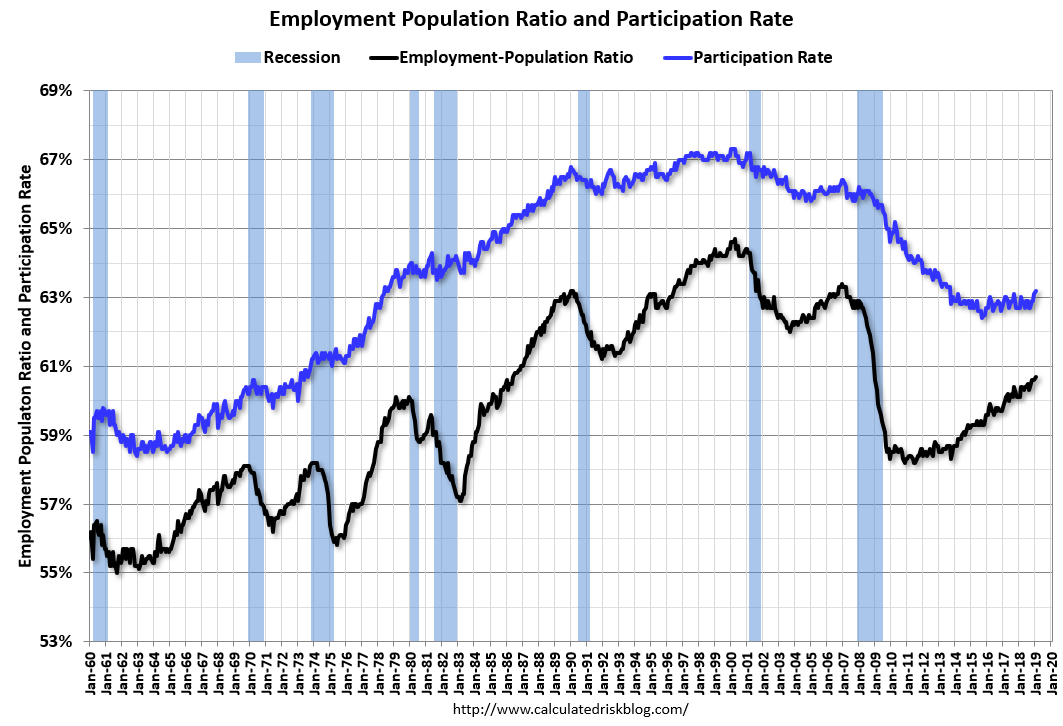

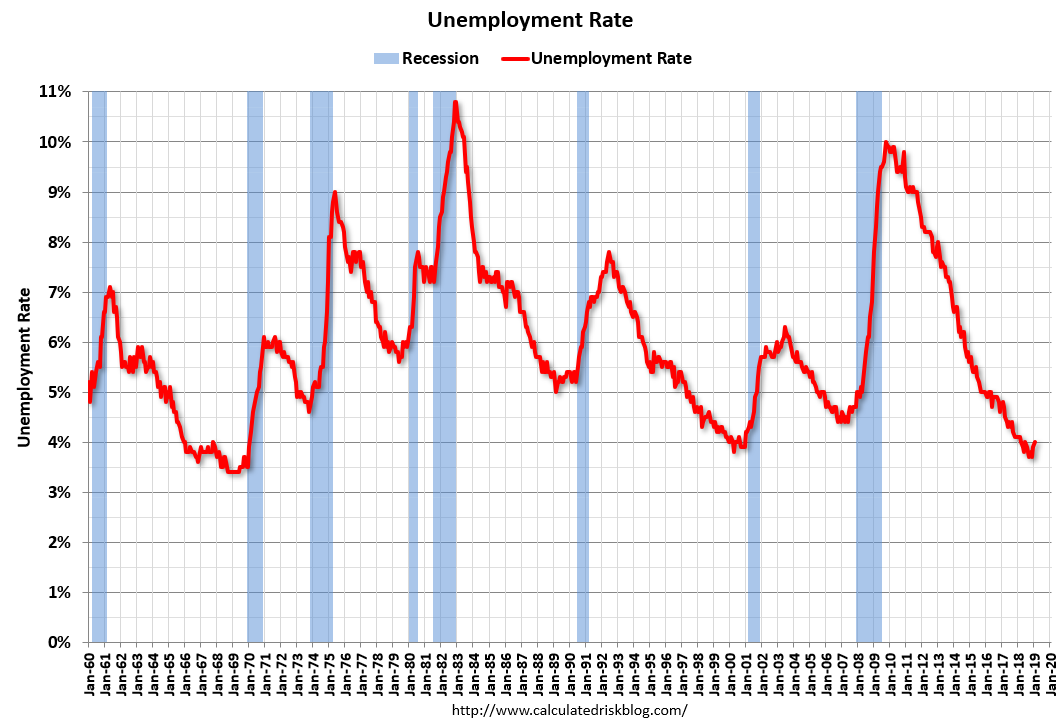

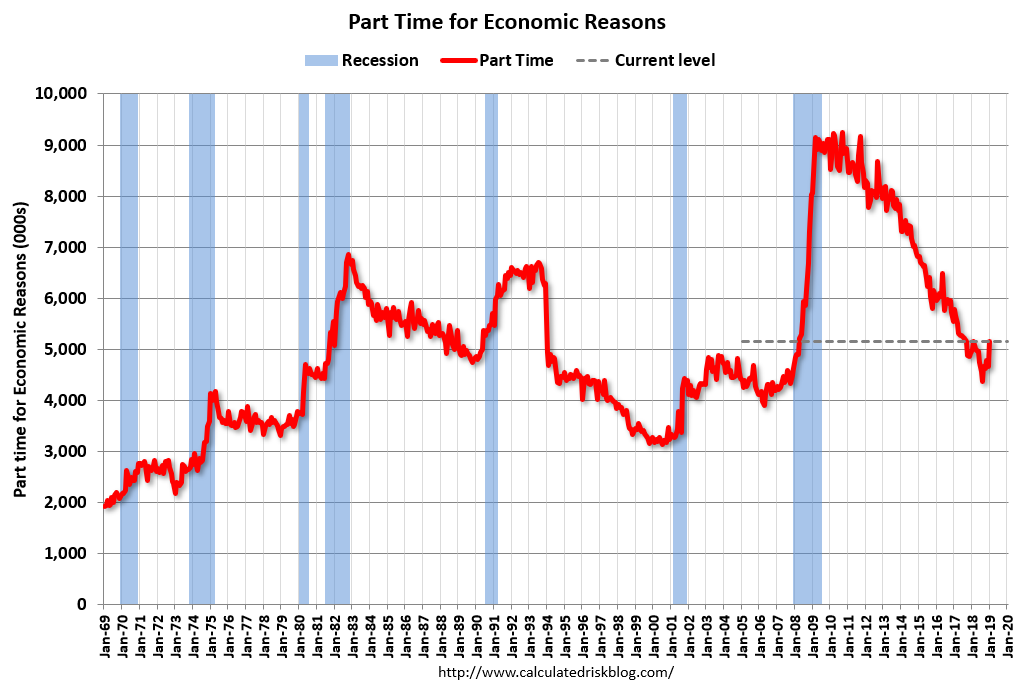

The big data releases for the night were US payrolls and the ISM, both of which were impressive. The ISM jumped on new orders (charts from Calculated Risk):

Advertisement

The January PMI® registered 56.6 percent, an increase of 2.3 percentage points from the December reading of 54.3 percent. The New Orders Index registered 58.2 percent, an increase of 6.9 percentage points from the December reading of 51.3 percent. The Production Index registered 60.5 percent, 6.4-percentage point increase compared to the December reading of 54.1 percent. The Employment Index registered 55.5 percent, a decrease of 0.5 percentage point from the December reading of 56 percent. The Supplier Deliveries Index registered 56.2 percent, a 2.8 percentage point decrease from the December reading of 59 percent. The Inventories Index registered 52.8 percent, an increase of 1.6 percentage points from the December reading of 51.2 percent. The Prices Index registered 49.6 percent, a 5.3-percentage point decrease from the December reading of 54.9 percent, indicating lower raw materials prices for the first time in nearly three years.

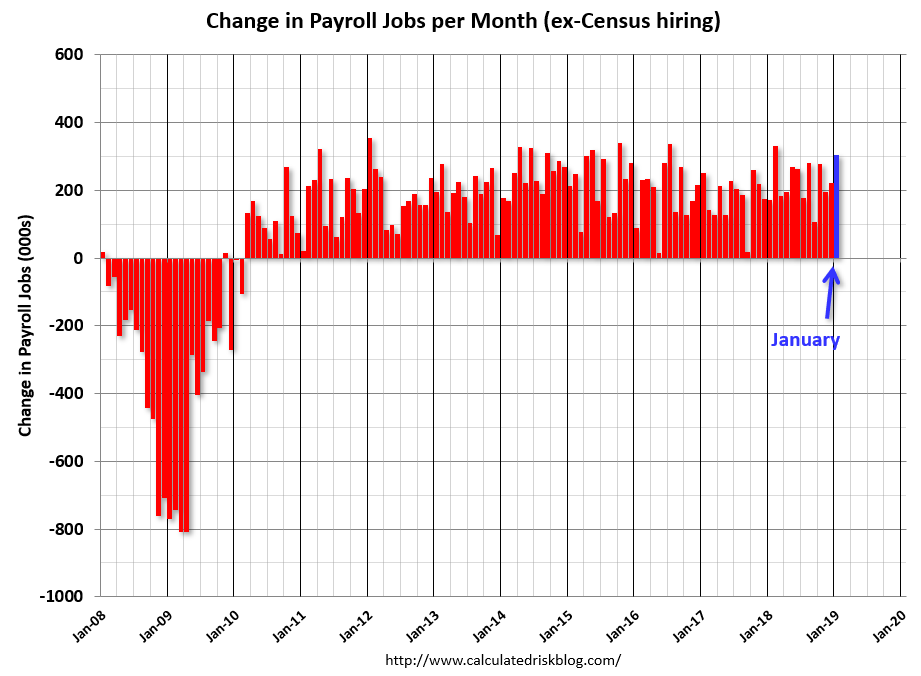

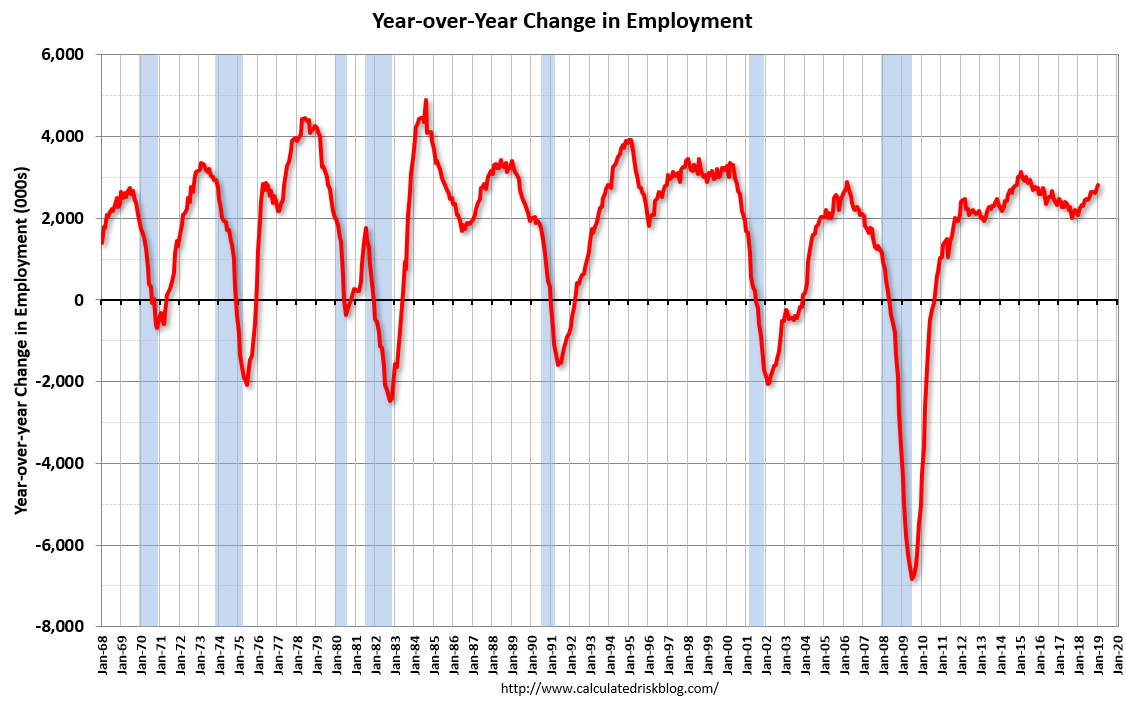

And employment jumped period:

Total nonfarm payroll employment increased by 304,000 in January, and the unemployment rate edged up to 4.0 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in several industries, including leisure and hospitality, construction, health care, and transportation and warehousing.

… Both the unemployment rate, at 4.0 percent, and the number of unemployed persons, at 6.5 million, edged up in January. The impact of the partial federal government shutdown contributed to the uptick in these measures. Among the unemployed, the number who reported being on temporary layoff increased by 175,000. This figure includes furloughed federal employees who were classified as unemployed on temporary layoff under the definitions used in the household survey.

…The change in total nonfarm payroll employment for November was revised up from +176,000 to +196,000, and the change for December was revised down from +312,000 to +222,000. With these revisions, employment gains in November and December combined were 70,000 less than previously reported.

…In January, average hourly earnings for all employees on private nonfarm payrolls rose by 3 cents to $27.56, following a 10-cent gain in December. Over the year, average hourly earnings have increased by 85 cents, or 3.2 percent.

Very impressive headline numbers given the shutdown:

Advertisement

Strong employment growth:

A rising participation rate:

Which lifted the unemployment rate:

Advertisement

The shutdown showed up in part time:

And wages growth eased:

This is not a market to take lightly this year. It is strong. Another month or two like that Fed hikes will return for mid-year.

Advertisement

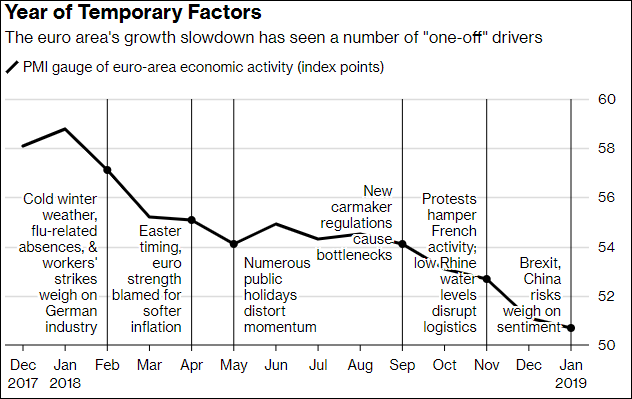

It was enough to stall the Australian dollar advance without really kicking it too hard. The reason the US dollar didn’t take off is the Fed’s new “patience” narrative. However, the other overnight data in Europe shows that DXY is going to come under further external upwards pressure soon via a weakening EUR. The zone’s PMI was toast:

Inflation is weakening fast at 1.4% with the oil shock though core lifted a touch to 1.1%:

Is the ECB reaching the end of its rope by brushing aside weaker growth on ‘temporary factors’? After a whole year of hearing it, is it time to retire that narrative?

If the central bank decides to revise its rate guidance in March, that’s when you know that they are no longer able to keep brushing aside the slowdown in the Eurozone economy as being ‘temporary’.

The latest signs aren’t looking good as Italy is posting recession-like growth while Germany’s factory activity slumps into contraction territory. And when you see a hawk like Weidmann start turning against the narrative, it just feels like the central bank and lawmakers have to start accepting reality at this point.

The ECB has continuously brushed aside the slowdown on “one-off factors”, but it is a narrative that is growing stale and markets aren’t buying it anymore. Inflation expectations in the Eurozone has fallen to two-year lows while rate hike expectations have been scaled back and in my view they are in no position to normalise policy at all this year.

After Germany’s latest retail sales slump, which the German stats office is blaming on “a growing preference for gift vouchers”, it shows that policymakers and lawmakers aren’t ready to change their language just yet.

But the longer this drags on and the more that the trend continues to point towards a further slowdown, the ECB is surely running out of reasons already to keep avoiding the reality of the situation.

Advertisement

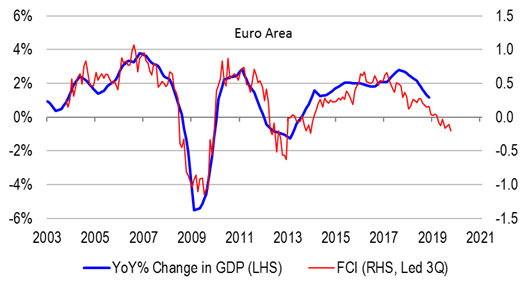

Yep. The ECB is the only central bank that is dumber and slower moving than the RBA. Its outlook is getting worse not better, via Credit Suisse comes the leading financial conditions index:

The ECB will have to flip dovish.

Advertisement

As we have been saying over and again, the US remains the growth leader and will all year despite slowing. The current move to EMs, commodities and risk assets like the Australian dollar is premature to say the least.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. The fund is positioned to benefit from a falling Australian dollar and rising bond values so he is definitely talking his book.

If these themes are of interest to you for your direct investment or super then contact us below:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.