DXY was weak last night. EUR is struggling. The source of global alarm, China, is seeing a rising currency for no apparent reason:

The Australian dollar was thumped versus DMs:

But not so much as EMs:

Gold keeps rallying on Fed hopes:

Oil appears to be rolling:

Base metals remain unimpressive:

Big miners are better ex-Vale:

EM stocks are threatening to break out of a double bottom pattern:

Likewise junk:

Treasuries were bid:

The bund curve keeps flattening:

Stocks took it on the chin:

News of evening was dominated by a couple of China-related profit warnings. Caterpillar and Nvidia blamed China, Yahoo:

U.S. stocks slumped on Monday, as warnings from Caterpillar Inc (CAT.N) and Nvidia Corp (NVDA.O) added to concerns about a slowing Chinese economy and tariffs taking a toll on corporate profits.

Shares of Caterpillar, the world’s largest heavy equipment maker, fell 9.3 percent after its quarterly profit widely missed Wall Street estimates, hit by softening demand in China and higher manufacturing and freight costs.

Nvidia tumbled 13.8 percent after the chipmaker cut its fourth-quarter revenue estimate by half a billion dollars on weak demand for its gaming chips in China and lower-than-expected data centre sales.

“Every time we get earnings stating China as a problem, investors start to realize that issues with China are going to spread and without China growing at a good clip it will be hard for the global economy and the U.S. to continue an expansion,” said Ryan Nauman, market strategist at Informa Financial Intelligence in Zephyr Cove, Nevada.

Capital Economics asks if the global slowdown is more serious than thought:

Annual gatherings, like those in Davos last week, tend to produce little in the way of meaningful policy shifts, but they can be a useful way of gauging the mood about the global economy. This year it was decidedly gloomy. The IMF grabbed the headlines by pulling down its forecast for global GDP growth in 2019 from 3.7% to – wait for it – 3.5%. As it happens, our forecasts are more bearish – we expect the world economy to grow by 3.0% this year and just 2.8% in 2020. The latter would be the slowest pace of expansion since the global financial crisis.

This slowdown has started to show up in the economic data, including another batch of weaker trade figures from Asia last week and sharp falls in the business surveys in Europe. The simple explanation for all of this is that country-specific factors are causing growth to slow in each of the world’s major economic regions.

In China, the lagged effect of earlier policy tightening is still pulling down credit growth, which in turn is weighing on activity in the real economy. In Europe, problems in Italy have been compounded by disruption to vehicle production caused by new emissions tests, and a rise in inflation that has dragged on real incomes.

The data from the US have held up for now, but we expect the economy to slow further over the course of 2019 as the sugar-high from last year’s fiscal stimulus wears off and the lagged effects of monetary tightening start to bite.

Taken together, these three regions account for just over half of global GDP. Given their size, weaker growth will inevitably weigh on the rest of the world – hence our view that we’re in the early stages of a global downturn.

The downturn in our forecast is more severe than that envisaged by the IMF and others, but relatively mild by past standards (particularly 2008-09). The real question, in my view, is therefore whether we’re missing something more serious. After all, the extent of the deterioration in the latest data has surprised even us. On some measures, industrial production in the euro-zone is now deteriorating at its fastest pace since 2009. What’s more, the global economy has been underpinned by increasingly shaky foundations. Debt levels are high, monetary policy in this cycle has been unusually accommodative, asset prices everywhere look stretched and global trade imbalances continue to linger in the background. None of this feels particularly sustainable, so it wouldn’t be a big surprise if it all came crashing down.

So what might we all be missing? Four things stand out. First, we may be underestimating the fallout from global “trade wars”. As we’ve argued before, it would require a significant escalation in trade protection to have a substantial direct impact on world trade volumes and thus global growth. But it’s possible that we may have underestimated the indirect effects of the trade war. Business investment in several countries has been unusually weak given the current point in the cycle, which may reflect skittishness about trade wars. And there is some evidence that the recent weakness in trade in Asia may have been caused by manufacturers of consumer electronics running down their inventories in anticipation of weaker demand resulting from higher tariffs. This should unwind if the US and China manage to agree a trade truce, but it may nonetheless help to explain the weakness of the recent data.

The second – and more ominous – thing we may be missing is that financial strains could be building in the world economy. There is nothing in the broad money or bank lending data to suggest that trouble is lurking around the corner. But financial conditions have tightened considerably in the world’s major advanced economies over the past six months, which has previously been a canary in the coal mine. Given the backdrop of high debt levels and stretched asset prices, it’s not difficult to see how this could develop into something more serious.

Third, it’s possible that we may be underestimating the extent of the slowdown in China. We track shifts in the economy using our China Activity Proxy, which we believe provides a more reliable measure of growth than the official data. But given the size and complexity of the economy, and the degree of structural change experienced over the past few years, it’s possible that we might be missing something. Of all the Chinese data, the trade figures are arguably the most reliable – and the fact that they have been particularly weak is an ominous sign.

Finally, it may be that we’re not missing anything at all, but the fact that the global economy is now more inter-connected means that feedback loops are amplifying the effects of slowing growth in each of the world’s major regions. These may have boosted growth in 2017, when the world experienced a synchronised upswing. But we may now be experiencing this in reverse.

Of course, it’s also possible that these concerns simply blow over and the global economy finds its feet once again. Some of the weakness in the euro-zone is undoubtedly due to temporary disruption in the auto industry, and lower oil prices are likely to pull down inflation this year which may give a boost to consumers. Likewise, a trade truce would remove one of the recent headwinds to growth and provide a shot in the arm for global equity markets. But ten years into the world recovery the risks probably lie on the downside – and it feels like this is where investors should be focusing their attention over the coming months.

Quite right. My view is we’re headed towards closer to 2% global growth in H2, 2019, led lower by fading Chinese growth, the US fiscal cliff and a European recession.

Yet, markets still have Trump Derangement Syndrome and are focused on every tick in US politics and the Fed rather than the overall picture. Friday saw the Fed leak that it is mulling easing up on quantitative tightening, at WSJ:

Federal Reserve officials are close to deciding they will maintain a larger portfolio of Treasury securities than they’d expected when they began shrinking those holdings two years ago, putting an end to the central bank’s portfolio wind-down closer into sight.

Officials are still resolving details of their strategy and how to communicate it to the public, according to their recent public comments and interviews. With interest rate increases on hold for now, planning for the bond portfolio could take center stage at a two-day…

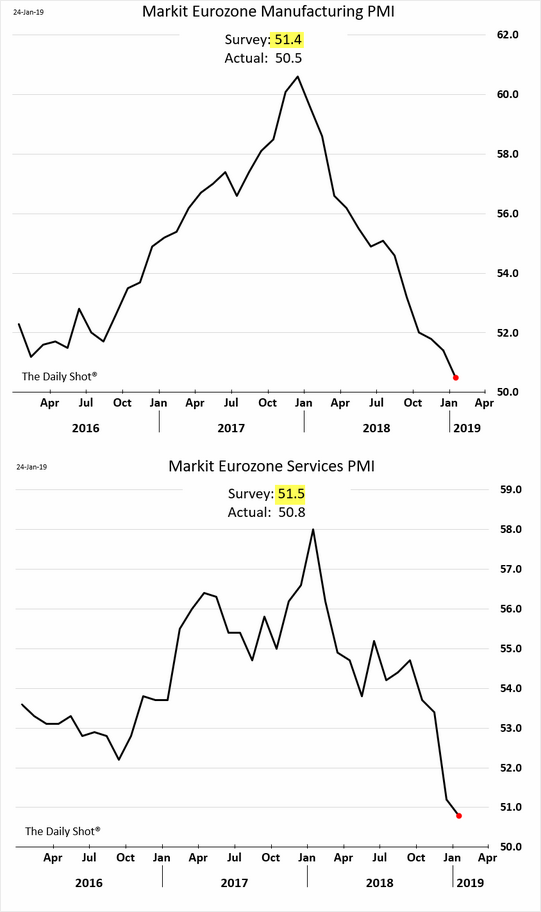

The ECB is still dawdling as recession tightens its grip on the Continent. The PMIs are one way train wreck:

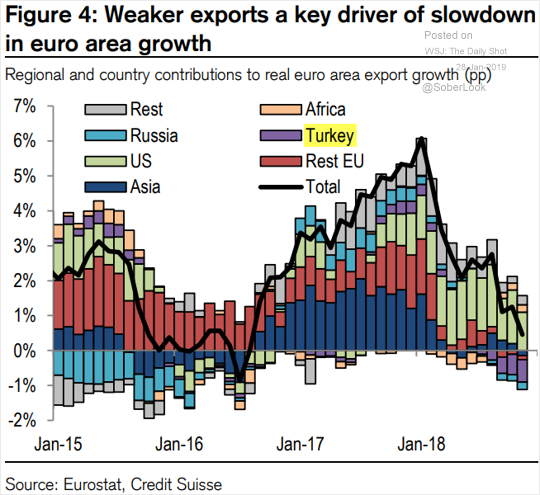

Led by collapsing external demand:

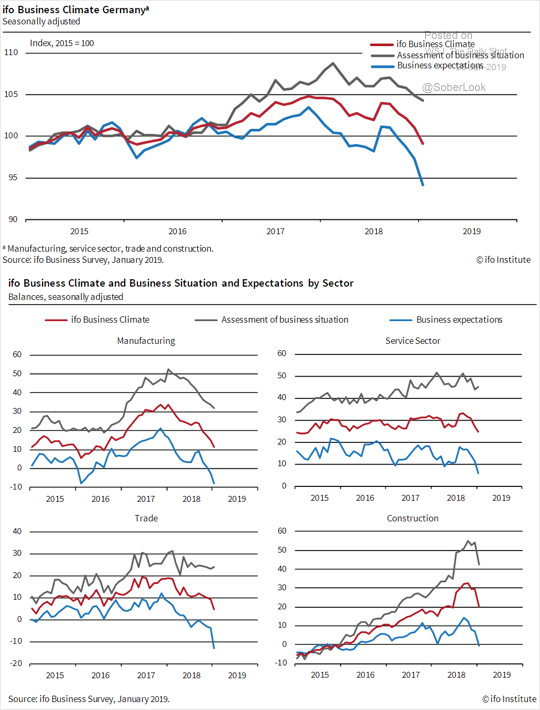

With investment to follow:

Mario Draghi is slowly warming up, also at WSJ:

The European Central Bank is ready to use all its policy tools to support Europe’s softening economy, including by restarting a recently shelved bond-buying program, ECB President Mario Draghi said.

The comments, delivered to European lawmakers in Brussels, underscore a new tone of caution from the ECB, which moved only last month to phase out its landmark stimulus policy, a €2.5 trillion ($2.9 trillion) bond-buying program known as quantitative easing or QE.

China has not done enough either to turn around growth and it will need to cut the cash rate to do it. In other words both the ECB and PBOC are going to have to trash their currencies.

For the time being, markets are obsessing over the US but it remains in decent shape post-shutdown. The Fed has been bashed into easing up by the White House but both China and Europe are going to have to ease much more aggressively if they’re going to turn growth.

Ironically, such will prevent the USD from falling which in turn will keep global liquidity tight until or unless US growth also falls over.

This will add ongoing downwards pressure to commodities and the AUD.