Hoocoodanode? From NAB:

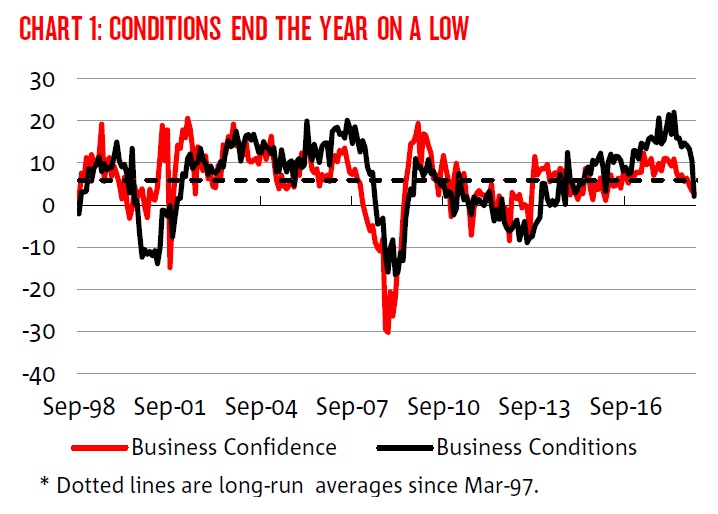

Business conditions fell sharply in December, and while caution should be taken when interpreting data around the Christmas/New Year period, this outcome continues the downward trend in conditions over the second half of 2018.

At face value, the fall over the past six months suggests a significant slowing in the momentum of activity in the business sector — especially from the highs seen earlier in the year.

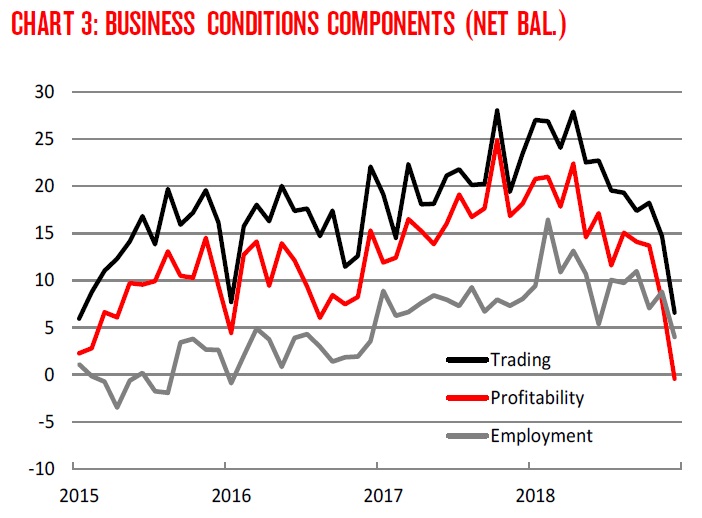

The deterioration… was driven by declines across trading, profitability and employment, and was relatively broad-based across states and industries.

Conditions remain particularly weak in the retail industry which reports further ongoing deterioration.

Capacity utilisation remains above average, though forward orders are below average and falling. Alongside below average business confidence this suggests conditions are unlikely to rebound.

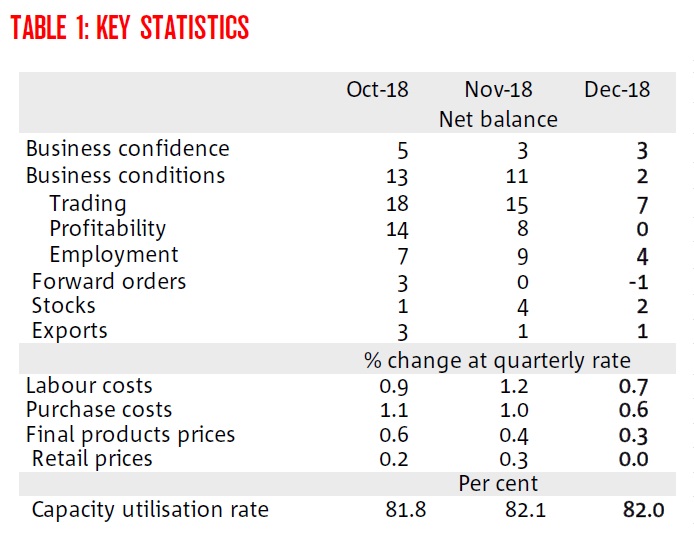

The result was driven by declines in all sub-indexes with employment falling five points to +4 index points, profitability falling 8 points to 0 index points and trading conditions declining to +7 index points.

At face value, the decline in the employment index suggests a slowing in the pace of employment growth to 18,000 per month from 22,000 per month.

Surveyed measures of prices and wages eased in December. Notably, retail prices were flat in the month.

Overall, these measures suggest that inflationary pressure remains weak, with final products prices and input prices such as purchase costs and labour costs continuing to track at relatively low levels.

With conditions having weakened notably in December following a trend slowing over the second half of 2018 we will be looking to the next readings from the business survey to confirm if the true underlying pace of business activity has slowed as sharply as the December survey suggests.

With confidence remaining below average and forward orders having also declined our expectation is that, at the very least, a significant portion of the decline in business conditions will persist.

If business activity has significantly slowed there could be some implications for the labour market and business capital expenditure (CAPEX) — two important variables whose outlook are critical for our outlook in 2019.

Here are the numbers:

Bye, bye employment. Forward orders and capex intentions are still falling as well. The headline crash is a beut:

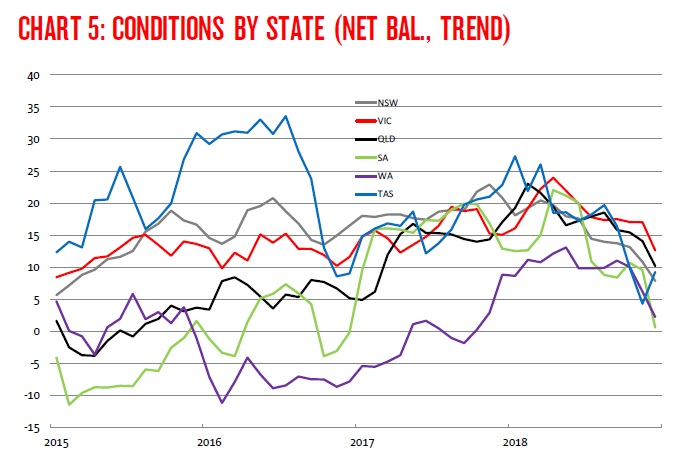

In every state bar Tassy, the only place property prices are booming:

And the everything crash:

Hello rate cuts.