By Martin North, Principal Analyst at Digital Finance Analytics:

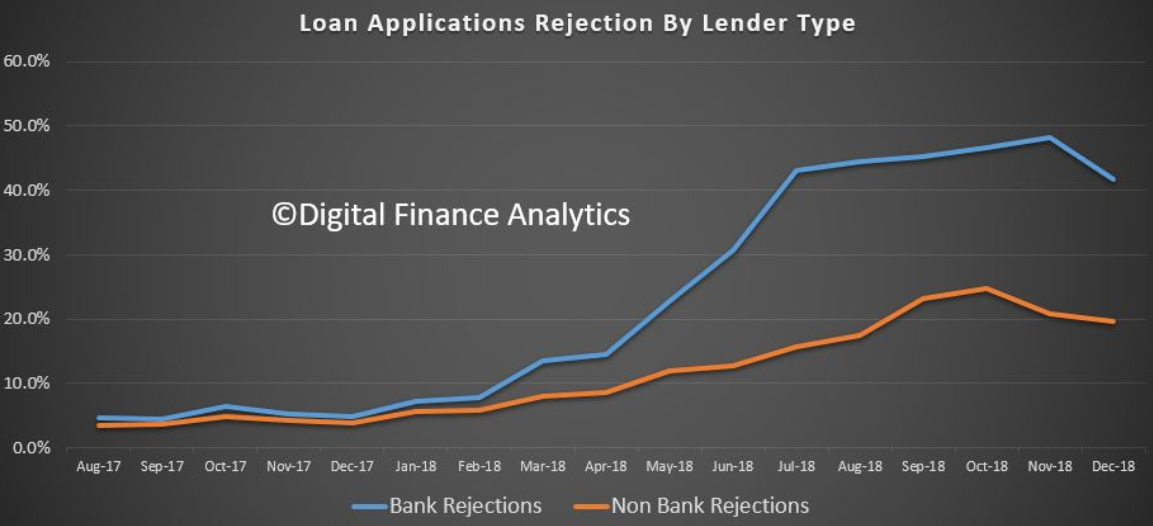

The latest data from our surveys indicates that around 40% of loan applications for mortgages were rejected in December 2018, compared with 8% a year prior, though on significantly lower absolute volumes. Households often made multiple applications when seeking a loan.

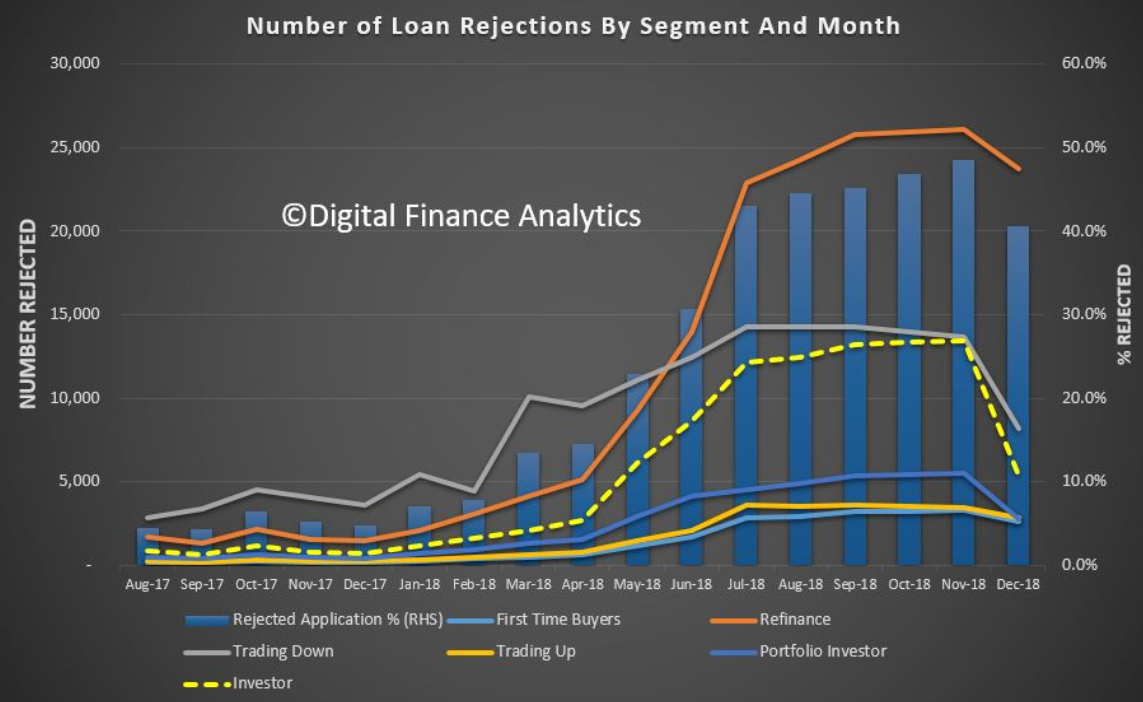

The volume of applications across all segments fell in the lead up to the holidays, and the proportion of rejections fell from 48% the prior month, which was a record.

The fall in investor applications is significant, as appetite for investment property eases. The relative volume of refinance applications remained quite high, as people are seeking to reduce their monthly repayments.

Non Bank rejections are running a much lower rates than bank rejections.