The Asian session was dominated by the release of the latest Chinese PMI manufacturing numbers, which remained in contraction mode, while the PBOC gave the Yuan a big push higher against USD, manuevering before the latest round of trade talks with the US. The reaction to the Federal Reserve’s meeting overnight has seen most undollar assets continue their rally, with the Australian dollar still well above 72 cents while gold also advanced.

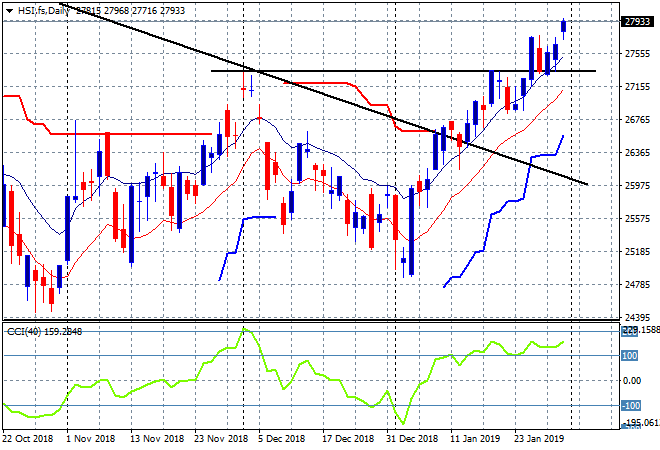

Chinese shares are powering ahead with the mainland Shanghai Composite currently up 0.% to 2593 points while the Hang Seng Index has advanced more than 1.2% to be at 27977 points, pushing well higher above the previous false break high above 27100 points:

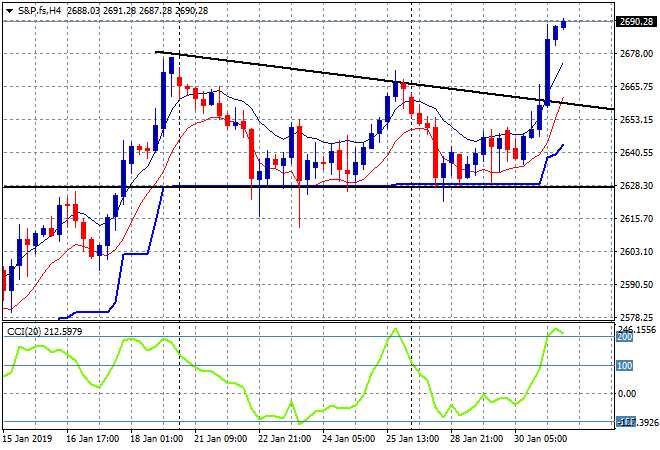

US and Eurostoxx futures are also getting a move on with the four hourly S&P 500 futures chart advancing from last night’s very solid gains with more positive expectations for earnings print tonight:

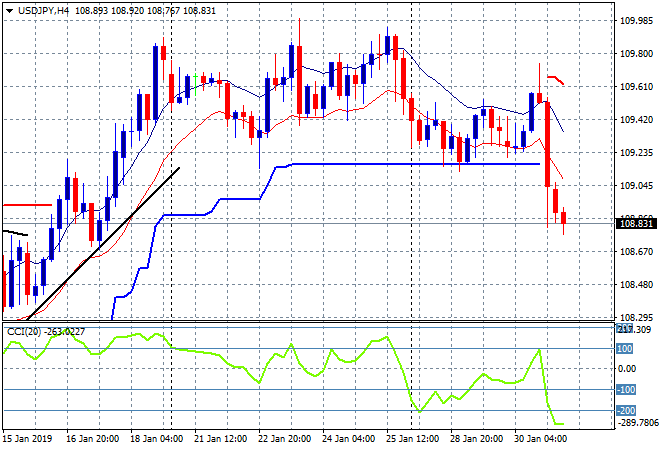

Japanese stock markets have done extremely well given the headwind of a major stronger Yen with risk sentiment overshadowing as the Nikkei 225 is currently more than 1% higher to 20812 points. The USDJPY pair continues to fall below previous trailing ATR support and below the 109 handle although this looks too far, too fast with momentum well overcooked to the downside:

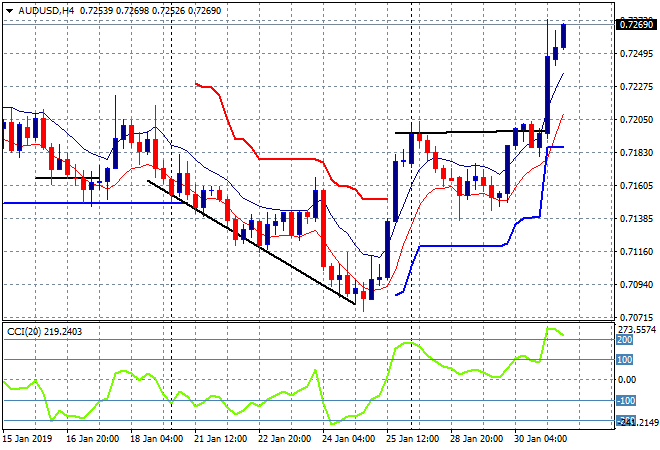

The ASX200 is the worst performer, barely hanging on at only a few points lower at 5884 points as the Australian dollar weighs on local risk. The Aussie is now well above the 72 handle following last nights’ spike on the back of the FOMC meeting with the 73 handle and a two month high well in sight:

The economic calendar continues to ramp up overnight with two important releases in Europe first, namely German unemployment and Italian 4Q GDP print. In the US its a backlog of data with the core personal consumption expenditure print – a key measure of GDP – an initial jobless claims coming out.