Caution reigns as traders weigh up the next FOMC meeting and continued US earnings, as the fallout from Caterpillar’s result last night and no further developments in US/China trade talks kept risk off the table. Currencies are relatively stable although the Kiwi is seeing a late bid, while the PBOC strengthening of the Yuan fix saw offshore trading fall down to the 6.75 level against USD.

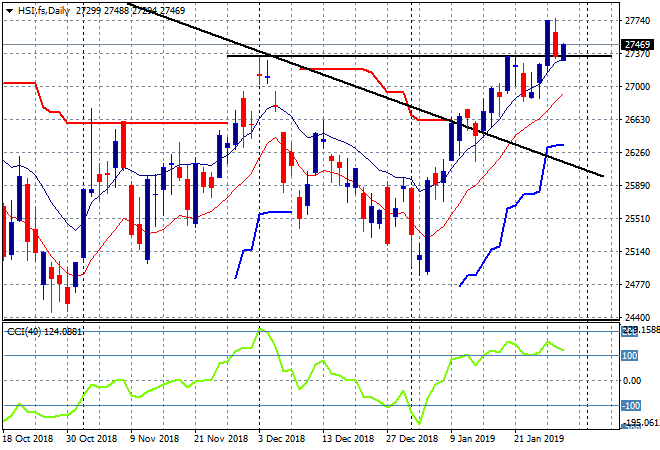

Chinese shares are selling off slightly going into the close with the Shanghai Composite currently down 0.2% to 2593 points while the Hang Seng Index is similarly weak, down 0.1% to 27539 points, still maintaining a daily close above the previous false break high above 27100 points which should give the bulls hope:

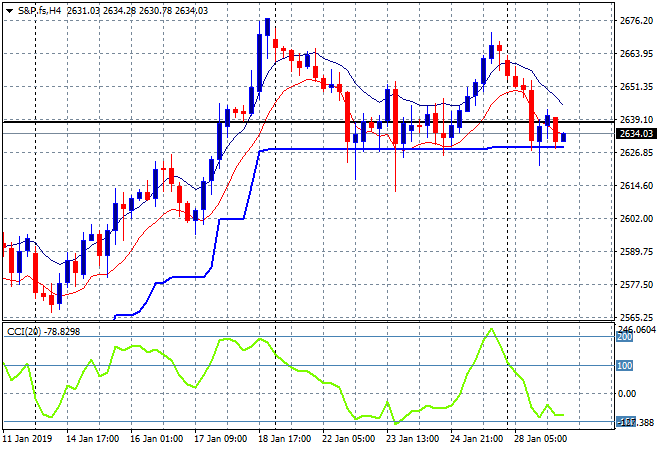

US and Eurostoxx futures are up slightly going into the London open with the four hourly S&P 500 futures chart barely holding on to last week’s support at the 2630 point level where the BTFD crowd needs to step in soon here:

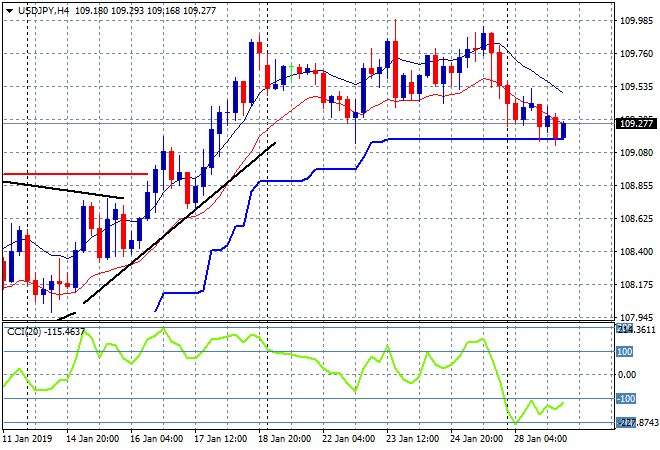

Japanese stock markets are the best performers for the day, but its not much with the Nikkei 225 eking out a minor 0.1% uptick to 20664 points. This is no doubt due to a much stronger Yen with a late selloff help pushing the USDJPY pair to remain just above the 109 handle where it could reverse below very quickly here:

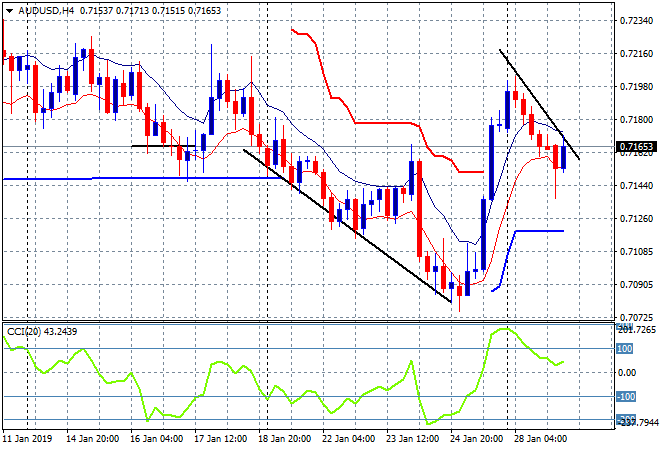

The ASX200 is the laggard losing nearly 0.6% to finish its first day back at 5874 points. The Australian dollar put in a late rally after floundering due to a very poor NAB business survey, currently just abvoe the mid 71’s against USD, but still facing a short term downtrend going into the FOMC and next weeks RBA meeting:

The economic calendar continues overnight with US home price data and the latest consumer confidence print plus a few wonky economic speeches from ECB and BOE boffins.