A mild selloff across Asian share markets today following the mixed action overnight due to the lack of direction from closed US markets. Focus on the Canadian imbroglio over the Huawei CFO court case brought the Yen buyers to the fore and saw risk currencies like Aussie and Kiwi to falter. The latest IMF growth forecast downgrades also didn’t help.

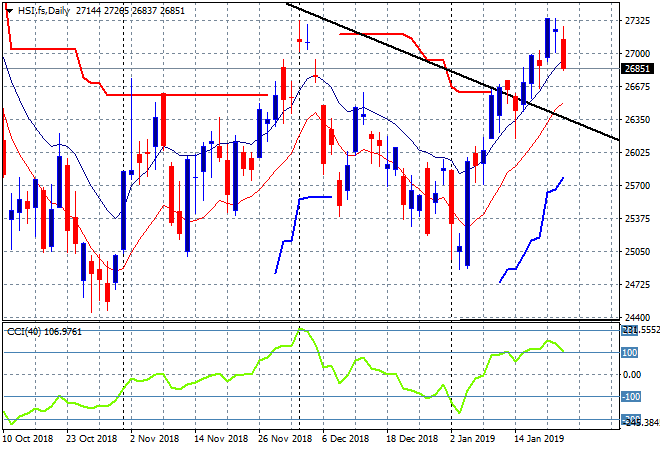

Chinese shares suffered the most, reversing the once positive mood with a weaker Yuan not helping as the Shanghai Composite closed over 1% lower to 2579 points with the Hang Seng Index also off, losing 1.1% to 26903 points. The daily chart shows how important it is for the market to really push through the previous falsebreak high above 27100 points so this one day reversal is not helpful:

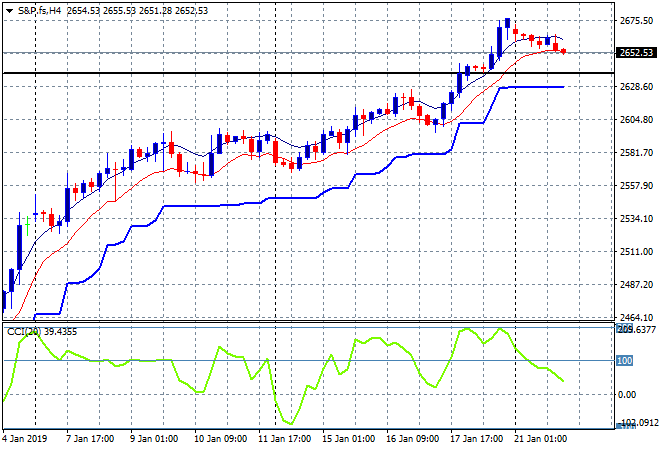

US and Eurostoxx futures are down slightly going into the London open with the four hourly S&P 500 futures chart still showing a market with the bulls still in control, but a small pullback would do well for a sustained uptrend:

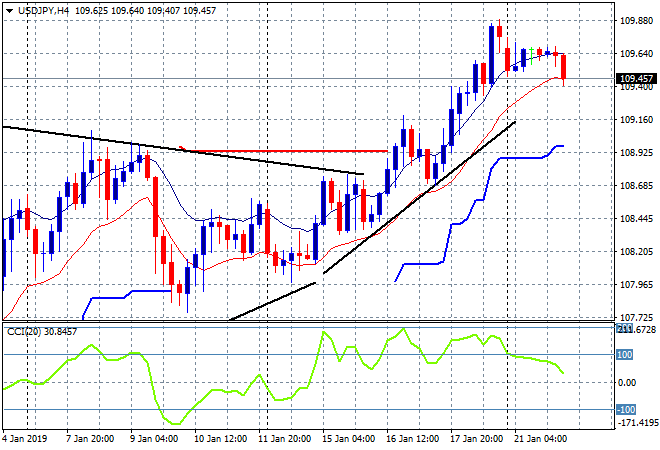

Japanese stock markets did the best relatively speaking, with the Nikkei 225 closing 0.5% or so lower to 20622 points. This was mainly due to a fall in the USDJPY pair with this pullback expected given that Friday night’s action was an overreach and could get down to the 109 handle proper:

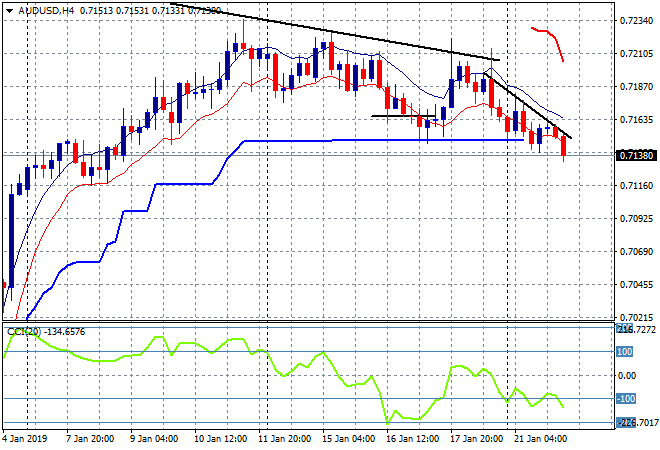

The ASX200 took back all of the previous gains, falling 0.5% to 5858 points, unable to build on the positive momentum and rebuffing psychological resistance at 6000 points. The Aussie dollar fell slightly on the open and then accelerated this afternoon, now heading for the 71 handle and breaking through solid support at the 71.50 level:

The economic calendar ramps up tonight with a slew of European releases, secondary ones first in the UK, but then the closely watched German ZEW survey. In the US, markets reopen after the long weekend and we get the latest existing home sales data.