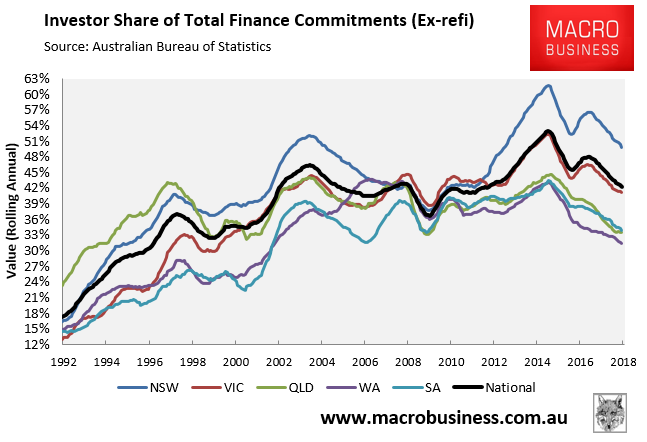

With the release yesterday of the ABS’ lending finance data for November, it’s an opportune time to once again chart how capital city house prices are tracking against both investor and total housing finance.

As MB readers know, housing finance has historically been strongly correlated with values. Therefore, it remains one of the best short-term predictors of price growth.

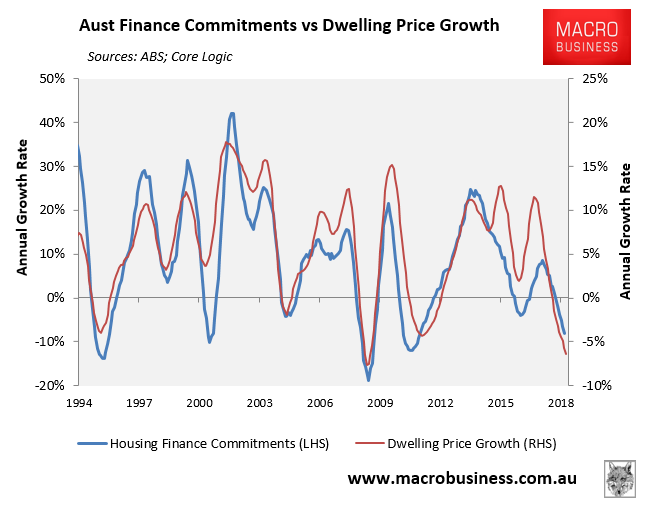

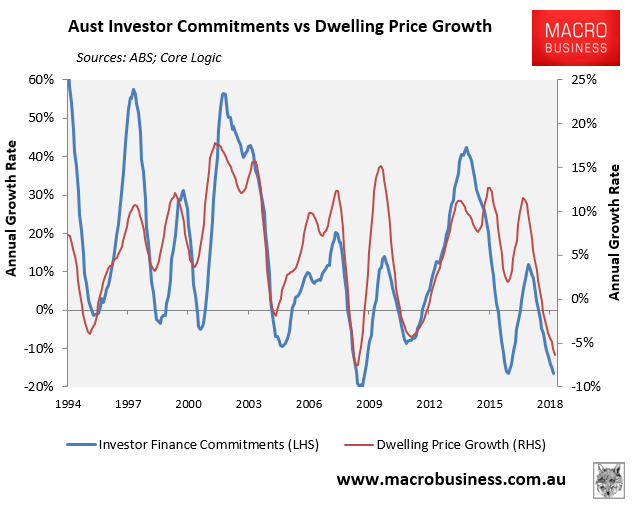

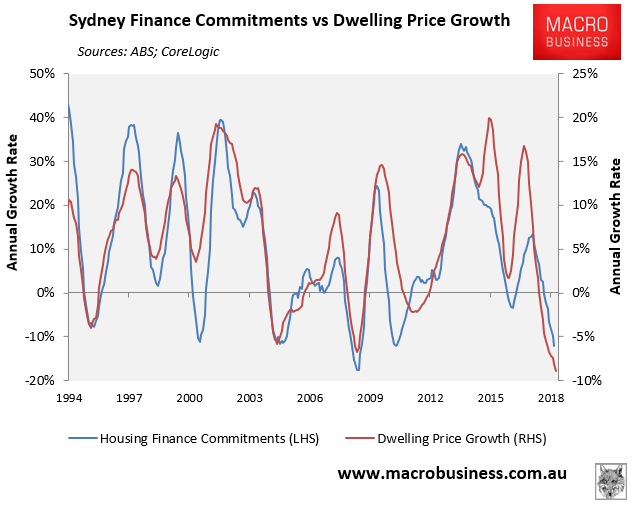

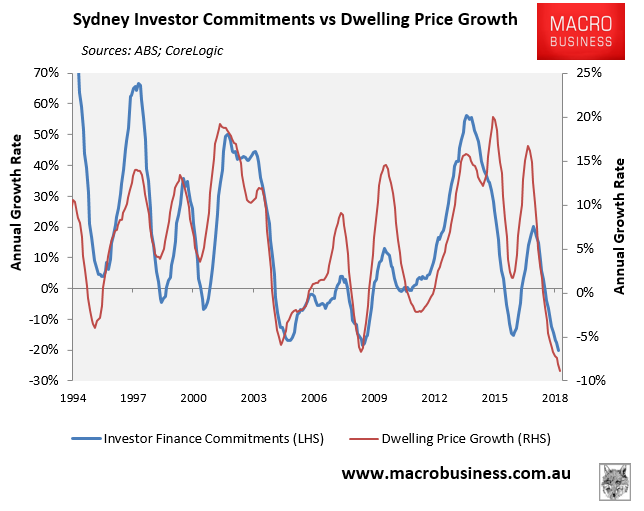

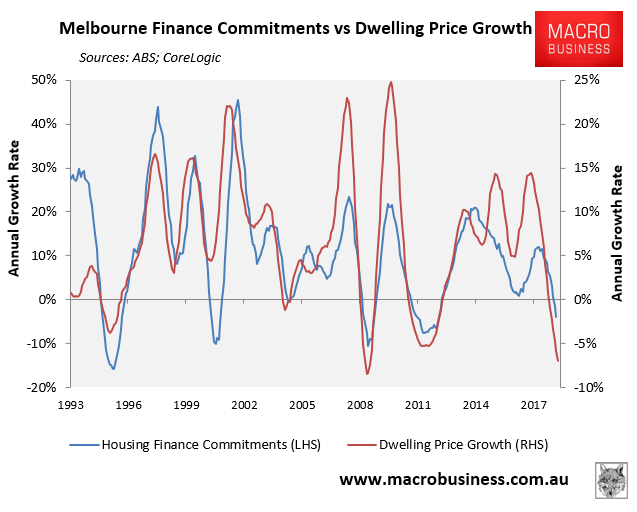

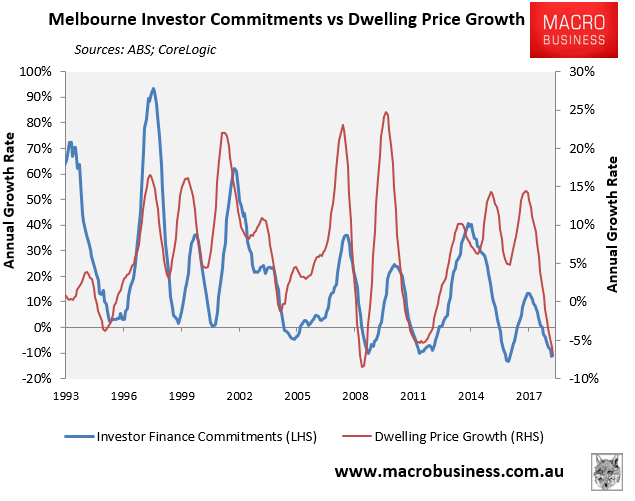

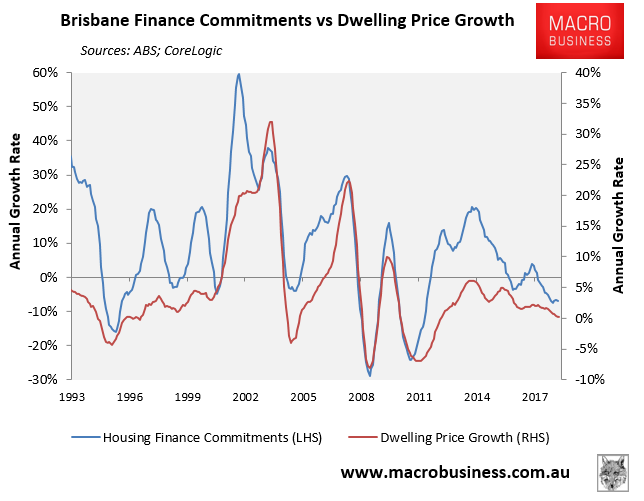

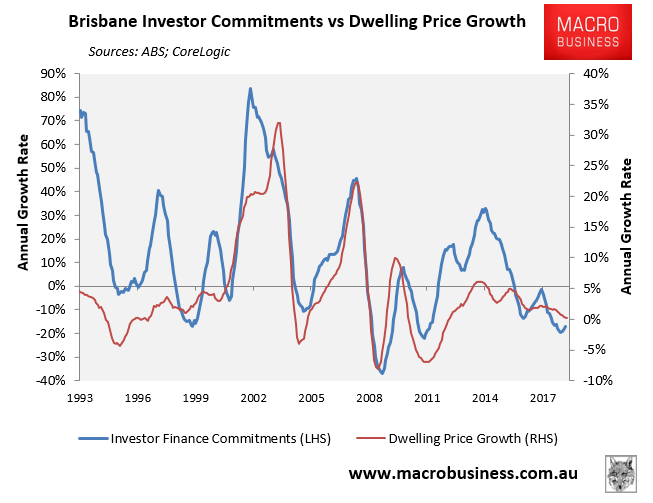

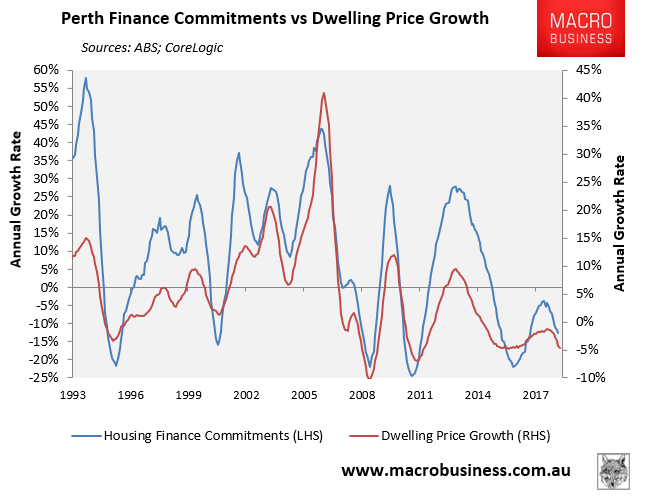

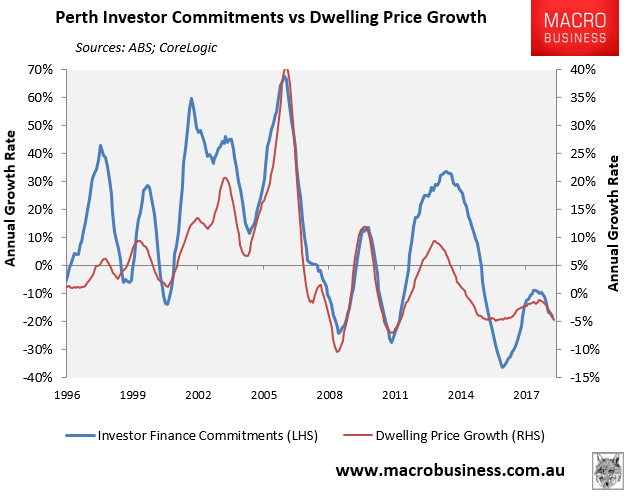

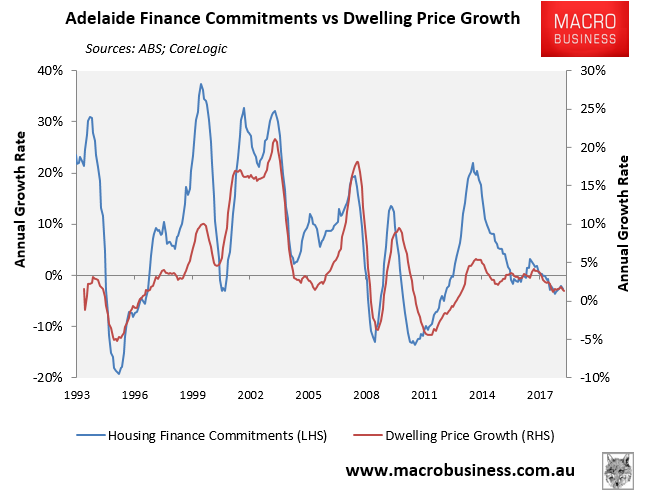

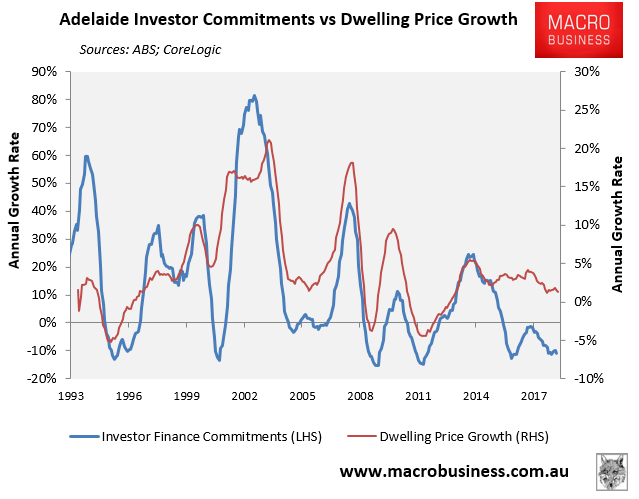

The below charts plot both CoreLogic’s monthly dwelling values index against the value of investor and total finance, as measured by the ABS.

First, here are the national charts:

Next, Sydney:

Next, Melbourne:

Next, Brisbane:

Next, Perth:

Finally, Adelaide:

As you can see, investor and housing finance growth as well as dwelling price growth has weakened across Sydney, Melbourne and Perth, but is stronger in Brisbane and Adelaide.

The decline is particularly sharp in the investor mecca of Sydney, where investors remain the marginal price setter.

We already know that investors face stiff headwinds in the period ahead due to:

- The massive interest-only (IO) mortgage reset due to take place over the next several years which, according to UBS, will see the potential expiry of IO loans in coming years (assuming a 5-year maturity and no rollover to another IO term) of up to $133 billion in FY19 and then $159 billion in FY20, in the process increasing repayments by around 35% on average;

- Tightening lending standards arising from the banking Royal Commission, which is due to release its final report early next month;

- Rising bank funding costs, possibly leading to further out-of-cycle mortgage rate rises; and

- Labor’s negative gearing and capital gains tax reforms in the likely event that it wins the next federal election, which is expected to be implemented on 1 July 2020.

These factors combined will continue to place downward pressure on housing values and make investing in property more risky and less desirable, especially in Sydney and to a lesser extent Melbourne, whose markets remain most over-valued and where investors are most dominant:

In short, until housing finance turns and begins to rise, Australian dwelling values will very likely continue to fall.