From Damien Boey at Credit Suisse

We have just published an article about the outlook for Sydney housing, now that prices have dropped around 15% from their late 2017 peak, and are falling at their fastest pace in several decades.

We take note of a few positives:

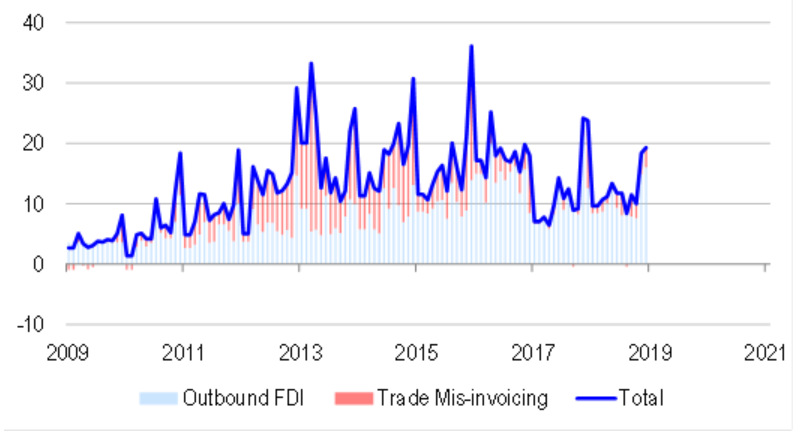

1). There are tentative signs that Chinese demand is bottoming out. Juwai.com reports a 58% increase in buyer enquiries in the year-to-4Q 2018. And our proprietary measure of Chinese resident outflows, based on outbound foreign direct investment, and trade mis-invoicing, has experienced its usual year-end spike, with the trend rate of decline slowing from 2017.

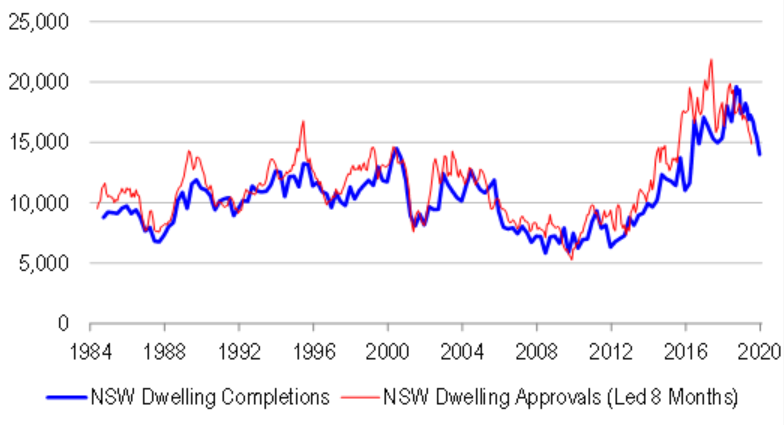

2). Supply is falling. Building approvals are down roughly 30% over the past year, foreshadowing quite a steep decline in dwelling completions.

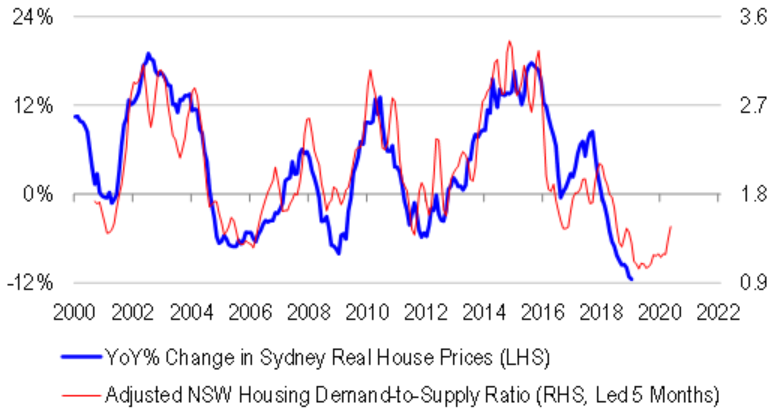

However, notwithstanding these “positives”, our proprietary measure of the demand-to-supply balance still remains 30% below its long term average. Even if we:

- Flat-track other demand drivers such as real mortgage rates and net new buyer participation,

- Assume that insolvency activity does not increase,

- Do not factor in any other tightening to come through, whether through stricter lending standards or out-of-cycle rate hikes,

the prospective bottoming out in demand, and the reduction in supply foreshadowed by leading indicators is still not enough to bring the housing market back into equilibrium. Therefore, real house prices are likely to continue falling, by around 9% in 2019, and possibly a little more in early 2020. Without timely or effective policy stimulus, the earliest that we can see the housing market stabilizing is 2H 2020.

We do believe that more stimulus is on the way. The RBA must cut rates, and quite substantially to ensure pass through to end borrowers, and offset potential tightening coming through from changes to negative gearing and capital gains tax discounts (in the event of a change in government). Whichever government ends up in power in 2H 2019, they must spend more to shield the economy from the large and negative multiplier effects from housing downturn. But all of this still seems a little while away. And in the interim, supply is the only variable able to adjust. Therefore, we could easily see building approvals fall by another 20-30%, after having already fallen by 30% over the past year. Nation-wide approvals have certainly not bottomed at 185K annualized.

If we consider that residential investment is 6% of GDP, a 20-30% nation-wide drop in construction activity would represent a 1.2-1.8% drag on 2019 GDP. This is even before considering negative wealth and credit effects of falling house prices on consumers, and the potential for residential investment to drop even more sharply than the 20-30% already baked in by building approvals.

Our outlook is negative for retail, building and banking sectors. We think that recently negative market momentum in these sectors is a meaningful signal to play.