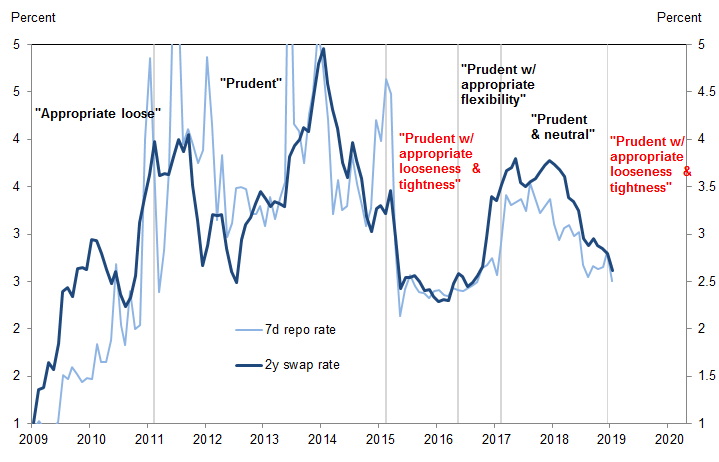

Over the weekend, when commenting on the latest rather disappointing RRR cut out of China (which would release just enough liquidity to offset liquidity drains via the MLP and repo) we pointed out another, far more important event which took place in late December, when traders were generally away on vacation, and when the PBOC indicated a critical shift in the official monetary policy description at the December Central Economic Work Conference, from “prudent and neutral” to “prudent with appropriate looseness and tightness”.

While the language sounds fairly similar, the new description is surprisingly similar to what was adopted in 2015, just as monetary policy eased significantly and ahead of the famous “Shanghai Accord” of January 2016 when, as the world was careening to a bear market, a coordinated response from G-7 leaders and China sparked a massive rally in stocks as China unleashed another major monetary easing burst which impacted the global economy for the next year. Furthermore, as Goldman adds, “such official policy language, while subtle, can carry important information about the monetary policy stance.”

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.