As predictable as the Sun rising:

BOQ today announced interest rates across a range of lending products will be increasing by between 11 basis points (bps) and 18 bps.

- The Economy Owner Occupier Principal and Interest rate is increasing by 11bps

- A number of other BOQ home loans and lines of credit rates are increasing by 18bps

While the changes affect a number of products, there is no change to BOQ’s Clear Path Owner Occupier Principal and Interest rates.

Lyn McGrath, Group Executive, Retail Banking said today’s announcement was a combination of a number of factors.

“Continuing funding cost pressures and intense competition for term deposits have contributed to this decision,” she said.

“While decisions like these are never easy, offsetting the impact of these costs ensures we balance the needs of our borrowers, depositors and shareholders,” she said.

The interest rate changes are effective Friday, 11 January 2019.

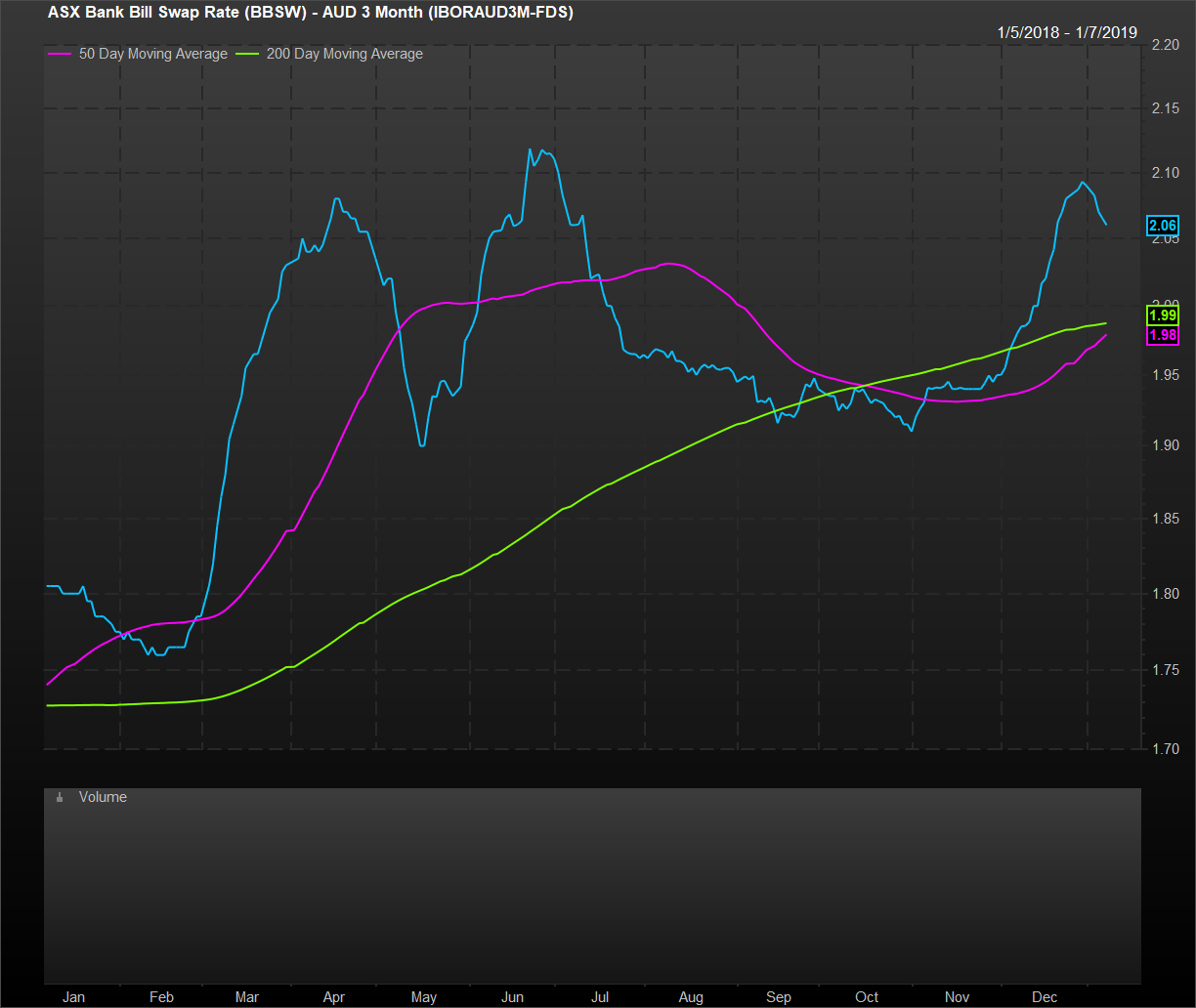

Front and back book. BBSW has been on a charge though may have peaked for now:

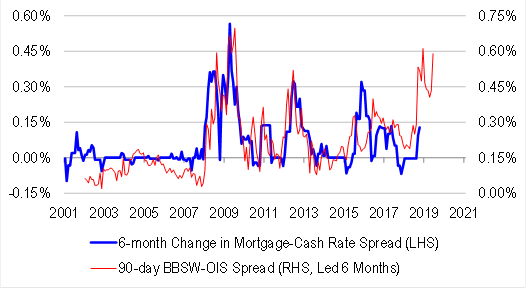

Term funding has been drawn in as well:

Leaving the banks little choice, via Credit Suisse:

You may recall that it was the regionals that kicked off the last round of out-of-cycle hikes. The majors will be next, managed around the release of the Hayne recommendations.

The economy is slowing fast, dragged down by the housing correction. The last thing it needs is tighter monetary conditions.

RBA to cut.