DXY was firm overnight. EUR was stable and CNY strong:

The Australian dollar was weak against DMs:

And EMs:

Advertisement

Presumably after yesterday’s NAB survey shocker. Gold was strong as we move into another Fed meet:

Oil too:

Advertisement

Base metals are still spoiling the party:

Big miners are OK. Aussie bulkers flew:

EM stocks are still threatening breakout:

Advertisement

Junk eased:

Treasuries were bought:

The bund curve flattened:

Advertisement

While stocks were mixed:

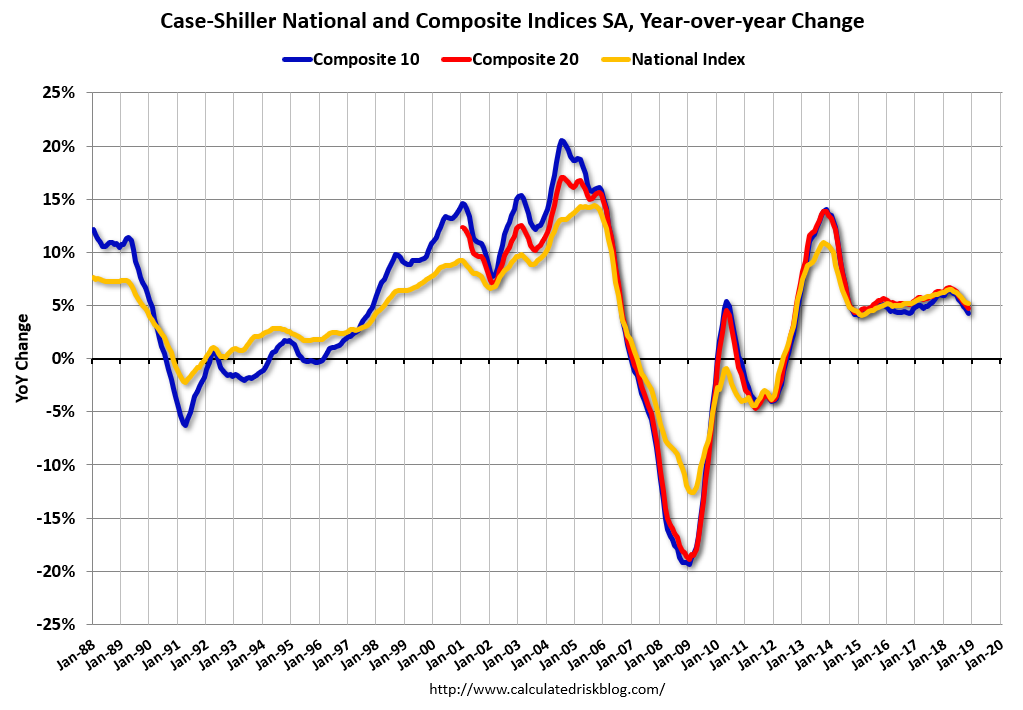

US data was OK with house prices slowing to 5.2% but still decent:

Advertisement

US consumer confidence took a hit from the shut down:

But that ought to pass quickly as government reopens and tax returns rain down.

I am still not especially concerned by the US. The shutdown will punt some first quarter activity forward so by mid-year it should still look decent as it heads into the fiscal cliff that will drag it down in H2. Even that still looks manageable on the domestic demand front.

Advertisement

The worry for the global economy remains external demand, specifically the China/Europe nexus, via FTAlphaville:

In our solar system, eight planets (sorry Pluto) revolve around the sun. As Stephen Jen and Joana Freire of Eurizon SLJ Asset Management see it, the US economy once served as that sun. The rest of the world, he says, were planets “revolving around, and being influenced by, the gravitational pull of the US economy.”

Now, a new sun has emerged. For Jen and Freire, “China has become not only big enough, but also the links of its economic ecosystem powerful enough” to pull on other “planets.”

…Using a series of network theory algorithms, Jen and Freire found that China’s influence on the world is now as sizable as the combined influence of the US and EU. The shift occured following the financial crisis in 2008, which saw the US’s impact on average global GDP shrink from just over 40 per cent between 1989-98 to half that between 2009-18:

What is more, the $9tn expansion of China’s GDP in dollar terms over the last decade outstripped that of the US and EU, which grew $7tn and $2tn respectively over the same period.

There’s bound to be some convergence as China’s economy continues to contract. And based on the most recent reading of industrial profits, China’s outlook is pretty dire. While profits officially fell another 1.9 per cent year-over-year in December, Freya Beamish at Pantheon Economics reckons that if other, more illustrative data is considered, the situation looks to be much worse (Authorities make certain adjustments, which Beamish says skew official results):

Fortunately for chief executives stateside, Europe bears much of the brunt for whatever originates in China. As Jen and Freire find, the region’s exposure is far greater than that of the US or the rest of the world:

Just as Draghi believes China can rescue the EU economically, so too can it drag the region down with it.

Which is why I see both China and Europe having to ease more aggressively than the US ahead which is CNY, EUR and AUD bearish.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.