DXY was up Friday night. CNY is going mad. EUR was down:

AUD is tracking the runaway CNY against DMs:

And blasted away from EMs as well:

Advertisement

This has absolutely nothing to do with the sagging local economy. It is a counter trend rally on the lifting trade war, pausing Fed, US government shutdown and modest Chinese stimulus. So long as those forces prevail we’re headed up on the AUD.

For how long? The good news for Aussie dollar bears is that it is almost certainly clearing out the big AUD market short. Owing to the US government shutdown we haven’t had a CFTC update since pre-Xmas but I’d be willing to bet that we’re headed swiftly back towards neutral from what was still moderately short. That will set us up to go lower:

Advertisement

Gold is stuck for now:

Oil flamed out:

Base metals still haven’t got the reflation memo:

Advertisement

Big miners fell:

EM stocks stopped in their tracks:

Same for high yield:

Advertisement

Treasuries were bid:

And bunds:

Stocks were flat:

Advertisement

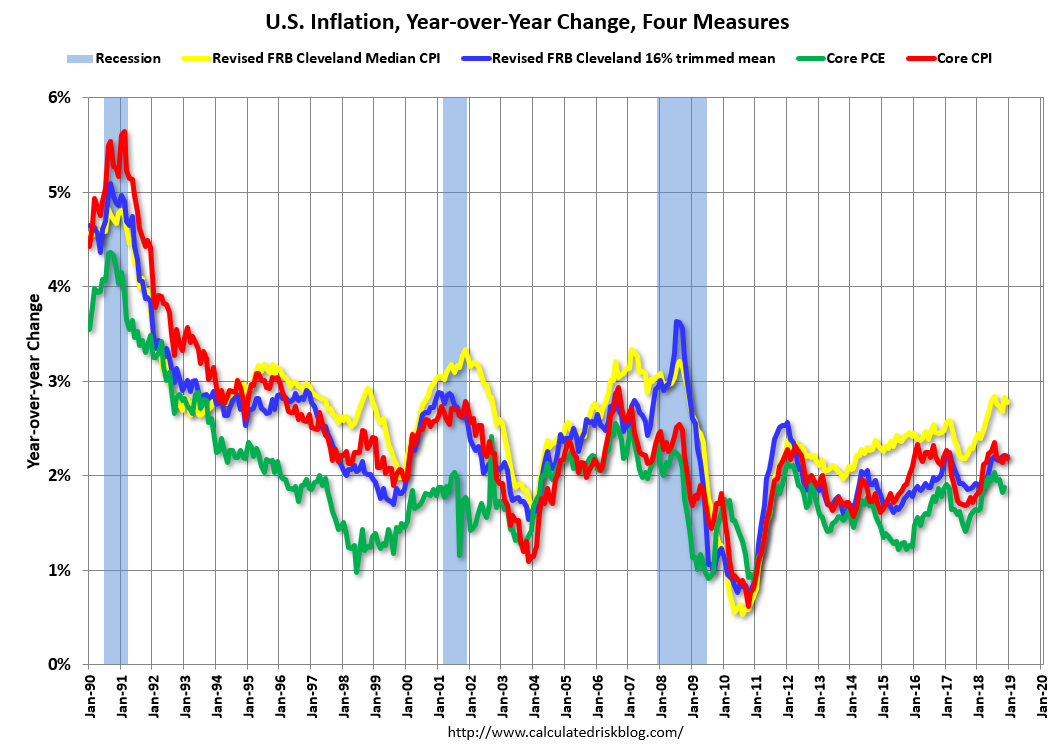

The big release for the night was US inflation which was still contained:

According to the Federal Reserve Bank of Cleveland, the median Consumer Price Index rose 0.2% (2.4% annualized rate) in December. The 16% trimmed-mean Consumer Price Index also rose 0.2% (2.5% annualized rate) during the month. The median CPI and 16% trimmed-mean CPI are measures of core inflation calculated by the Federal Reserve Bank of Cleveland based on data released in the Bureau of Labor Statistics’ (BLS) monthly CPI report.

Earlier today, the BLS reported that the seasonally adjusted CPI for all urban consumers fell 0.1% (-0.7% annualized rate) in December. The CPI less food and energy rose 0.2% (2.6% annualized rate) on a seasonally adjusted basis.

It also appears the shutdown is ending with Trump moving to fund his wall outside of congressional channels.

Advertisement

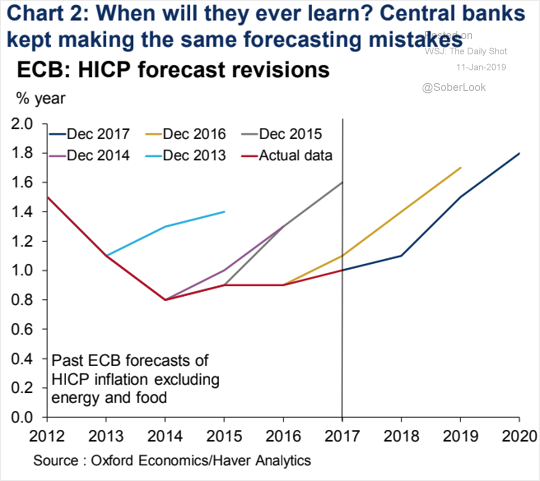

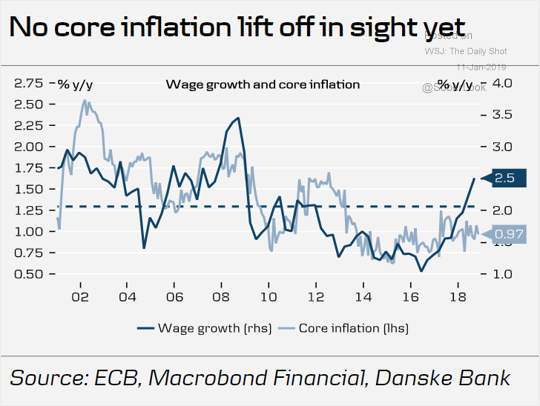

Meanwhile, in Europe central bankers are still hopeful as the economy tanks. The ECB really is an RBA scale dill:

Advertisement

It will have to learn the hard way…again.

Finally, we have China, which is going to cut its growth target, via Reuters:

China plans to set a lower economic growth target of 6-6.5 percent in 2019 compared with last year’s target of “around” 6.5 percent, policy sources told Reuters, as Beijing gears up to cope with higher U.S. tariffs and weakening domestic demand.

The proposed target, to be unveiled at the annual parliamentary session in March, was endorsed by top leaders at the annual closed-door Central Economic Work Conference in mid-December, according to four sources with knowledge of the meeting’s outcome.

Stimulus remains modest.

Advertisement

So, the ECB is going to be forced to its knees and China is not doing enough. Meanwhile, despite it’s pause, the Fed is not finished its tightening cycle and that is the key to everything. Via FTAlphaville:

When Federal Reserve Chairman Jay Powell said in December that the central bank’s reduction of its balance sheet was on autopilot, global markets balked. When he later walked back that statement at the annual meeting of the American Economic Association and assured that the Fed “wouldn’t hesitate” to alter its balance sheet policy if needed, investors cheered.

Few markets have gyrated on the comings and goings of this so-called “quantitative tightening” as wildly as emerging markets. As primary beneficiaries of its counterpart, quantitative easing, in the aftermath of the financial crisis, and the subsequent reach for yield as interest rates in developed economies fell, the fate of emerging markets is tethered quite closely to decisions made by the Federal Reserve.

Despite Powell’s new promise for patience when it comes to unwinding the balance sheet, an outright pause appears unlikely. For emerging markets, which have already felt substantial pain this year from this shift, the situation could deteriorate further.

Accelerating in earnest from 2009, the Fed snapped up US Treasuries to inject liquidity into the system and mortgage-backed securities to prop up demand for what were once considered safe assets. This helped to ease financial conditions and borrowing costs as prices rose and interest rates fell. Central banks across emerging markets followed suit, as did the Bank of Japan and European Central Bank. As Matt King of Citi shows in the below chart, that process has begun to taper off in some economies, and in the US, reverse altogether. The pace is set to quicken this year:

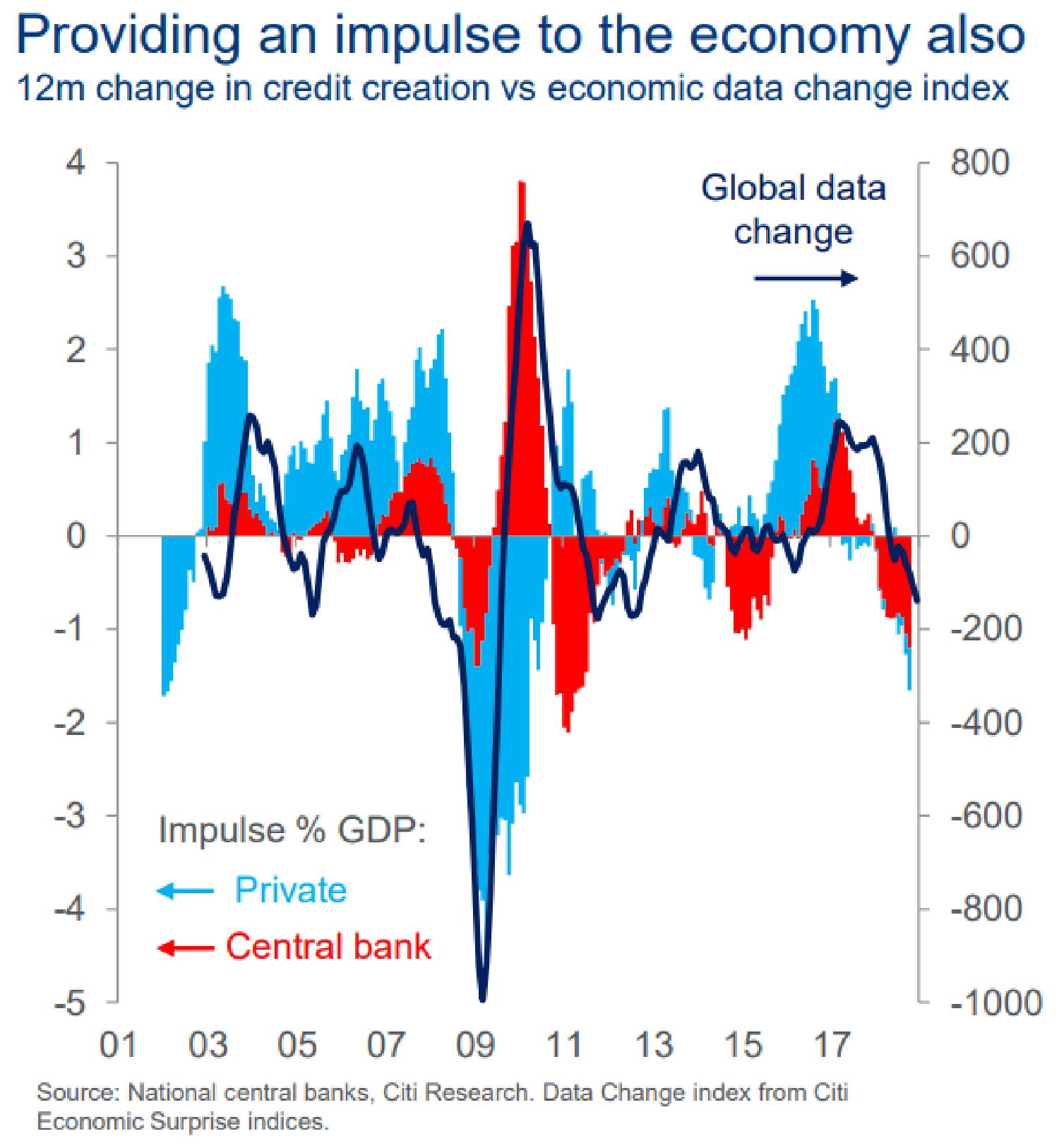

What this level of support helped to do was to allow non-financial corporations to pile on debt very cheaply. And that they did. Private credit in China and across emerging markets ballooned. Businesses in developed markets imbibed as well, but to a much smaller degree. Now, with central banks rolling off their balance sheets, King points out that private credit has started to shrink, too:

As with most binges, the come down is never easy — a reality of which many across the emerging world are now acutely aware. Given that “credit creation has been the most important driver of asset prices for decades,” according to King, the net effect on global economic growth and equity markets has been disruptive to say the least. Take a look at the change in global data versus credit creation in both the public and private sector. As credit creation has pulled back, economies have stumbled, per King:

A similar dynamic has played out in global equity markets, with the MSCI World Index plunging nearly 8 per cent since January 2018.

China and emerging markets have borne the brunt of this unwinding not only because they binged the most on the giant pool of cheap money in the years since the crisis, but also in large part because of what such an unwind means for the US dollar, as Citi’s Calvin Tse points out:

…if one thinks of the price of any asset as its relative supply versus demand, as the Fed shrinks its balance sheet, the supply of global dollars will also shrink. And this supply of USDs has proven to be a strong predictor of USD performance in recent years.

The dollar rally of 2018 surprised many, but none more so than emerging markets. On a trade-weighted basis, the greenback surged just shy of 8 per cent last year, exacerbating currency crises not only in Argentina and Turkey, but other economies with large dollar-denominated debts.

Advertisement

In short we are not yet in a rerun of the 2016 stimulus takeoff. Things must get worse first as the excellent Viktor Schvets of Macquarie argues today:

The climb down by all parties (including the Fed) has always been as close as one gets to an absolute certainty. The only question that we have been raising is one of timing and how much pain would need to be endured. Neither CBs nor China are yet embracing our bleak view of the future of ever diminishing windows of acceptable cost of capital and volatilities, as private sectors atrophy under pressure of technological evolution and financialization. Instead, we see everyone (from IMF to PBoC) debating debt sustainability, reforms and returning to private sector primacy. Hence, neither US, Fed nor China want to ‘overreact’; as a result, they run the constant risk of ‘under-reacting’.

First, the commodity complex (CRB), is ~20% higher.

Second, wage pressures in most key economies, though relatively tame, are stronger.

Third, inflation rates are higher (G7 CPI is ~1.9% vs 0.6% in Feb ’16), while China’s PPI is no longer negative (-5.3% in Jan ’16 vs 0.9% today).

Fourth, investors need to take into account far more unpredictable and nationalistic political background.

Fifth, Europe is potentially facing a revolution. But as in ’15, all measures of liquidity have turned negative, and global momentum is ebbing.

We believe there is a high probability that investors might revisit lows of late ’18 as policy-makers dither. It seems unlikely that China would embark on a sufficiently large stimulus until later in ’19. As the state is on both sides of any transaction, nothing moves until the state significantly raises spending. At the same time, we don’t believe that just ending balance sheet reduction and pausing (Fed) is sufficient. Also, Europe might be paralysed until elections and changes in key portfolios (including ECB). The threshold required to go from normalization to liquidity injections is high; hence, pain is likely to rise.

It is my view that with China refusing to go all-in on stimulus and Europe dying, the US dollar bull market is not yet over. While it lasts global growth will keep slowing. To end the global US dollar squeeze we will need to see a virtual recession in the US that bashes the Fed back to rate cuts.

Advertisement

That will take much more market pain. Global recession levels of it (anywhere around 2% growth). The kind of environment that crashes the Australian dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.