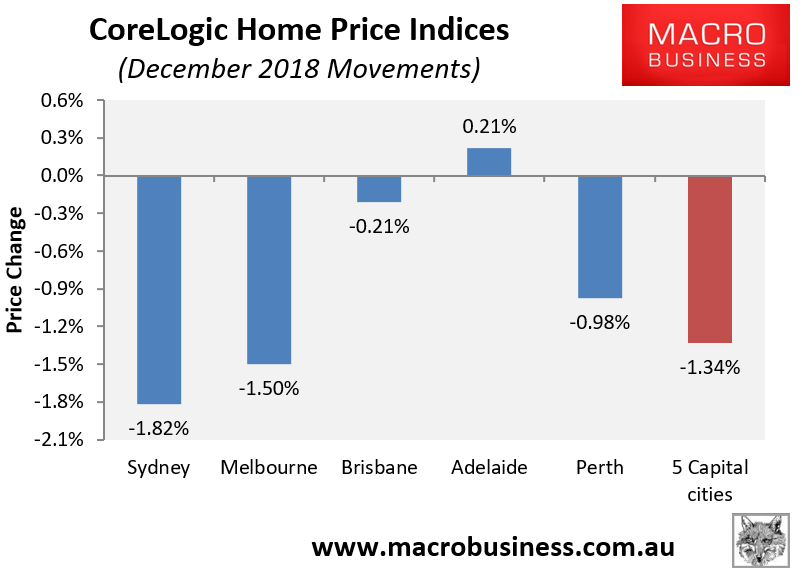

CoreLogic’s dwelling price results were released for December, with revealed another 1.34% decrease in values recorded over the month at the 5-city level:

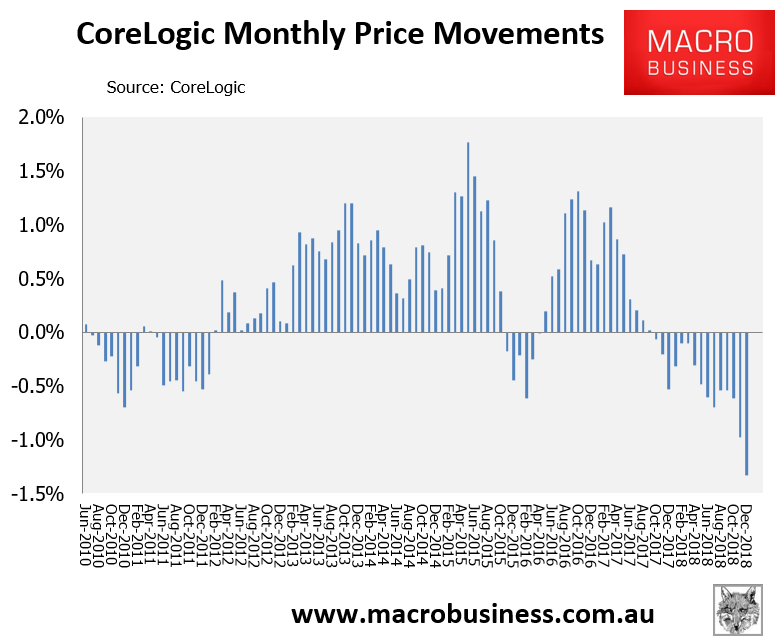

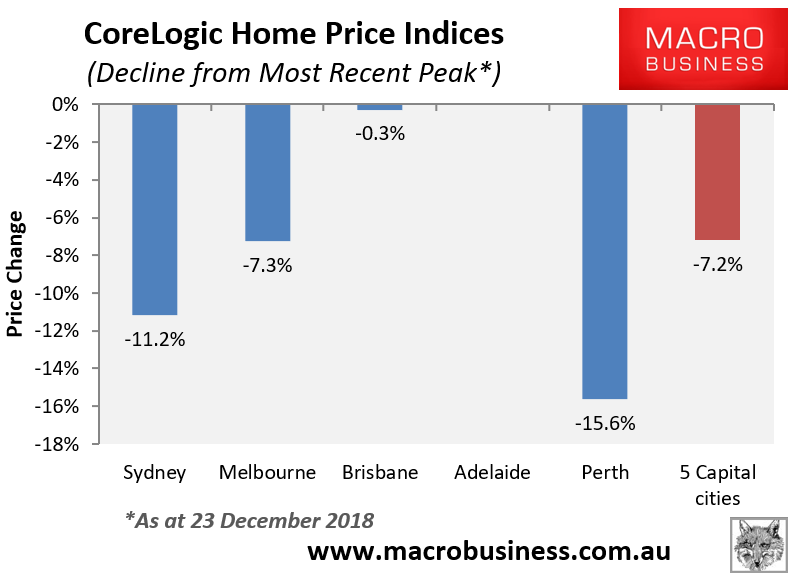

It was the 15th consecutive monthly decline in home values, with values down a cumulative 7.2% over that period at the 5-city level:

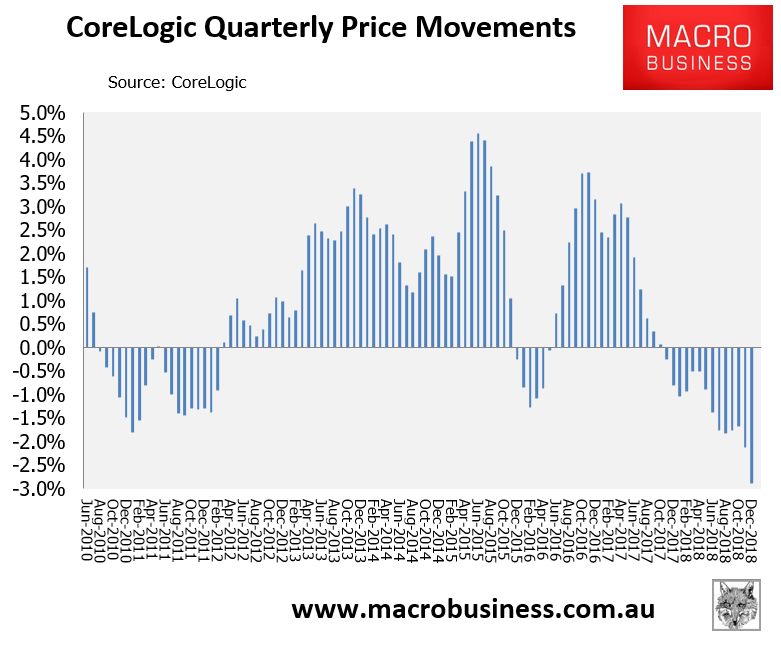

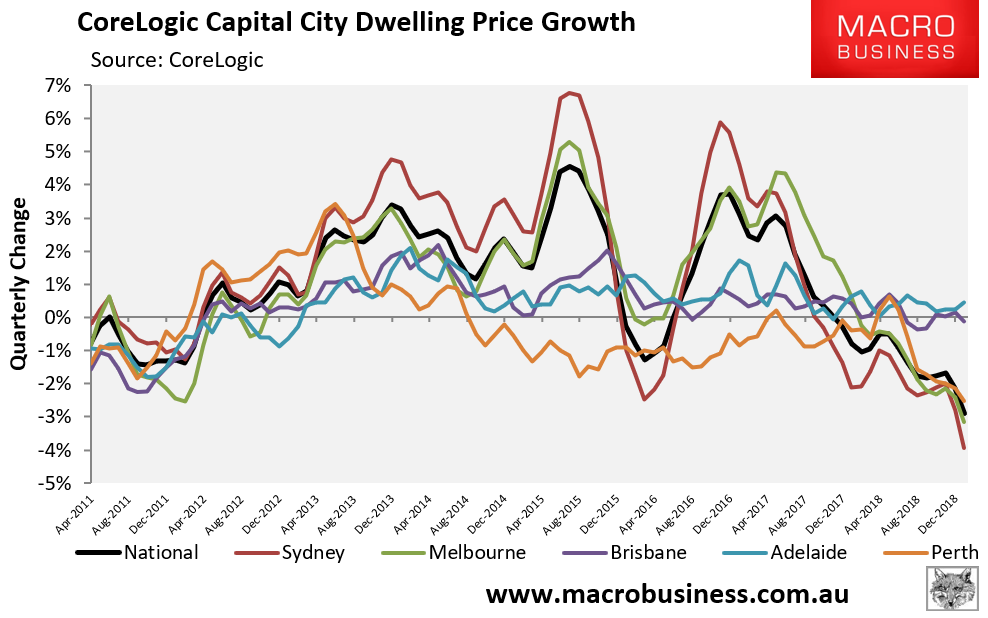

Quarterly values also dived another 2.9%, with the trend worsening:

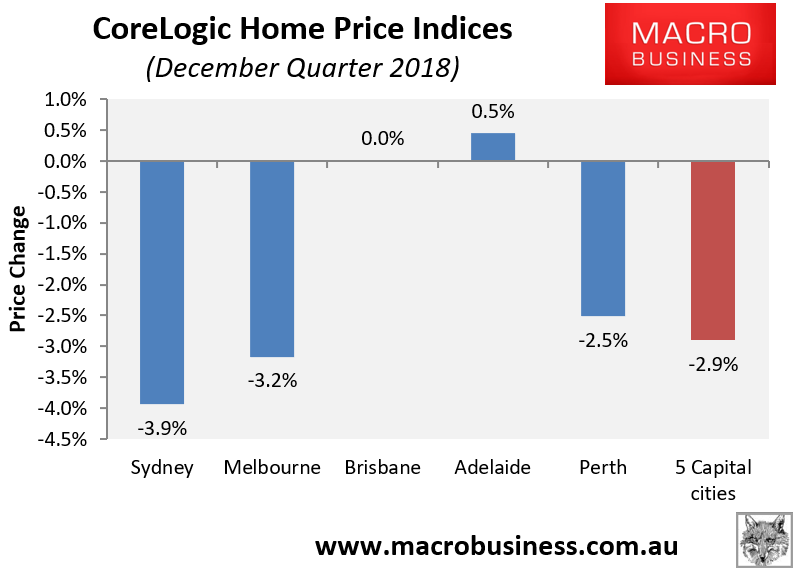

Over the December quarter, values were down heavily across Sydney, Melbourne and Perth:

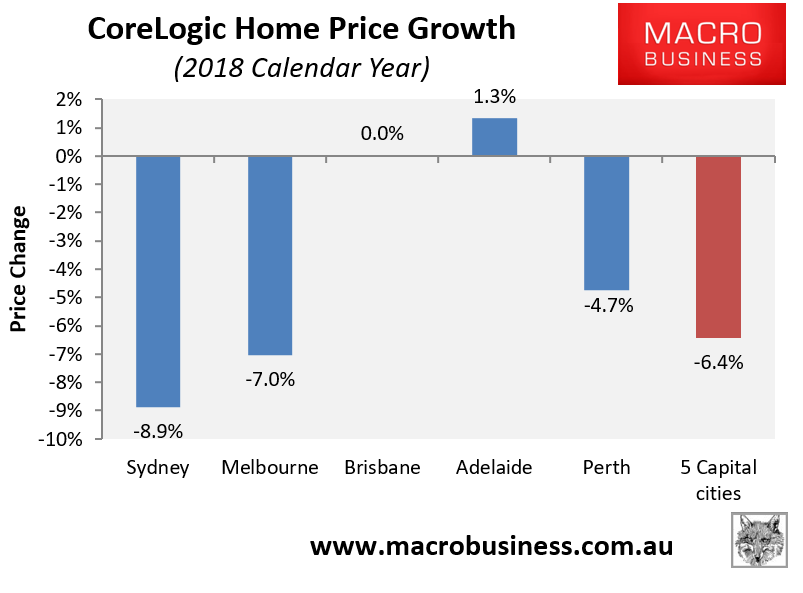

In the 2018 calendar year, home values crashed by 6.4% at the 5-city level, driven by Sydney (-8.9%) and Melbourne (-7.0%):

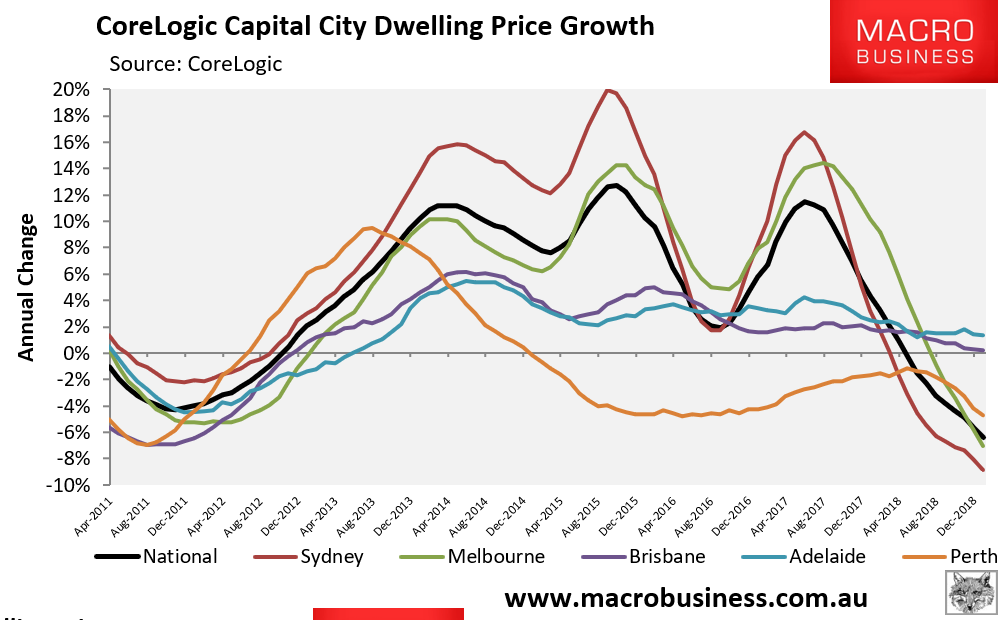

The next chart, which tracks trend annual price growth, shows a collapsing trend driven by Sydney, Melbourne and Perth:

Similarly, the below chart tracks price growth on a quarterly basis, with the same three markets collapsing:

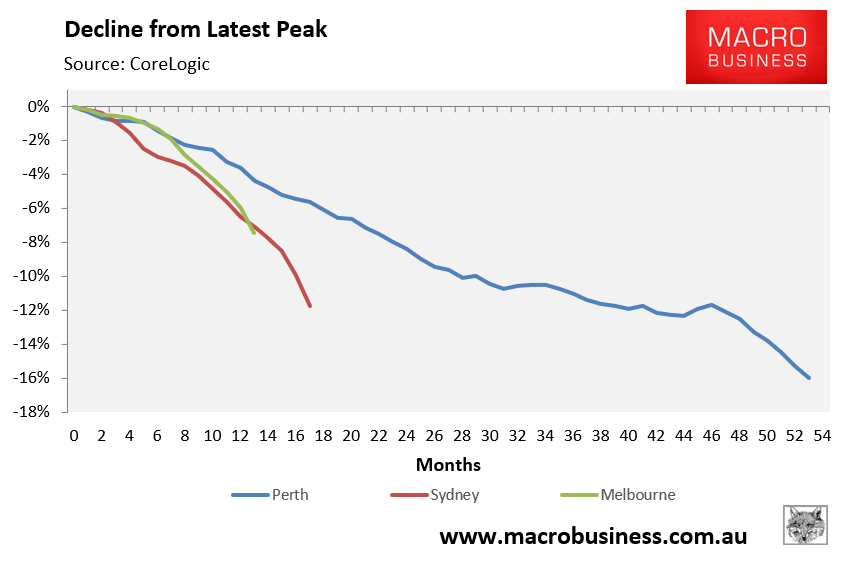

Sydney has already followed Perth into double-digit peak-to-trough falls, with Melbourne following:

And the pace of decline is both steep and accelerating in Sydney and Melbourne:

The crash is on like Donkey Kong!