With the royal commission awaiting the final report, we have been treated to a range of superannuation specific stuff-ups from major institutions. Most were through the master-trust structure that pools all the money and you end up in the situation where you as an investor find yourself paying for tickets to the tennis for HostPlus super clients, or you find IOOF using your money to compensate other investors for mistakes that IOOF made or Suncorp using your tax return to pay its own expenses.

This all feeds into the 6 main problems, as I see it, with superannuation:

- The tax breaks skewed towards those who need them least

- The fees charged are too high

- Super is not succeeding at getting people off the pension

- The complexity is too much for most people

- Related party and “game of mates” deals are rife

- Bundled products rip-off disinterested clients

1. The tax breaks skewed towards those who need them least

The problem with superannuation is that it gives the biggest tax break to those on the highest incomes:

- Someone on the top tax bracket who earns $1 in interest not in super would pay $0.47 in tax. In super that falls to $0.15, a gain of 32c for every dollar earned.

- Someone on the lowest tax bracket who earns $1 in interest not in super would pay $0.00 in tax. In super that rises to $0.15, a loss of 15c for every dollar earned.

From Grattan:

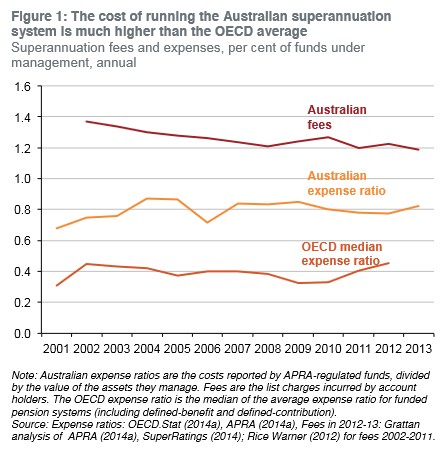

2. The fees charged are too high

Australian costs are well above the costs of other countries, despite the sector being larger and compulsory in Australia.

3. Super is not succeeding at getting people off the pension

Superannuation was introduced to reduce the problem of an aging population and a growing pension bill. It isn’t working.

The societal outcomes are suboptimal – we are giving huge tax benefits to the richest (who probably wouldn’t have needed the pension anyway) and the needle is barely moving on the proportion of people on the Age Pension.

Basically, about 80% of old people get some form of pension, which is hardly improved from the introduction of superannuation.

4. The complexity is too much for most people

I don’t have a lot of stats on this one.

What I do know is that the ACCC just finished a report into the electricity sector and found that consumers were being gouged by not staying on top of their bills and not shopping around for new deals. Basically, most people don’t care enough to look closely at their electricity bill and electricity companies take advantage. The electricity companies also take advantage by creating complex discounts which can make it difficult to work out which is cheaper. I also know electricity is a commodity good – the kW of electricity from AGL is no different to the kW from Origin.

But investment returns are different, there is the active vs passive debate, a host of different quality funds, different risks, historical returns over different periods, backtest returns vs real returns and hundreds of strategies to consider before we even get to the price. And when you do get to the price there are embedded fees (which often don’t get seen), performance fees (which are unknown), high water marks, lockup periods and a hundred other variations.

I also know that the effect of a higher/lower electricity bill has some sense of urgency on a forty-something-year-old. If the forty-something-year-old changes provider now they can save money in 3 months time when the next bill comes. When they are not going to see superannuation for 300 months there is a lower sense of urgency.

Letting the average Australian loose to choose the right electricity contract and relying on “market forces” not to screw the average Australian hasn’t worked. What are the odds of market forces working if we take the same average Australian and introduce them to the superannuation market where the product complexity is 1,000x greater and the time before they see any money is 100x longer?

5. Related party and “game of mates” deals are rife

Dr Cameron Murray has a whole chapter on this in his book Game of Mates. Basically, cosy relations between employers and unions in industry super funds lead to lots of money for all involved except the employees whose super is being invested. Unlisted projects like property and infrastructure are a great place for “grey gifts” to be swapped.

From Cameron’s book:

Cameron goes on to give a range of examples where the actors have been caught.

Just as contentious in my view is the ability of some funds to spend money on marketing (to attract new members), and have that paid for by existing investors. Why should you as an investor have to pay for your fund’s decision to advertise for new clients?

6. Bundled products rip-off disinterested clients

Retail funds often bundle financial advice or insurance, and often these are not at commercial rates.

Again, Cameron has the story in his book:

I had my own experience with a child actor who did some advertising work. Her agent set up the payments and superannuation fund – it wasn’t much, a few hundred dollars in super but as an eleven-year-old, you would think that the power of compounding returns was on her side. By the time I looked at it two years later all of the money had gone in life insurance premiums which had been set up by default.

————————————–

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.