Stock markets around the world have fallen precipitously over the last 3 months, and our portfolios have not been immune to the effects. We have maintained our overweight cash and bond positions which helped to stem the losses and helped our portfolios outperform – although falling by less than competitors is rarely of much solace to investors.

The real question is where to from here, with markets down again in December so far. And for that, I want to take a step back to consider the bigger picture.

First, a definition: Reflexivity is the theory that a two-way feedback loop exists in which investors’ perceptions affect that environment, which in turn changes investor perceptions. An example is the “wealth effect”: (1) stock prices rise, (2) then consumers spend more, businesses increase hiring and capex (3) more employment means consumers have more to spend (4) company profits rise which “justify” the stock price rise from step 1.

Why this is important is because there are a few key areas where reflexivity is a major issue in today’s markets:

- Fears that the Fed will raise rates too quickly and crash the US economy

- Fears that Chinese growth will slow and the debt-driven growth model will come unravelled

- Fears of a hard Brexit in Europe sending the UK into recession and effects on the European economy

Reflexivity 1: The US Fed

Economically, little has changed over the past three months in the US, unemployment is low, inflation contained, business surveys in expansion mode, company profits still rising and nascent signs of wages growth which could spur the business cycle into another upward leg. The main difference is the stock market has fallen around 20%.

Reflexivity question: Can a weak stock market cause the economy to slow?

Early in his role as the US Fed chair, Jerome Powell made comments that the Fed was not there to bail out markets – suggesting the “Bernanke/Yellen put” (where the US Fed will provide support if stock markets fall) is no longer in action.

The reality is that, at least in some respects, the Fed is there to bail out markets. There is little sense in the Fed lowering interest rates to stimulate the economy by “pushing investors into risky assets” if investors are at the same time fleeing risky assets.

The issue is whether a falling stock market sends the wealth effect into reverse, crimps investment in the US economy as companies pull back from their plans (partly due to the increased uncertainty sparked by a lower stock market) and then unemployment rises.

In my view, this can happen if markets keep falling and a general air of panic takes hold.

The circuit breaker needs to be the Fed. It needs to explicitly tell the market that the Fed will support growth and that the Fed recognises the danger of raising rates too quickly and causing a 1937 style1 downturn. If this happens sooner rather than later, there will probably be little effect on the real economy. The longer it takes, the greater the effect.

Reflexivity 2: Chinese growth

China’s reflexivity problem is more complex. First some background:

- China has serious longer-term economic issues that we have discussed on numerous occasions. China is running a Gerschenkron economic growth model, which has been run by many countries in the last 50 years including Russia, Japan, Cuba, South Korea and a number of Latin American countries. For countries that are underinvested, by repressing consumption, countries can increase savings and investment and then, for a period of time, generate growth that more than makes up for the repressed consumption. When the investment stops generating adequate returns, the debt burden begins to grow and the country needs to change its growth model or go through a debt crisis. China is at the debt accumulation stage where the debt burden needs to grow significantly to maintain growth. This is not an imminent issue but it is clearly unsustainable.

- The problems have been getting worse in recent years. China has made several attempts to rebalance its economy away from capex driven growth. Each time China has slowed sharply enough that the attempts to rebalance have been abandoned.

- Growth is slowing in China despite record home building. There is scope for China to grow its infrastructure spending, but the key driver of much of China’s growth is home building which looks is already running at elevated levels.

- The US/China trade war is exacerbating the problem. Tariffs get the most headlines but in our view, the concerted and relentless release of hacking stories across multiple countries is likely to be more damaging in the long term as companies in developed markets shift structurally away from incorporating Chinese technology.

- China also has a number of other constraints. Cutting interest rates and reducing the currency might spark capital outflows and further US sanctions.

Reflexivity question 1: Can a weak stock market prompt Trump to make a trade deal with China?

Yes is the short answer. However, it is unlikely to be an all-encompassing fix to the issues between China and other countries. Cancelling a few tariffs will not solve China’s trade issues and trade is not the only consideration in the growth issues facing China.

Reflexivity question 2: Does weaker Chinese growth mean a bigger Chinese government spending package is coming, and a weaker global growth outlook mean that it is coming sooner?

Markets are certainly pricing it this way. The iron ore stocks in particular have reacted to poor Chinese growth numbers by outperforming rather than underperforming – seemingly pricing in the expectation that China will need major stimulus yet again.

Reflexivity question 3: Does a weak stock market suggest another “Shanghai accord” is likely?

In 2015 China went through a similar period of weak growth, stock markets declined and the oil price plunged. The situation ended with the US Fed pausing its upgrades and the US dollar stopped rising. The rumour is that a secret deal was made between central banks at a meeting in Shanghai to limit the USD which would give room for China to stimulate its economy.

Given the trade tensions and a US economy growing quickly, this did not look likely 3 months ago. Fast forward to today and a deal is now more possible.

Reflexivity 3: Brexit

The biggest issue for Brexit is that there is no easy solution that will satisfy everyone and the default option is a hard Brexit which will cause the most disruption and be the most damaging economically.

Politically, this means that the advocates of a hard Brexit can get what they want without having to take responsibility for the decision – simply stymie any proposals for a soft Brexit and then sit back and wait.

As an example of reflexivity, in 2008 US politicians voted against a bail-out for financial markets. The stock market then fell almost 10% and then US politicians changed their minds.

Reflexivity question: Will a globally weak stock market prompt UK politicians to avoid a hard Brexit?

Maybe, maybe not. I suspect for those looking for a hard Brexit, weak global stock markets provide a semblance of cover – blame any weakness on “global issues” and wait. If stock markets were strong globally but the British market was down significantly with the prospect of a hard Brexit then maybe a few swaying voters may have been influenced.

The outcome of Brexit still hangs in the balance, but as it stands I suspect the prospect of Brexit is adding to the woes of global stock markets – but the woes of global stock markets are not helping the prospect of a less economically damaging Brexit.

Reflexivity Conclusions

Markets are caught in a self re-inforcing downward cycle which needs a circuit breaker. A circuit breaker occurring is more likely than no circuit breaker. But there are still risks.

For now, we don’t believe there have been structural effects on growth, which would suggest that a significant rally is possible with resolution – but there are a lot of moving parts and variables.

For the moment we are holding lots of cash and bonds and waiting for the right opportunity.

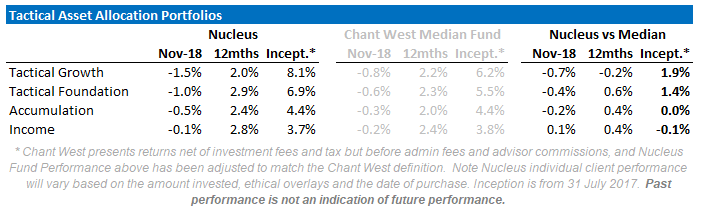

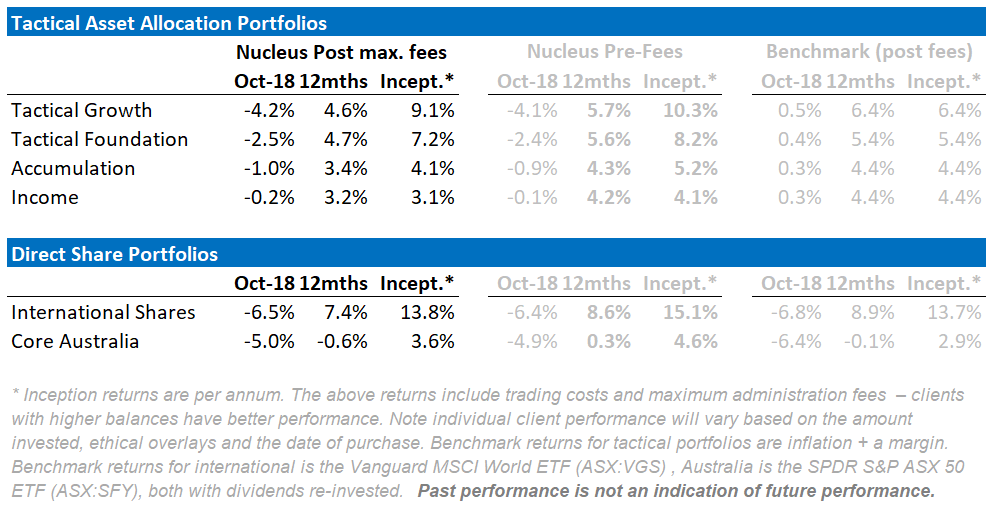

Tactical Asset Allocation Portfolio Positioning

In our tactical portfolios, we own cash, bonds, international shares and Australian shares. We tend to blend these portfolios for clients so that each investor receives an exposure tailored to their own risk and income requirements.

The broad sweep of our asset allocation over the last 18 months was to ride the Trump Boom, switch into Europe in March / April last year as the US became overvalued and then switch back into the US as the Euro rallied and the USD fell.

We remain underweight shares in aggregate, overweight bonds, marginally overweight international shares and significantly underweight Australian shares.

Over / Underweight positions by portfolio

Individual Stock performance

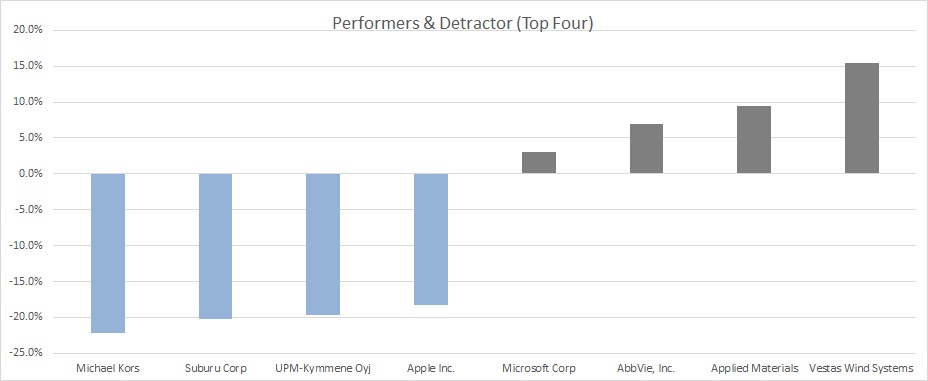

November was a better month for the international portfolio with around half or stocks posting positive returns. Some of performers were rebounds from October lows (Microsoft, Applied Materials) but others reflected sector rotation into more defensive sectors like Drug manufacturers and Renewables (AbbVie, Vestas). Most notable detractor was Apple that has fallen from favour on the back of lower demand concerns.

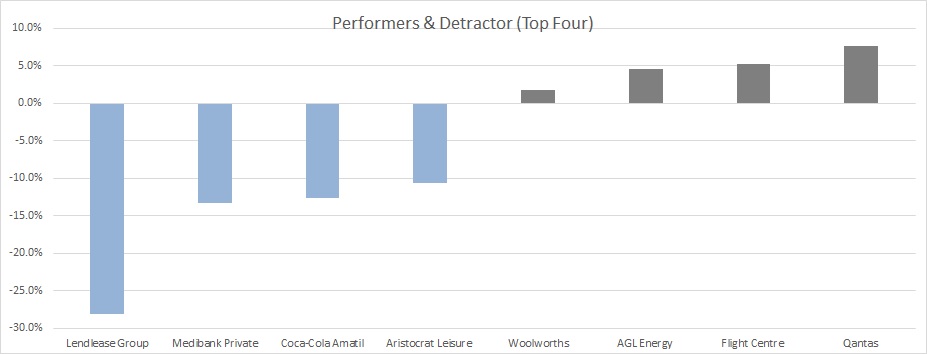

Domestically the detractors were companies disappointing the market with increased costs (Lend Lease), lost contracts (Medibank) or lower guidance/profits (Aristocrat/Coca Cola). Performers were in the more defensive areas of Food/Energy Retail and Travel.

Epilogue

In summary, our view continues to be that Australian investors should continue to hold minimum weights for Australian shares at this point in the cycle. Our intention is that our portfolio is positioned to take advantage of our key themes but minimise risk in the event that our themes take longer than expected to resolve themselves.

We retain relatively large cash and bond balances to hedge against volatility and to look for a cheaper entry point. If markets continue to be weak then we will look to buy more international equities. We are concerned about the potential for trade wars or an emerging markets crisis. These will be a key focus for us over the next few months.

Recent months have been a reminder for investors about the benefit of positioning and of taking profits when markets rise. Markets are still clearly not without risk.

———————————————————-

Damien Klassen is Head of Investments at Nucleus Wealth.

Footnotes:

- In 1937 the US Fed raised rates too quickly as the US emerged from the Great Depression and caused another recession

Damien Klassen is Head of Investments at the Macrobusiness Fund, which is powered by Nucleus Wealth.

The information on this blog contains general information and does not take into account your personal objectives, financial situation or needs. Past performance is not an indication of future performance. Damien Klassen is an authorised representative of Nucleus Wealth Management, a Corporate Authorised Representative of Integrity Private Wealth Pty Ltd, AFSL 436298.