DXY rebounded last night. CNY and EUR were weak:

AUD lifted a little versus DMs:

CFTC was out late and showed another small draw in shorts to -50.8k:

And was mixed against EMs:

Gold held its gains:

Oil dumped again. It requires US output to slow:

Base metals were weak:

And big miners:

EM stocks got hit:

Junk held up:

Treasuries sold:

And bunds:

Stocks were hit in Europe but did a bit better in the US:

Westpac has the wrap:

Event Wrap

US job openings rose 119k to 7,079k in October (vs 7100k expected), after falling 333k in September to 6,960k (revised from 7,009k), and that followed a record high of 7,293k in August. The job openings rate rose to 4.5% from 4.4%, the hiring rate rose to 3.9% from 3.8%, and the quitters rate – a closely followed metric of confidence in employment prospects – edged back to 2.3% from 2.4% but remains at a historically elevated level. Overall, the report reflects a still-tight labour market.

UK PM May postponed Parliament’s vote on a Brexit agreement and would not specify a new vote date. UK media suggested May’s minority Government could have been defeated by around 200 votes (out of a total of 650).

Event Outlook

NZ: Electronic retail spending in November is estimated to have risen by 0.3%.

Australia: Nov NAB business survey conditions were last at 12, having eased in recent months.

Euro Area: Dec ZEW survey of expectations was last at -22 with forward looking sentiment much weaker over 2018.

UK: The eagerly awaited Parliament votes on Prime Minister May’s Brexit withdrawal agreement with the EU was to occur tonight but has been delayed. Oct ILO unemployment rate is expected to remain low at 4.1%.

US: Nov PPI is out ahead of the CPI release tomorrow. Nov NFIB small business optimism is released.

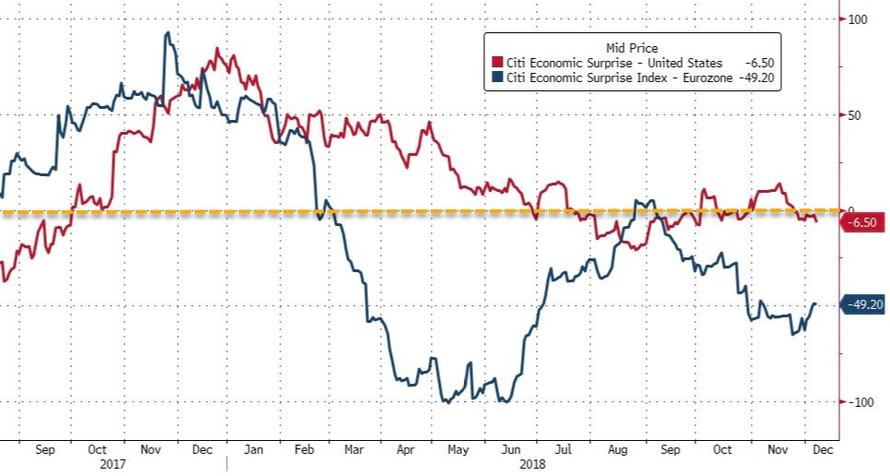

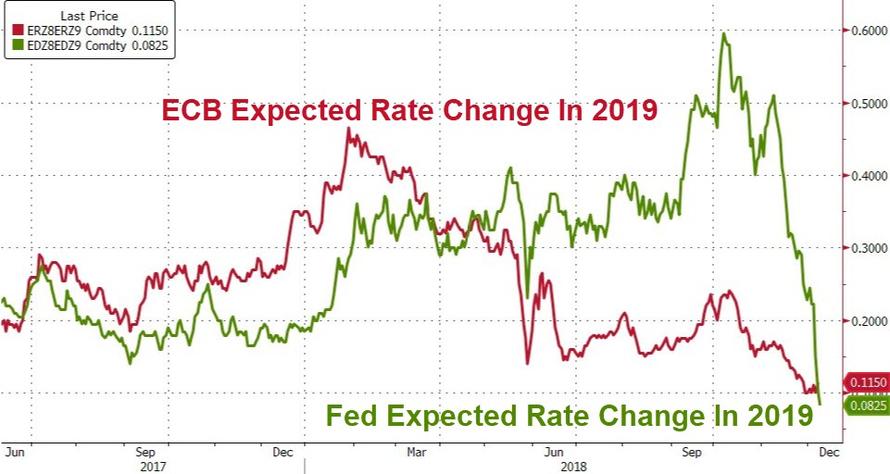

A couple of charts from ZH explain the resilience of the USD despite rapidly falling Fed hike expectations. Simply put, the US is still the cleaner dirty shirt versus Europe and EUR:

Fed dovishness has outpaced ECB now:

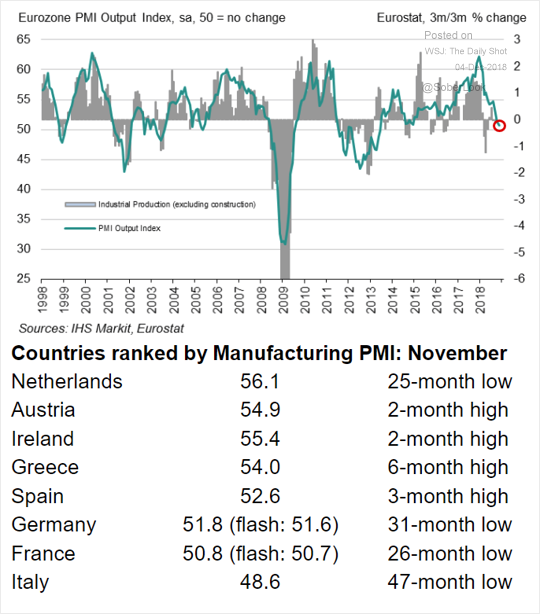

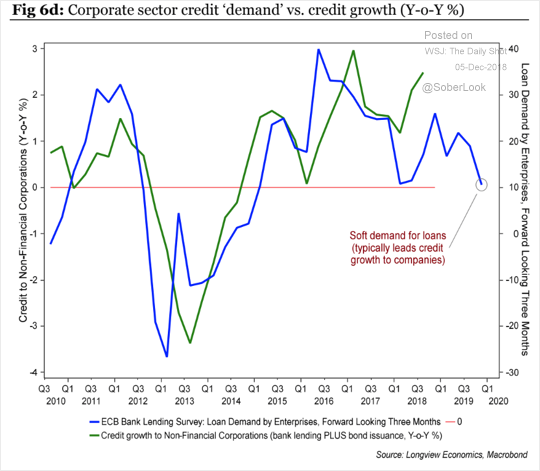

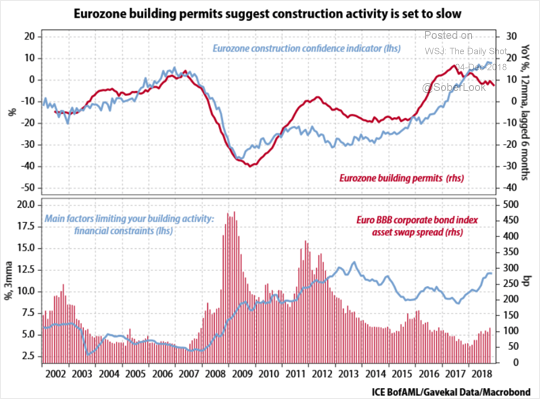

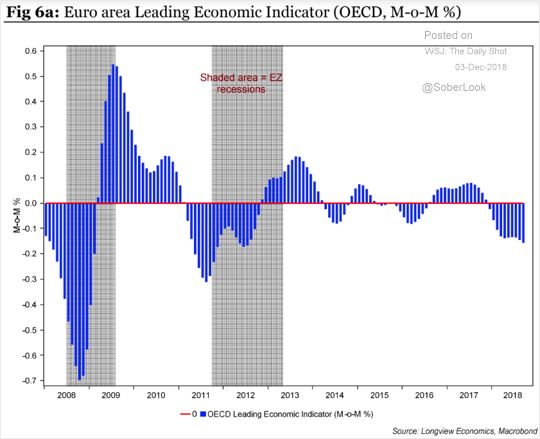

But the ECB is way behind the times with growth falling fast.

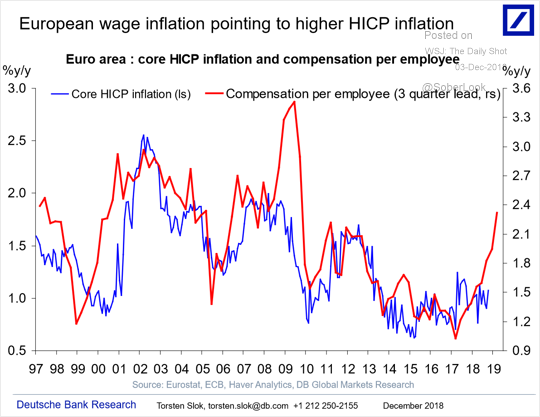

The one thing still keeping the ECB interested is wage growth:

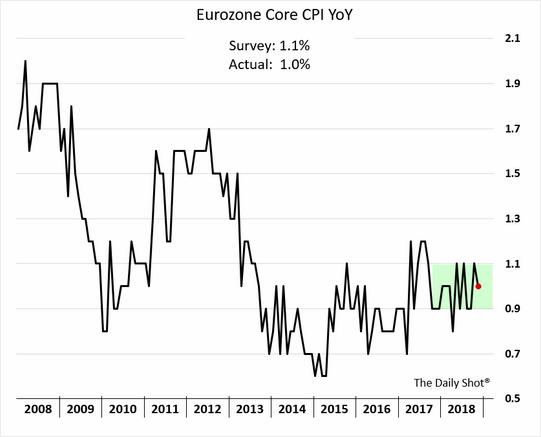

But core CPI is going nowhere as oil crashes:

Europe can’t outrun the US by itself so it is helping keep DXY aloft.