It’s been a straight risk-off session here in Asia as the Huawei headlines are fracturing the possibility of a trade deal between the US and China, fueling safe haven bids and dumping of stocks. US Treasury yields continue to fall while commodity currencies their downward trajectory as markets expect a dour night on Wall Street as traders return from the state holiday.

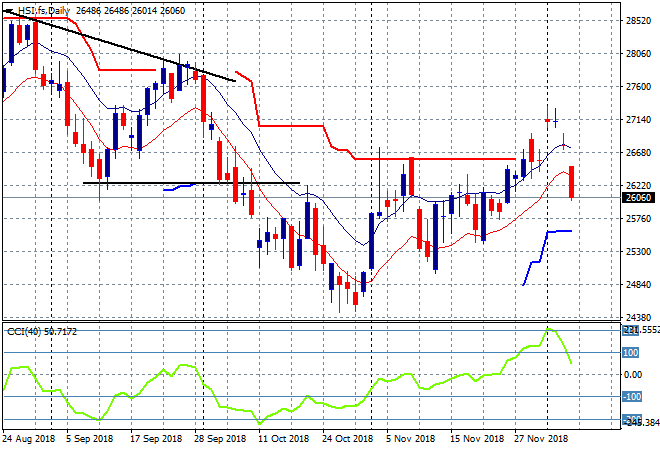

The Shanghai Composite is selling off sharply going into the close, down over 1.5% to 2606 points, barely hanging on above the previous support level at 2600 points. The Hang Seng Index has retreated even further, down nearly 3% to 26067 points, slumping below the previous support level, the low moving average and ATR trailing resistance at 26700 points, creating another dead cat bounce:

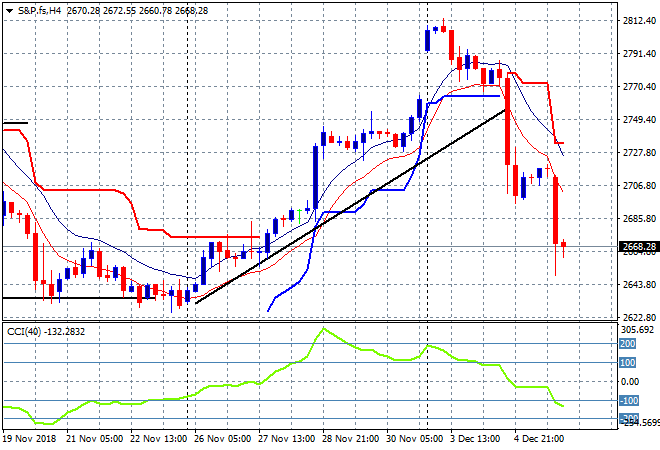

US and Eurostoxx futures have fallen sharply going into the London open, with the four hourly S&P 500 futures chart showing a market that will fall tonight on the re-open after yesterdays holiday:

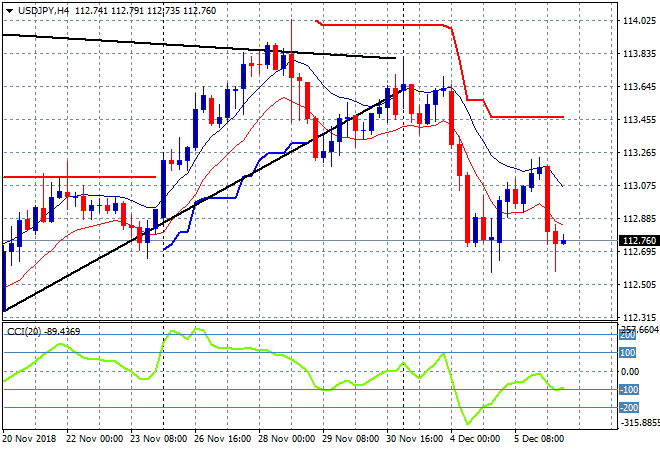

Japanese stocks have slumped as well as Yen buyers stepped in, with the Nikkei 225 closing 1.9% lower to 21501 points, making a new weekly low. The USDJPY pair has also made a dead cat bounce with a sharp retracement after last night’s meagre bounce up to the high moving average, falling back to the mid-week low at the 112.70 level:

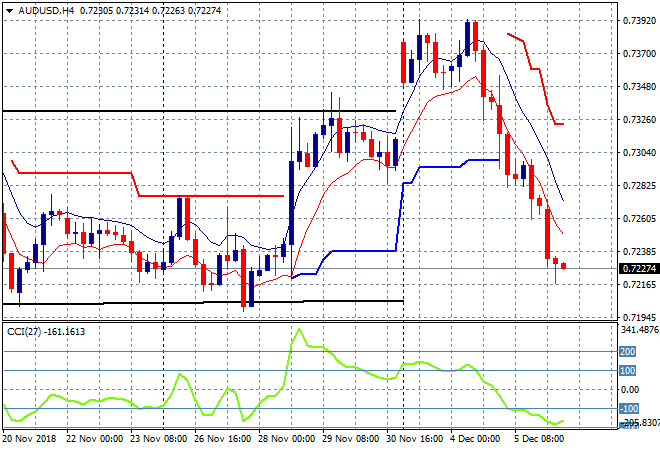

The ASX200 was the best of the region, falling only 0.2% lower to 5657 points, as the trade balance and retail sales numbers didn’t disappoint as expected. The Aussie dollar however continued its slump, remaining well below the 73 handle and now almost back to the previous weekly lows:

The economic calendar has three releases/speeches to watch out for tonight, starting with the moved ISM non-manufacturing print, followed by the DOE oil inventory report and finished off by a speech from Fed Chair Powell.