DXY was strong Friday night and it looks primed for a break out. EUR and CNY were weak:

AUD was hosed across developed markets:

EMs were even worse:

Advertisement

Shorts continued to pull out of AUD last week, now down to -46k contracts:

Gold was soft:

Advertisement

And oil:

Plus base metals:

Big miners fell:

Advertisement

EM stocks too:

Junk was soft:

Treasuries were bid:

Advertisement

Bunds too:

Stocks look like they want go lower yet:

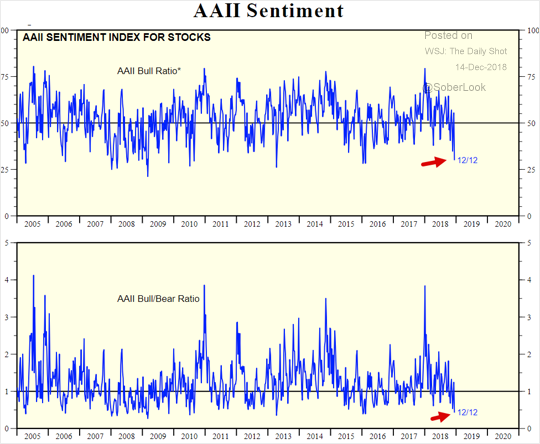

Despite poor sentiment:

Advertisement

So, why do I say that the Australian dollar looks likely to go lower ahead? Basically, we know that the US is slowing and the Fed is likely to pull back on tightening. The problem is, the wider world is slowing even faster:

And China look set to decelerate very sharply in H1, 2019:

Advertisement

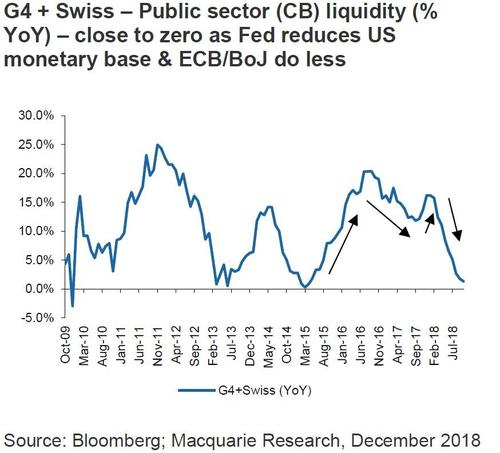

As well, the excellent Viktor Schvets of Macquarie notes liquidity is key:

Is the coast clear? It is not safe; too many sharks out there

‘Well this is not a boat accident! It wasn’t any propeller! It wasn’t any coral reef! And it wasn’t Jack the Ripper! It was a shark!’ As in ‘Jaws’, investors are now trying to assess whether there are sharks out there in the dark waters ahead, and what signals should they watch? Is it trade, politics, CBs, extraditions, retaliations, fiscal stimuli, spreads, private equity (arguably the single most overvalued and least liquid asset class), FX, oil or other uncertainties that could sink the boat? Who is selling and what does it mean? As we saw in ‘97-98 or ‘08-09, trying to anticipate whether it would be Russia, LTCM, subprime or Lehman’s PN business that would change everything is a fruitless exercise. We will know when we do. The value of a single signal by itself is limited, and the headlines that ‘we have just discovered the signal’ are not worth much.

Having said that, there is an underlying ‘heart beat’ that tells investors whether the general direction is towards a greater disinflation or reflation. In a world dominated by asset prices, there is a need to generate more liquidity and debt than economies require. We no longer live in a conventional capitalism; there are no recognizable cycles, and late cycle arguments mean little, when public sectors determine their duration and strength.

In a modern economy, it is all about tax cuts, fiscal stimuli and manipulation of yield curves & rates. Indeed it makes sense, as generating excess liquidity & corralling volatilities is the only way to guide highly financialized economies. It does however lead to a Matrix world of random signals, turning what only days ago seemed solid into liquid.

…ultimately the world does not work if liquidity drains & reflation slows.

This brings us to the latest ‘signals’. First, we had Powell changing tune in space of less than eight weeks from ‘far from neutral’ to ‘just below neutral’, altering expectations of a tightening cycle, and pushing US$ lower. Second, we had a plethora of news regarding the trade war. China apparently agreed to buy a bit more US soybeans (~0.5m tons) and is willing to re-phrase and underemphasize its ‘China 2025 policy’. Third, it appears that the Italian populist Government is folding on its budget spending. It is enough to reflate sentiment and markets by lowering probabilities of more extreme outcomes.

Unless economies evolve in strongly positive or negative ways, it is this flow of random signals that drives markets, which in turn impacts economies in a complex and iterative process. However, at the end of the day, unless CBs reverse their contractionary stance, global liquidity would continue to drain, and unless China and US alter their policies, global reflationary momentum would weaken.

The world cannot function unless China and the US see ‘eye to eye’ and Eurozone avoids implosion. It is possible that we might find a middle ground, but it would require a miracle; at least in the absence of a greater dislocation.

We maintain that while China would like to find a compromise, it can never give up its state-driven model and EU is still facing a revolution in ’19. There are also uncertainties of a divided Congress that could either lower or raise US$ (depending on whether US accepts slower growth or stimulates).

Despite recent relief, direction remains disinflationary; the coast is not clear.

Advertisement

Although the Fed will lower its tightening outlook and revert to a data-driven, month-to-month reaction function, it won’t be easing any time soon. That makes it tough for China to make the shift from iterative easing to aggressive kitchen sink stimulus given it must protect the yuan for its own reasons and if it is not going exacerbate the trade war.

While this context lasts it is AUD negative. Add that Australia now confronts a toxic H1, 2019 as the housing bust combines with the federal election and tumbling commodity prices to force the RBA to slash rates.

That ought to be enough to take the AUD into a new and lower trading range until the Fed, China or both panic once again.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.