DXY was soft last night. CNY too. EUR better:

AUD was hosed across developed markets:

And emerging:

Gold tried and failed to rally:

Oil was smashed:

Base metals fell:

Big miners broke:

And EM stocks:

Also junk:

Treasuries boomed:

As did bunds:

Stocks fell sharply but recovered losses:

Westpac has the wrap:

Event Wrap

US Services ISM index defied expectations and rose back toward near record levels in November, hitting 60.7 compared to consensus expectations for a pullback to 59, from 60.3 last month. New orders and prices paid advanced while employment intentions cooled slightly, though they remain at historically high levels. The ISM survey underscores robust conditions for the US, in contrast to the increasingly cautious message on the economy from markets. Markit’s Services PMI for Nov was revised up too, from 54.4 to 54.7. Other US data points were on the modestly softer side; ahead of Friday’s non-farm payrolls the ADP Research Institute’s private payrolls report showed a +179k gain in November, slightly shy of expectations for a +195k gain, the trade deficit widened to its largest levels in 10 years ($55.5bn) with the politically delicate deficit with China hitting a record high of $43.1bn, while durable goods orders for October were revised down to show a steeper 4.3% decline from an initial estimate of -2.4%.

German October factory orders rose +0.3% (expected -0.4%), though September was revised to +0.1% (from +0.3%). This was a welcome relief after persistently disappointing data from core Eurozone.

RBA Dep. Governor Debelle said in a speech there is still scope for further reductions in the policy rate if required by economic conditions, and that they could deploy QE in a future crisis. On housing he said banks’ nervousness about lending at a time of falling house prices risks exacerbating the slump.

Event Outlook

China: Nov foreign reserves data is released.

Euro Area: Q3 GDP 3rd estimate will finalise the 2nd estimate of 0.2% and provide the expenditure breakdown. By country, Germany’s 0.2% contraction relating to a significant drop in net exports – a likely one-off – weighed on the Euro Area’s growth in the quarter.

US: Nov non-farm payrolls are expected to rise by 198k with an unchanged unemployment rate at 3.7% as well as average hourly earnings at 3.1%yr. Dec University of Michigan consumer sentiment is released. Fedspeak involves Brainard on financial stability and Williams in conversation with former BOE Governor Mervyn King in NY.

Captain Obvious can call this one, via the FT:

China’s government has demanded the release of Huawei’s chief financial officer, whose arrest in Vancouver on US sanctions-busting charges sent financial markets reeling from the widening confrontation between the world’s two largest economies.

In an angry rebuke issued on Thursday, the Chinese embassy in Ottawa accused US and Canadian authorities of having “seriously harmed the human rights” of Meng Wanzhou, the daughter of Ren Zhengfei, founder of the Chinese telecoms group.

Diplomatic and intelligence officials briefed on the case said the US was pursuing Ms Meng as part of a criminal probe related to attempts by Huawei to sell US-made equipment to Iran, a move that could be in violation of sanctions against the country.

Also of keen interest, OPEC is struggling, at Bloomie:

OPEC ended talks without a deal on oil production cuts for the first time in nearly five years as Russia flexed its muscles by so far refusing to commit to the big output curb that Saudi Arabia is demanding.

After two days of talks in Vienna, Saudi Energy Minister Khalid Al-Falih said he isn’t confident of an agreement when the Organization of Petroleum Exporting Countries meets again with its allies on Friday. A proposal for a combined OPEC and non-OPEC cut of 1 million barrels a day was left dangling in uncertainty.

“Not everybody is ready to cut equally,” Al-Falih told reporters in Vienna. “Russia is not ready for a substantial cut.”

So much for that G20 bonhomie.

To sum up, if the Huawei issue isn’t resolved then it could derail the trade rapprochement, such as it is. That’s anybody’s guess so is an ongoing market headwind.

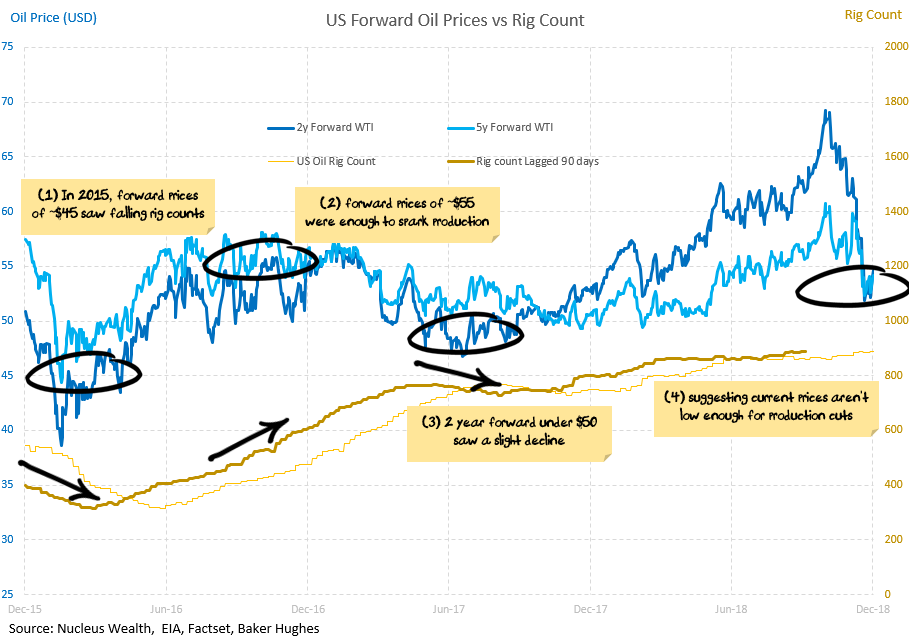

OPEC is a boon. If it had cut enough to push oil back up then the Fed would be snookered. As it stands, oil will have to fall further to cap US shale instead:

Assuming oil falls further, the Fed is one and done in December. An oil patch recession will kill inflation and cap wage growth. The WSJ signaled as much last night which is what saved stocks:

Federal Reserve officials are considering whether to signal a new wait-and-see mentality after a likely interest-rate increase at their meeting in December, which could slow down the pace of rate increases next year.

Officials still think the broad direction of short-term interest rates will be higher in 2019, according to recent interviews and public statements. But as they push up their benchmark, they are becoming less sure how fast they will need to act or how far they will need to go and want to assess how the economy…

The question now is when does ‘bad news is bad news’ become ‘bad news is good news’ for equities as bond yields tumble? I’d guess not much further down unless Huawei tuns really nasty. US growth is going to slow sharply not collapse as a supportive Fed approaches.

For the Australian dollar, headwinds and tailwinds are shifting. A stalled Fed helps take upwards pressure off the USD, though not that much given everyone else is still in worse shape. Moreover, tumbling oil is bad for all commodity prices and will weigh on the AUD to that extent.

One way or another it appears that, in the short term at least, the AUD rally is already over.