DXY was slammed then bud last night. EUR is stable. CNY on a tear:

AUD flamed out across DMs:

EMs were worse:

Gold is breaking out as Fed easing looms:

OPEC couldn’t get bid under oil. Just as well, markets would not like it now:

Base metals were mixed:

Miners fell:

EM stocks were smashed:

Junk too:

Treasuries were bid hugely at the long end:

Bunds too:

DM stocks were pounded:

Westpac has the wrap:

Market Wrap

Global market sentiment: Sentiment reversed overnight amid uncertainty regarding the recent US-China trade war truce. The S&P500 is down 2.6%, bond yields are lower, and the US dollar is higher.

Interest rates: The US 10yr treasury yield extended a month-old decline, from 2.97% to 2.88% – the lowest since early September. 2yr yields fell from 2.84% to 2.79. Fed fund futures continued to price the chance of the next rate hike on 19 December at 80%.

FX: The US dollar index rebounded from noon London. EUR initially rose to 1.1420 but fell in NY to 1.1320. USD/JPY extended a multi-day decline to 112.60, the safe-haven yen outperforming. AUD initially nudged up to 0.7394 – a high since early August – but fell as risk aversion developed to 0.7326. NZD initially rose to 0.6970 – a high since mid-June – before falling to 0.6920. AUD/NZD fell from 1.0625 to 1.0585.

Event Wrap

No data to report.

Fed voter and moderate Williams said the economy remains on a strong path, and further rate increases over the next year make sense. Non-voter Kaplan said “we are in a more challenging period in our efforts to normalize policy”.

The Brexit debate in UK’s Parliament began, with a vote scheduled for 11 December. Earlier overnight, there was a defeat for the Government in a vote on Parliamentary powers to vote on other options if PM May’s deal is ultimately rejected.

Event Outlook

NZ: Q3 construction work is expected to rise by 2.3%. This data typically does not move markets, but it does feed into GDP estimates.

Australia: Q3 national accounts are released with the consensus forecast for GDP growth to be up 0.6%, 3.3%yr. Westpac’s forecast is 0.6% with domestic demand up 0.5% and partial data indicating inventories making a -0.3ppt contribution and net exports a +0.4ppt contribution.

India: the RBI policy decision is expected to be on hold.

US: Nov ISM non-manufacturing is seen to edge down to a still very positive level of 59.0. The Federal Reserve Beige Book is released covering regional economic conditions.

Canada: the BOC policy decision is anticipated to be on hold with growth and inflation around the Bank’s targets.

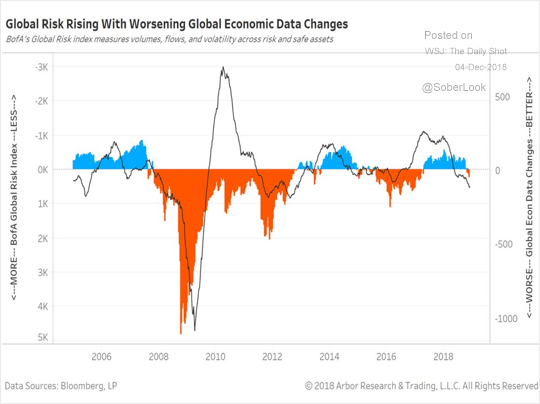

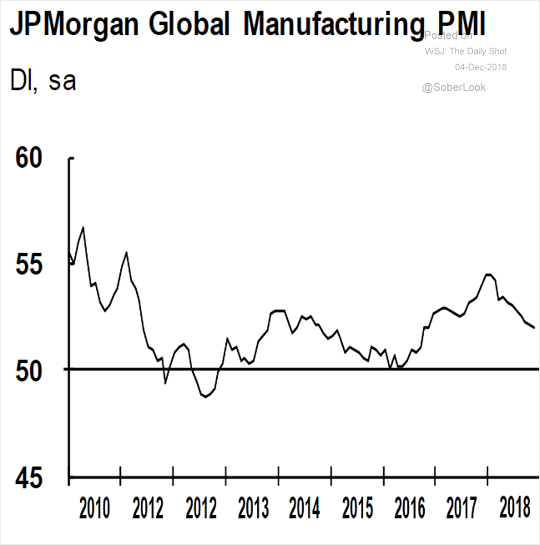

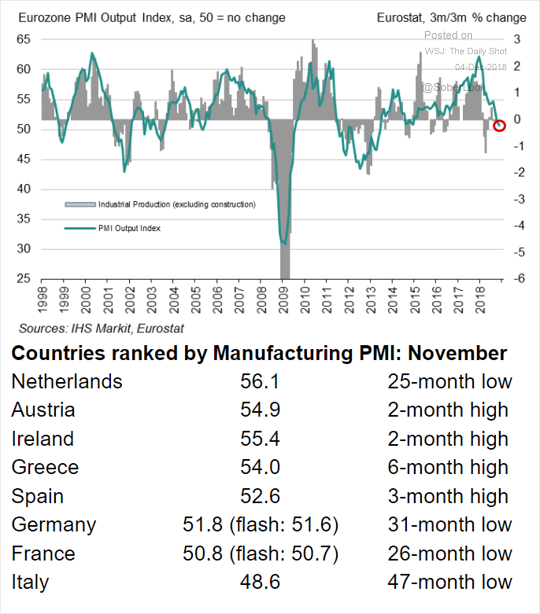

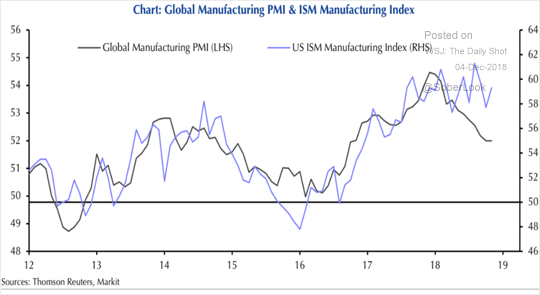

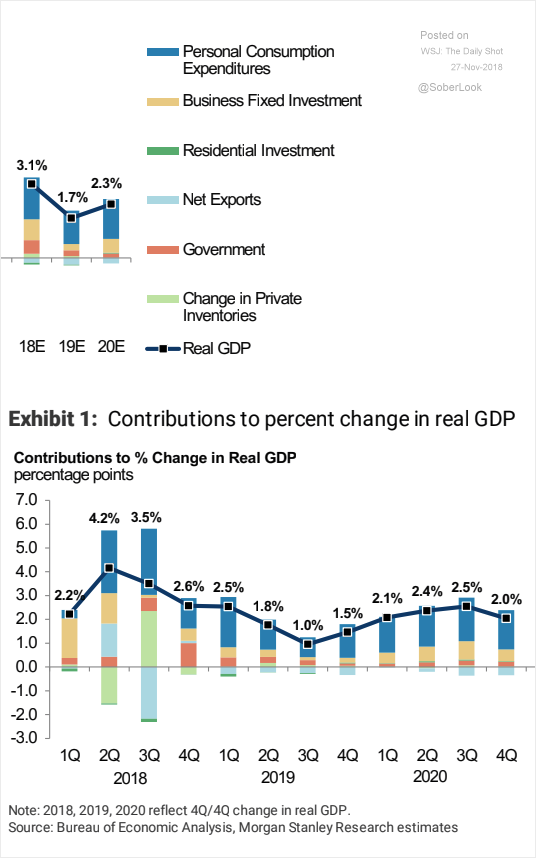

We’re now into global growth scare territory. Data is not too bad but is trending the wrong way:

And we know that the US is going to slow sharply ahead thanks to its fiscal cliff:

And so is China given its credit flow:

The present mix of richly valued asset prices and rising interest rates does not makes sense in the emerging growth challenged macro regime.

As for the Australian dollar, it still has upwards momentum from the cessation of trade hostilities but growing is groaning under the downwards weight from fading global growth prospects and falling commodities. For now the former is still prevalent but if the shift towards repricing growth lower continues then the weight on AUD will grow.