ABC 7.30 Report last night aired the first of a three part special on Australia’s budding housing bust, which is well worth watching.

The episode first features auctioneer, Damien Cooley, who has seen buyer interest evaporate:

DAMIEN COOLEY: The market is challenging for me. An auctioneer is only as good as the product they are selling.

Advertisement

It then features an interview with UBS chief economist, George Tharenou, who expects prices to keep falling into 2020:

GEORGE THARENOU: Initially, it was generally higher-priced homes in Sydney and Melbourne for investors, but that downturn has now spread and this is the concern that I have, is that the likelihood of Australia facing the longest housing downturn in history has increased.

And it seems quit plausible to me that house prices will continue to fall into next year into 2020…

We have just had this multidecade period where lower and lower rates went into higher and higher debt and higher and higher house prices…

The mechanism and the main driver of the correction this time is a credit tiding. It is a reduction in borrowing capacity. The problem is I can see what reverses that quickly. It would take a major reversal of policy decisions by the government and the regulators to try to attempt to reflate the housing market and, at the moment, that is not the case.

CoreLogic’s Tim Lawless is then featured:

Advertisement

TIM LAWLESS, HEAD OF RESEARCH, CORELOGIC: Absolutely. The chances of an economic downturn being fuelled by a housing market downturn are heightened at the moment because of the wealth effect, reversible of the wealth effect and fear of transactions in the market…

When you look at the value of housing across Australia, nearly 60 per cent of Australia’s housing value is in two cities – Sydney and Melbourne…

When you look at Australia’s wealth, we see about 55 per cent of household wealth in Australia is in the housing asset class.

About 70 per cent of Australia household debt is in the housing asset class as well.

Australian household debt — it’s tracking at about 190 per cent of disposable income. It has never been that high.

Followed by a migrant family, the Gupta’s, highlighting the housing obsession underpinning the bubble:

BILL GUPTA, PROPERTY INVESTOR: Everyone wants to come to Sydney and Melbourne from overseas. Everyone wants to live in these established cities where the jobs are available. Everyone wants to buy the property here because the value grows in Melbourne and Sydney, as compared to the other states.

GEOFF THOMPSON: The Guptas now own more than 30 properties between them.

GORO GUPTA, PROPERTY INVESTOR: I call it generational wealth. When you are building something with generational wealth, you build it together. So, Yes, I might have a few properties, dad might have a few properties, mum has got a few properties and even grandma has a couple up her sleeves, right.

For us, it is a never ending thing. Buying as much of the monopoly board as one sees fit.

BILL GUPTA: My view is that every 10 years the property doubles while other investments, there is always risk.

The investment bust is then profiled:

Advertisement

DAVID JACKSON, PROPERTY INVESTOR: Major effect has been the borrowing capacity that we have had and the valuations that have dropped, not substantially, but have dropped a fair bit, which has made the major lenders a little bit hesitant to lend against the current values.

GEOFF THOMPSON: Throughout the boom, investor David Jackson was successfully building a

property portfolio. Then, suddenly, an apartment he bought off the plan in central Sydney’s Woolloomooloo was valued at less than he paid.

DAVID JACKSON: In this particular circumstance the valuation came in less than the purchase price, which was news to me after investing in properties for 10 years. Because we are in a small business, bank lending has restricted the amount of debt that we can borrow. So, it has restricted our employment, the number of employees that we can hire.

GEOFF THOMPSON: Increasingly, David’s had to turn to more expensive second-tier lenders.

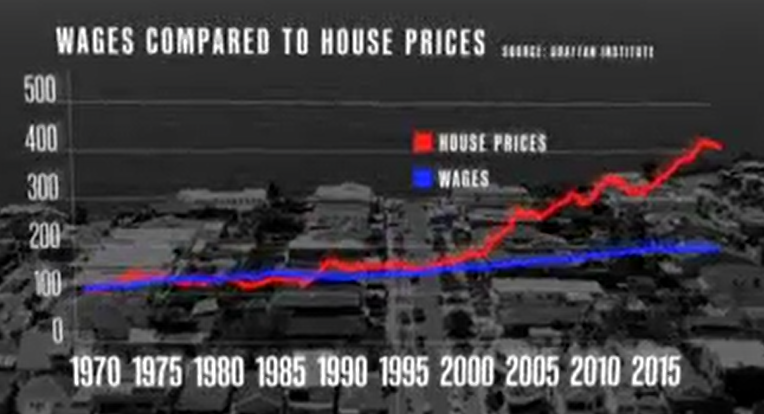

And finally, the “yawning gap” between house prices and incomes is discussed:

JOHN SYMOND: If you said the me 20 years ago, people in 2018, young people are taking mortgages for nearly $1 million to buy a house, I would have said, well, what are you smoking?

We just don’t know what the next 10 or 20 years is going to bring. I will tell you one thing, it will be very, very different.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.