Via the always excellent Jonathon Mott at UBS today:

(1) ‘Underlying’ revenue fell -1.3% (h/h); (2) NIM was down 7bp to 199bp; (3) Average Interest Earning assets grew just 1.4% as the banks further tightened underwriting and continued to run off low yielding institutional assets; (4) Fee income and markets revenue were weaker; (5) ‘Underlying’ costs rose 1.9% (h/h) given ongoing investment, compliance and regulatory spend, which more than offset productivity savings; (6) This left ‘Underlying’ Pre-Provision Profits down 3.6% (h/h); (7) Credit impairment charges fell to just 11bp – the lowest ever recorded.

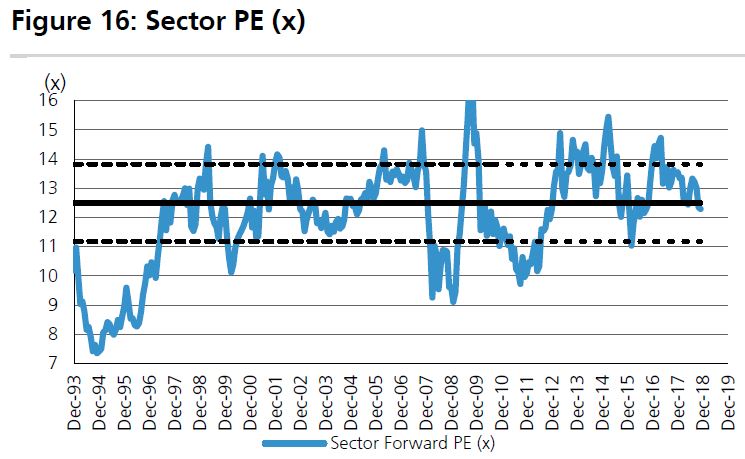

Book pricing is cheap but no good if the assets are dodgy and the forward P/E is still only average:

Yet to be discounted, profit growthless banks with massive payout ratios for huge dividends on record low provisions entering a housing adjustment, regulatory crunch and legal imbroglio.

Now that’s a short!