King Dollar is back. CNY was weak. EUR cracked a big head and shoulders pattern:

AUD was thumped versus USD and JPY, rose against EUR and GBP:

Advertisement

It was a mix versus EMs:

Gold was hammered:

Oil waltzed straight through OPEC cuts:

Advertisement

Base metals were mixed but copper fell:

Big Miners were hit:

EM stocks were pounded:

Advertisement

US junk debt broke. A sell signal:

Treasuries are still not well bid:

Bunds are better:

Advertisement

Stocks were thrashed:

Westpac has the wrap:

Market Wrap

Global market sentiment: The risk-averse mood persisted, reflected by further declines in US equities (S&P500 -1.6%) and US bond yields, and a firmer US dollar. The latter was also helped by Brexit and Italian Budget concerns.

Interest rates: US 10yr treasury futures implied yields fell from 3.18% to 3.15%. Fed fund futures yields continued to price the chance of another rate hike in December at 75%.

FX: The US dollar index is up 0.7% on the day, and at the highest level since June 2017. EUR was one of the worst performers, falling from 1.1325 to 1.1239 –a 17-month low – amid concerns the Italian Budget impasse could escalate. GBP was the worst performer, falling from 1.2950 to 1.2828, amid reportedly waning support for Brexit in May’s cabinet. The safe-haven yen was the best performer, USD/JPY falling from 114.20 to 113.67. AUD slipped further from 0.7235 to 0.7188. NZD also slipped, from 0.6750 to 0.6706 but later recovered. AUD/NZD thus fell further, from 1.0720 to 1.0677 – the lowest since June.

Economic Wrap

There was no major data to report on. Regarding Brexit, there were further negative official and media comments over the lack of potential for a break through this week amidst increased political tension within May’s minority Government. Regarding Italy’s Budget, tensions persisted into today’s deadline on responses to the EU’s rejection of the initial budget proposals, whilst the Italian Government. continued to hold staunchly to their proposals.

Event Risk

Australia: Oct NAB Business survey last showed conditions at +15, a still elevated level but off 2017 highs.

Euro Area: Nov ZEW survey of expectations was last at -19.4 with the forward outlook of financial firms declining over 2018.

UK: Sep ILO unemployment rate is anticipated to show the unemployment rate holding at 4.0%.

US: Oct NFIB small business optimism is expected to remain at a high level of 108.0. Oct monthly budget statement is released. Fedspeak involves Kashkari at a regional economic conference on migration and Brainard and Harker speak at a Philadelphia Fed fintech conference.

Just as expected, as the EUR breaks, AUD falls against DXY. We’re back to the deflating commodities trade with a bullet as EUR breaks down.

Advertisement

Some see European growth as nearing the bottom, from Capital Economics:

The recent flow of both news and data from Europe has painted an increasingly gloomy picture and events this week are unlikely to provide much respite, with Italy’s government facing a deadline on Tuesday to submit a re-drafted budget to Brussels and then GDP data due on Wednesday likely to show that Germany’s economy barely grew in Q3. So how should investors navigate the increasingly troubled waters in Europe?

One of the challenges is distilling the sheer volume of news. Stepping back, though, three major developments over the past couple of months stand out. They are:

a) The weakness of the latest activity data;

b) The stand-off between Brussels and Rome, and Italy’s perilous fiscal trajectory more generally; and

c) The decision by Angela Merkel to resign as head of the CDU and to step down from the Chancellorship when her term in office ends in 2021.

To cut a long story very short, our view is that investors should worry less about (a) and more about (b). And the extent to which (c) becomes a problem depends in part on how quickly and to what extent (b) escalates. Simple, right?

At first sight, the sharp slowdown evident in the latest data should set alarm bells ringing. While the US economy grew by 0.9% (3.5% annualised) in Q3, the euro-zone grew by just 0.2% (or 0.6% annualised). Italy’s economy stagnated and Germany’s economy looks likely to have grown by 0.1-0.2%. (It’s a quirk of European statistics that Germany releases GDP data after we get the euro-zone aggregate.)

But we think that the slowdown in euro-zone growth can be explained in large part by the disruption to auto sectors caused by the rollout of new emissions tests. (See this for more detail.) These new regulations have hit car producers in Italy and Germany especially hard, and both economies appear to have borne the brunt of the slowdown in GDP growth in Q3. In contrast, France and Spain – whose car sectors have been less affected by the new regulations – posted relatively decent GDP figures. (See Chart.)

The key point, however, is that once the disruption caused by the emissions tests fades, there is likely to be a bounce in output in the countries most affected as producers make up for lost time. Brace yourselves for a barrage of negative headlines about Germany’s economy on Wednesday, but our sense is that growth will rebound in Q4.

The challenges posed by Italy appear more intractable. As I’ve noted before, its problem is primarily one of low growth rather than acute fiscal difficulties (the government is actually planning to continue running a primary budget surplus in 2019, 2020 and 2021).

This raises the prospect that Italy might muddle through for a long time, provided that the bond markets remain quiescent. But at low rates of growth the arithmetic that underpin the public debt dynamics become extremely sensitive to small changes in bond yields. And while the EU has so far won all of its battles with fiscally profligate governments, there is no sign yet that Rome will back down. It’s not difficult to see how all of these risks could crystalise as the ECB shifts from policy accommodation to policy tightening in 2019.

This is where the recent political developments in Germany start to come into play. The decision by Angela Merkel to step down as the head of her party, the CDU, was expected at some point, and it was likewise understood that she was likely to step down as Chancellor when her current term expires in 2021. The immediate implications for Germany’s economy are limited.

Instead, the much bigger issue is that Mrs Merkel’s decision to step back comes against the backdrop of German government coalition that is already starting to fray around the edges. Even if the coalition survives, there is a risk that a disjointed government in Berlin will be less able to lead a rapid response to problems in Italy if they intensify. And there is now an even greater question mark hanging over the more fundamental issue of euro-zone reform. The key message, then, is that when thinking about the outlook for Europe’s economy, we should focus less on the latest quarterly growth numbers that are grabbing the headlines and more on the structural challenges that remain at the heart of the euro-zone.

I am less bullish on any rebound. As China slows the Eurozone will too via its exports. Other key indicators are also waning. To me, Europe is simply slipping back to its trend growth as the globe slows, which is a relatively weak sub-2%.

Advertisement

Even as US growth comes back to the pack, I can’t see the ECB reaching monetary take off this cycle so still see the bullish case for USD as predominant.

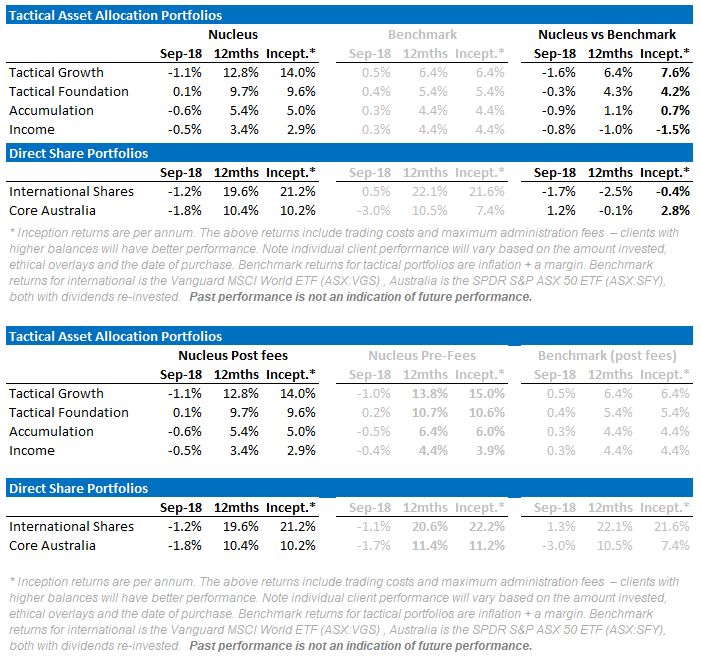

David Llewellyn-Smith is chief strategist at the MB Fund and MB Super which is long US equities that will benefit from a falling Australian dollar so he is definitely talking his book. Below is the performance of the MB Fund since inception:

Advertisement

If the ideas above interest you then contact us below.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.