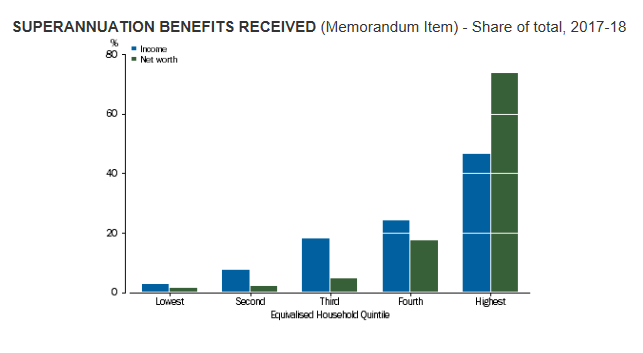

The ABS yesterday released the below chart showing the disproportionate superannuation benefits received by high income earners:

Superannuation benefits received are recorded as a memorandum item of the household income account. Superannuation benefits received in the ASNA are treated as financial transactions of households and are not recorded as income; instead they are recorded in the financial account and balance sheet.

The full text of this article is available to MacroBusiness subscribers

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.