By Chris Becker

Another poor night for equity markets with news of the Brexit deal impacting European bourses in a perverse way, rallying before realising it’s not that good and selling off into the close. The US CPI print did not cause a flutter with currencies reacting more to the EZ CPI and GDP prints instead, which slightly missed expectations with lower results. Oil prices stabilised after their mammoth drop in recent weeks but is it over yet? Poor Saudis…

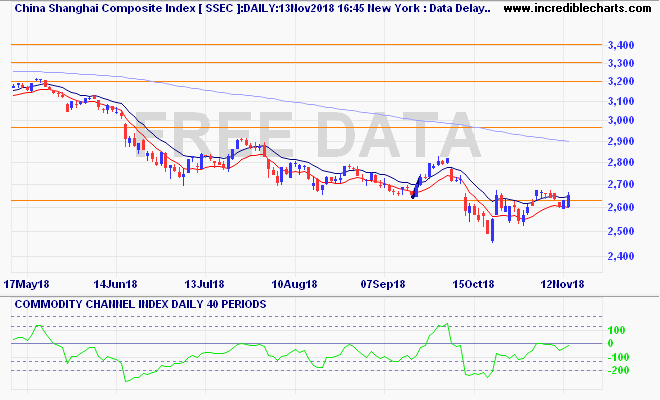

Recapping Asia’s session yesterday where the Shanghai Composite closed nearly 0.8% lower to 2633 points, retracing most of the previous session build above key support at the 2600 level as the retail sales data took the edge of recent confidence. The daily chart shows the potential of a slowdown in this long standing correction, but price must maintain itself above 2600 here to translate that into a recovery rally:

The full text of this article is available to MacroBusiness subscribers