No big news to move stocks around here in Asia, just a series of headlines over Chinese trade, Brexit and local politics to get through another trading day. Interestingly, the CBOE has increased oil future margins, which is a case of closing the door after the horse has bolted, while the latest New Zealand trade figures with record deficits hasn’t upset the Kiwi as expected.

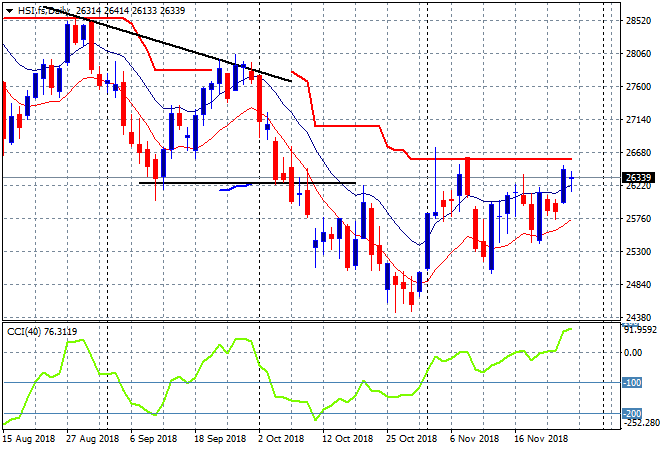

The Shanghai Composite is up 0.1% to 2579 points going into the close, struggling to make any traction here quickly get back above key support at the 2600 point level. The Hang Seng Index is off about the same, sitting at 26349 points, still above the previous support level at 26000 points as the the daily chart is starting to stabilize:

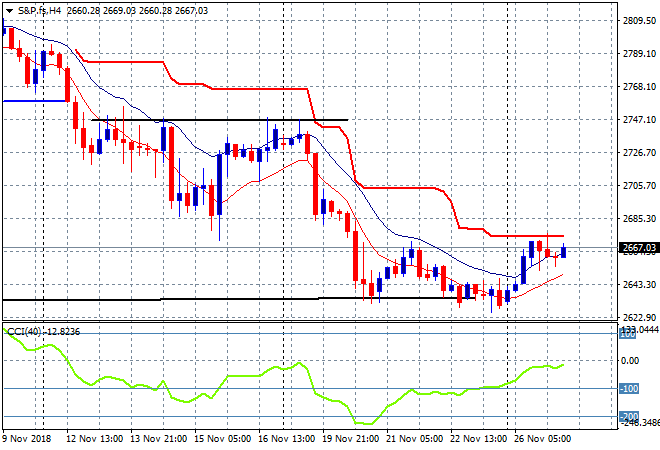

US and Eurostoxx futures are up slightly with the four hourly S&P 500 futures chart showing a potential breakout above trailing ATR resistance at 2675 points or so, but there’s significant resistance above that level as well:

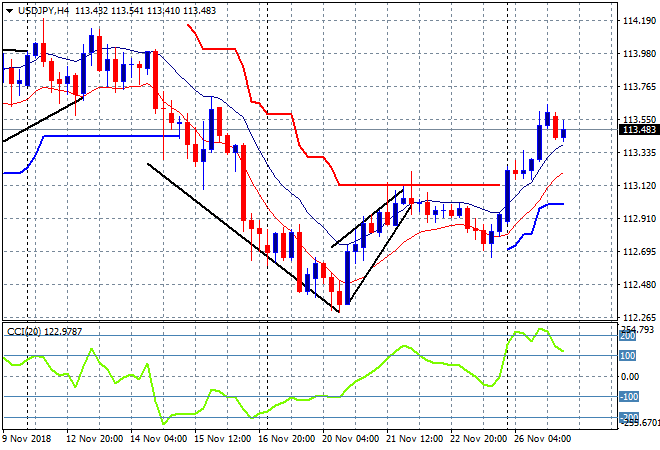

Japanese stocks have put in a solid day as expected, helped by a much weaker Yen from overnight, the Nikkei 225 closing 0.8% higher to 21986 points. The USDJPY pair has come back slightly after shooting significantly above both trailing ATR resistance and the 113 handle yesterday, now in a slightly overbought trajectory:

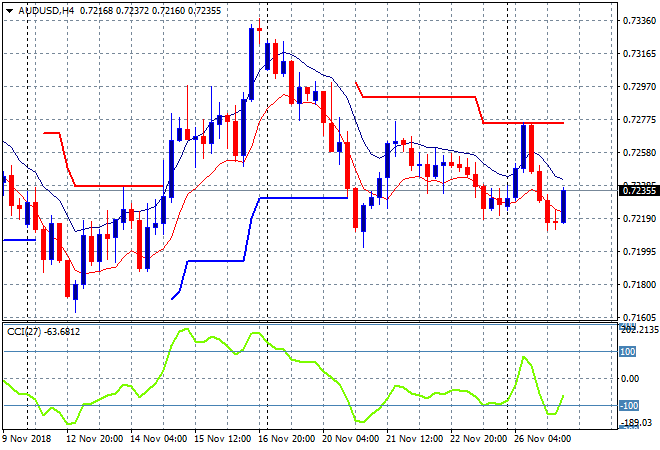

The ASX200 played catchup by launching exacntly 1% higher today, closing at 5728 points, finally getting back above the 5700 point support area. The Aussie dollar has blipped higher after a solid retracement overnight with a surge back up to the 72.30 level, but this is looking weak going into the City open:

The economic calendar has two major releases in the US to watch closely tonight, first September house prices and then consumer confidence figures for November.