Stocks across the region were mixed today with the local bourse falling nearly 2% on the back of another rout in banks, while the trifecta of Chinese data also proved a little dicey even though on most metrics they were good figures. The oil price and their effect on energy stocks plus the Brexit deal will be the main catalysts for risk markets tonight but there’s also a lot of economic data to absorb.

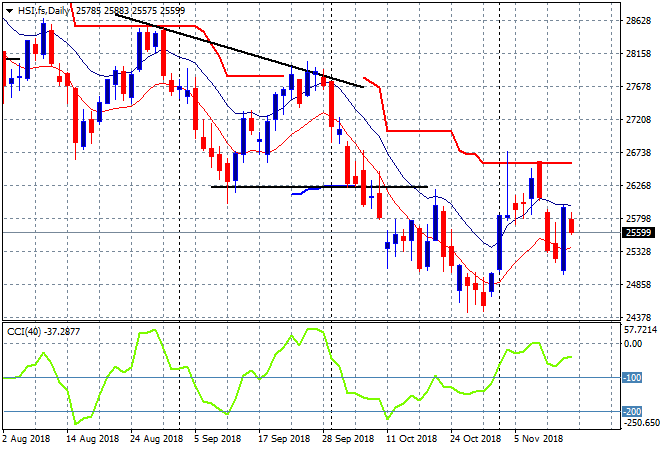

The Shanghai Composite has closed nearly 0.8% lower to 2633 points, retracing most of the previous session build above key support at the 2600 level as the retail sales data took the edge of recent confidence. The Hang Seng Index is off a similar amount, down 0.6% to 25614 points, with the daily chart again displaying an inability to get back to the previous support level at 26000 points:

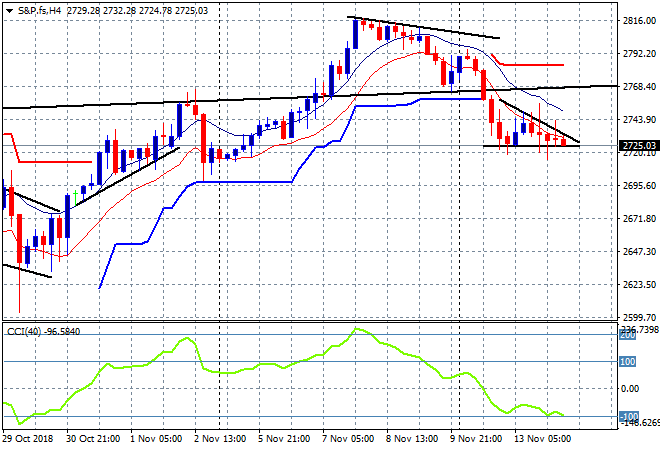

US and Eurostoxx futures are down slightly with the four hourly S&P 500 futures chart showing a potential breakdown with a descending triangle on very tentative support at the 2725 point level:

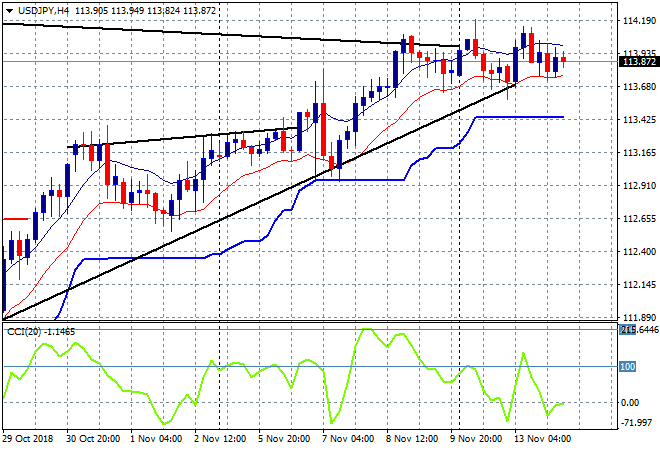

Japanese stocks lifted ever so slightly, with the Nikkei 225 closing up 0.2% to 21846 points. The USDJPY pair is treading water and looks set to tackle last week’s high again above the 114 handle after another staid session:

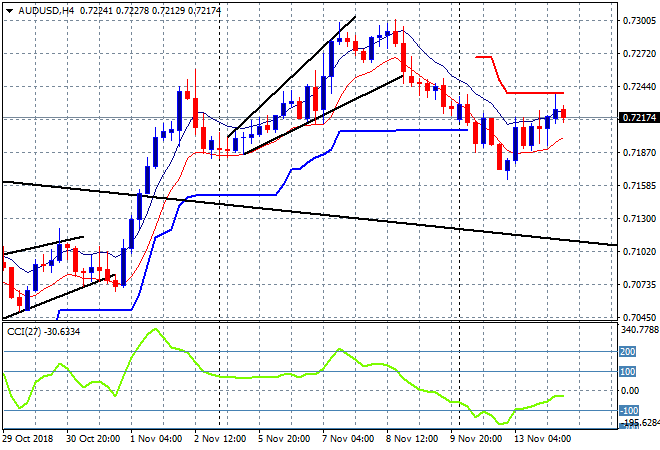

The ASX200 was the worst performer and again finished nearly 1.8% lower to break below the 5800 point support level, closing at 5732 points with the banks the biggest drag as Megabank feels the heat. The Aussie dollar has found some more buying support here, continuing its small bounce to remain just above the 72 handle, but I still contend this looks like short covering at best:

The economic calendar has three major releases tonight, first in Europe its German and EZ 3Q GDP and UK October CPI, while in the ‘States its also the October CPI print plus Fed Chairman Powell’s speech to keep an eye on.