Stocks are sharply lower across most of the region in response to the risk off mood overnight with the added concern of a breakdown in Brexit negotiations and the falling oil price adding to the tensions. The PBOC again moved the Yuan closer to the 7 handle in a big move in today’s fix with all eyes on the upcoming US/Chinese trade talks which could be another catalyst for a risk-off correction if a depressed Trump drops the ball. Again. Hope it doesn’t rain…

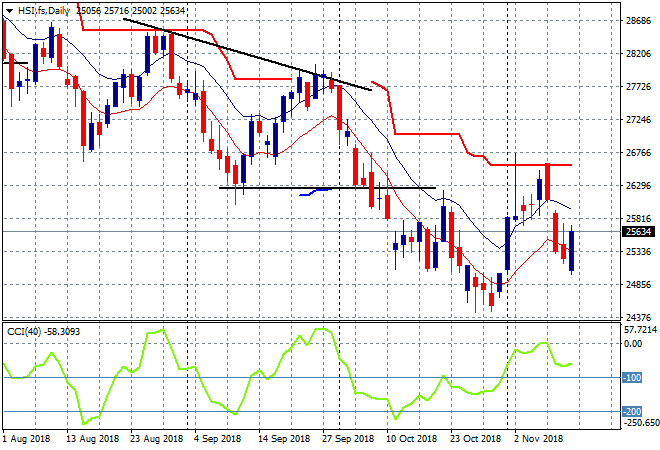

The Shanghai Composite has closed 1 % higher to 2658 points, now building on its recent move above key support at the 2600 level and shrugging off concerns about the trade talks – more likely because the PBOC directly injected funds into the market again. The Hang Seng Index is treading water however, down about 0.1% or so to 25614 points, with the daily chart showing how it’s been unable to get back to the previous support level at 26000 points:

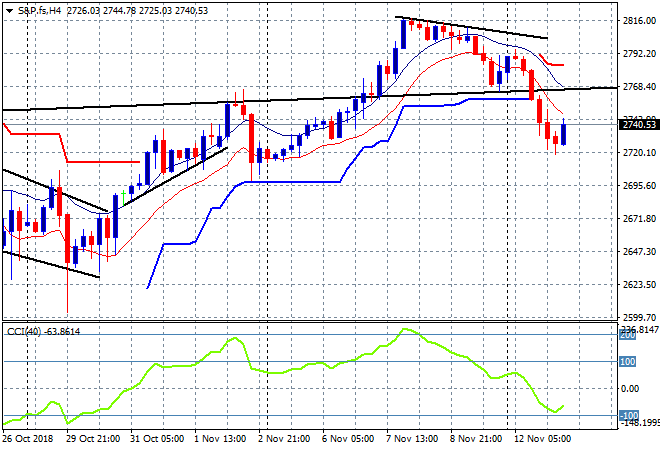

US and Eurostoxx futures are up slightly here with the four hourly S&P 500 futures chart showing a potential and short term bottom at the 2720 level after last nights swift falls

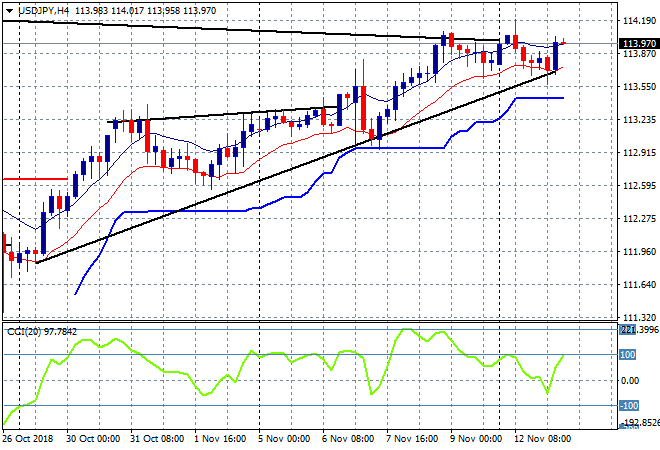

Japanese stocks have fallen the hardest in the region even as the usually positively correlated USDJPY pair advanced. The Nikkei 225 closed over 2% lower to 21810 points although it was down lower during the session. The USDJPY pair is getting ready to tackle last week’s high hereagain above the 114 handle after a staid session yesterday:

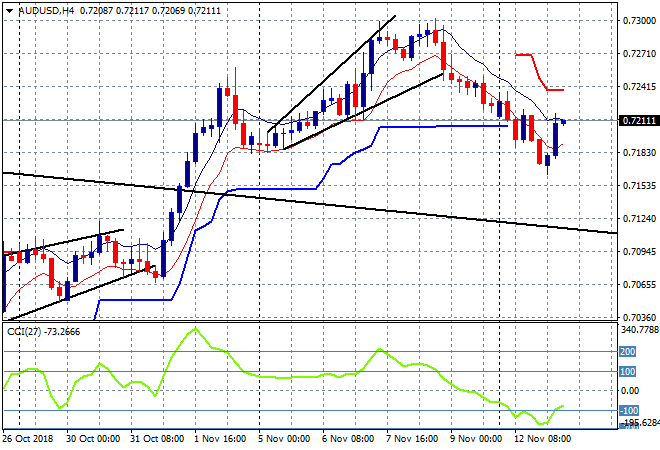

The ASX200 gave back all of its recent gains to finish 1.8% lower to finish the day at 5834 points, unable to hold on to support at the 5900 level. The Aussie dollar has found some buying support here with a small bounce to get just above the 72 handle . Note however on the four hourly chart that the high moving average remains untouched with momentum still quite negative – this looks like short covering at best:

The economic calendar ramps up tonight with an inmportant German ZEW survey just as Brexit negotiations push on for a potential November deadline.