A slew of bad internal data and new policy directions by Chinese authorities – not helped by another big easing in the Yuan fix by the PBOC today – has seen Chinese equity markets selloff to close the week out in a bad note. With no new direction from the Fed overnight, looking set to raise interest rates next month, currency markets re-evaulated their weak USD positions and turned them around, with the Aussie and Kiwi off the boil, the former not helped by a wishy washy SOMP by the RBA.

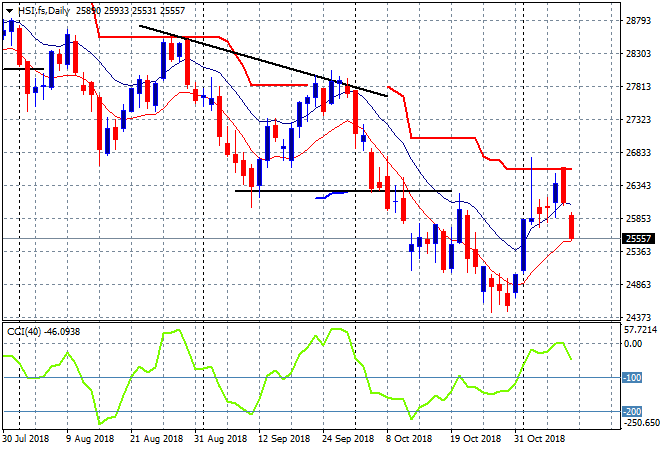

The Shanghai Composite looks set to close 1.3% lower, currently at 2601 points, barely hanging on to key support at the 2600 level as it has been unable to translate the recent swing gains into a proper recovery all week. The Hang Seng Index is off even sharper, down 2.4% to 25608 points, gapping down just after it was starting to get some traction above the previous support level at 26000 points:

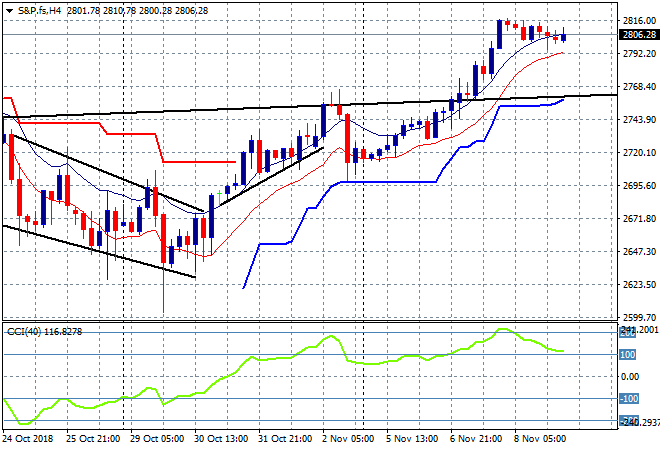

US and Eurostoxx futures are stalled here going into the final session of the week with the four hourly S&P 500 futures chart continuing its pause here as the oversold rally looks set to just consolidate here above the 2800 point level:

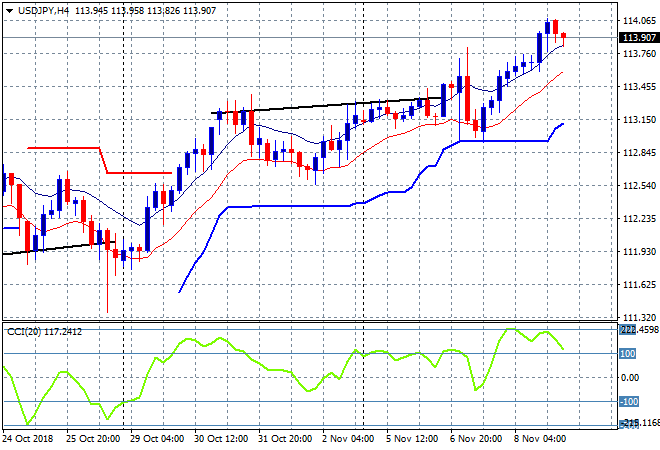

Japanese stocks have retraced as Yen buyers stepped in briefly to cap the overbought USD, the Nikkei 225 suffering by falling just over 1% to 22250 points. The USDJPY pair is looking very overextended here and is hovering just below the 114 handle as buying exhaustion is setting in here:

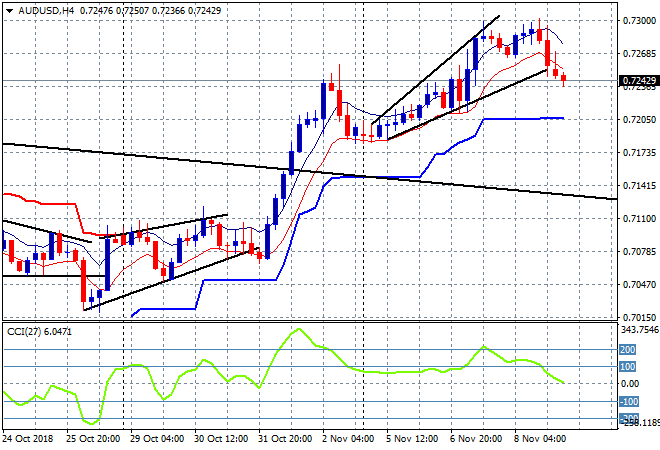

The ASX200 was the best performer, basically only treading water with a small fall of 0.1% to finish the day at 5921 points. The Aussie dollar is failing here with another poor session, down to the low 72’s as the USD gains strength:

The economic calendar finishes the week with UK preliminary 3Q GDP estimates, plus the University of Michigan consumer sentiment survey – plus the usual Trump drama.

Have a good weekend!